It might not quite be THAT red phone that’s ringing, but rest assured, management is currently dealing with a serious problem, and they are looking at IT to solve it for them.

There are two things that make Boards and C-Suites nervous beyond all else. Risks that have the potential to impact the bottom line and company/brand reputation. This current issue can do both and fast if not dealt with timely.

I’m talking about government tax mandates.

Now you may ask, haven’t government mandates been around for decades? Why the urgency now? Yes, they have been around for a long time, but they have never existed in their current form or had the ability to impact your operations so quickly.

Allow me to explain. In the past, organizations around the world were required to report on transactions after the fact and pay the amounts they were legally obligated to pay. If they didn’t, the government might get around to auditing them a few months or years down the road and assess a penalty if things were found to be out of order. In the grand scheme of things, it was a minor inconvenience for businesses and not a real deterrent for having faulty processes or negligence.

That all began to change a few years back when governments began looking at a tax gap that was growing with no easy solutions to reign it in. Think I’m exaggerating? According to the 2021 report on the VAT Gap issues by the European Commission, in 2019 alone EU countries lost out on €134 billion in Value-Added Tax (VAT) revenues legally owed to them by businesses.

This was a wake-up call to every country that employs the VAT system of taxation anywhere in the world. Not only were they losing out on much needed revenues, but the problem was growing worse. Something needed to be done and done fast or they wouldn’t be able to fund vital programs in their countries.

Fast forward to today. Countries have taken a serious look at the problem and have decided that technology is the answer. They have invested heavily in digitization and have brought their capabilities not only up to par with business, but in many cases, probably for the first time in history, have surpassed the capabilities of private industry to monitor and report on financial transactions.

Today, there is no more reporting after the fact. Governments have set up shop right in your data stack and are reviewing transactions in real-time. And with real-time monitoring has come real-time enforcement. If you are not reporting the information the way the government has mandated, you can expect swift action ranging from expensive fines right up to the revocation of your business license in that country. Both would be devastating shots to your company’s financial outlook and reputation.

This is why there is so much urgency to get IT on board and have a strategy to address the issue on a global basis. Things are only going to get more complicated and the ability to scale systems to meet changing tax mandates in all places you do business has become a top priority for companies.

It’s a new world out there as far as VAT is concerned and this is a lot to come to terms with. If this is new information to you or you are in the process of coming to terms with how it impacts your organization, I’d encourage you to remember and share the following five things with your colleagues:

1. The government is in your data

Real time tax reporting is becoming the new norm for businesses worldwide. Governments are no longer satisfied with receiving data after the fact and are now requiring a permanent presence in your data stack.

2. Government data mandates are taking control away from companies

With government mandated e-invoicing taking the world by storm, businesses are left with little time to prepare for this shift. To remain operational and comply with these mandates, IT must create a strategy to ensure that they are meeting mandate obligations while keeping with the parameters of long-term plans and budgets.

3. Data mandates are moving and evolving quickly

As governments are rapidly moving towards mandated e-invoicing implementation, organizations are now faced with an extremely short window to update their tax codes and mandates. For IT departments, overseeing and executing these changes will become one of their top priorities.

4. Data mandates lack consistency from country to country

For international organizations staying up to date on new processes, technologies and regulations are all essential components to running a successful business. However, the different approaches being adopted by each individual regulatory authority are causing a lot of uncertainty for businesses. The challenge for IT is to create the infrastructure that allows the business to meet the individual mandates of each country’s regulatory authority, while also integrating with one another to provide a real time global dashboard of the organization’s compliance status.

5. Governments have increased the severity and speed of enforcement

Tax authorities are becoming more aggressive than ever to close tax gaps. With the use of digital tools and processes, governments can quickly expedite compliance and track tax fraud effectively. In today’s digital world, penalties can be swifter and more severe than in the past. IT needs to ensure that transaction data is presented to regulatory authorities in the format and time frame they demand.

I’m hopeful this information will give you some things to think about as you work through the changing realities of global tax mandates.

Invoicing in Chile is changing on 1 December 2022. This is when resolution 66 from the Chile Internal Revenue Service comes into force.

This new regulation concerns organisations with foreign currency operations. Banks, stockbrokers, exchange houses and financial institutions are affected. Other intermediaries or entities that carry out foreign currency purchase and sale operations themselves or on behalf of third parties are also included.

All these organisations must issue the following:

Electronic invoice

Invoice Not Affected or Exempt Electronic

Electronic Credit Note

Electronic Debit Note

Electronic Ticket

Electronic Ticket Not Affected or Exempt

How is invoicing in Chile changing?

Every electronic tax document must consider the specifications described by “Electronic Tax Document Format”. This document is available on the Internal Revenue Service’s website and is regularly updated.

What electronic information is required in Chile?

Resolution 66 also contains technical instructions. These establish the details necessary for electronic tax documents that support foreign currency purchase and sale operations.

The resolution states the following must be included:

Name and code of the traded currency

Transaction type and detail

Exchange rate

Amount traded

Total value

Date of the transaction

There are other requirements not listed above, so it’s important to check the guidelines.

This change allows the Internal Revenue Service to receive, validate, and process electronic tax documents. This ensures the operations are accurately reflected and prevents inconsistencies.

More on rights, commissions and other charges in Chile

In the case of commissions, the taxpayer must issue an invoice or electronic ticket containing all the information indicated by the Technical Annex.

If the document doesn’t include an affected item, consider the following:

Likewise, when differences in collections and values are subject to VAT, an electronic credit or debit note must be issued.

The following information must be recorded separately as well:

The total value of the instruments traded

Value of commissions and charges, if any

Total to be paid in favour of the client or total to be paid in favour of the company

Need help for invoicing in Chile?

Are you in financial services or working at a bank with more questions about invoicing in Chile? Speak to our tax experts.

A recent preliminary ruling request to the European Court of Justice, Case C-664/21, NEC PLUS ULTRA COSMETICS, has re-emphasised the importance of collecting documentation when carrying out a zero-rated supply in the EU. The 2017 NEC PLUS ULTRA COSMETICS case involved a company established in Switzerland selling cosmetics products under the Ex Works clause from their warehouse in Slovenia to business customers established in Romania and Croatia. Ex Works (EXW) is an Incoterms rule, a set of definitions outlining the responsibilities of buyers and sellers in international transactions. With Ex Works the transport obligations, costs and risks are the buyer’s responsibility.

The tax administration of the Republic of Slovenia inspected NEC PLUS ULTRA COSMETICS and requested evidence and supporting documentation relating to these supplies to verify that goods had been transported to another EU Member State.

NEC PLUS ULTRA COSMETICS provided copies of the invoices and of the ‘Convention relative au contrat de transport international de marchansises par route’ (CMR) consignment notes. The company failed to provide the evidence requested by tax officers to prove the right to tax exempt the supplies to their customers (delivery notes and other documents mentioned in the CMRs).

The company clarified that the reason for the late submission was that the Hamburg office responsible for supplies to Croatia ceased its activities in August 2018, making it more difficult to find the documents asked for by the tax officers.

Consequently, the Slovenian tax authorities provided the company with an additional VAT assessment notice and ordered it to pay the relevant amount.

What documents do you need to keep for supplies carried out after 2020?

In the implementation of the Quick Fix related to the proof of transport in 2020, the European Commission has clarified that where the supplier arranges transportation of the goods, it must be in possession of either:

At least two non-contradictory items of evidence from two sources independent of each other and of the supplier and of the acquirer in what HMRC neatly describes as List A, below, or

A single item from List A and a single item from List B, below, again from non-contradictory and independent sources:

List A

Signed CMR document or note

Airfreight invoice

Invoice from the carrier of the goods

Bill of lading

List B

An insurance policy for the transport of the goods

Bank document proving payment for the transport of the goods

Official documents issued by a public authority, such as a notary, confirming the arrival of the goods in the Member State of destination

Warehouse keeper’s receipt confirming storage of goods in the Member State of destination

If the acquirer is responsible for transport of goods (i.e. under the Ex Works clause), they must provide the vendor with a written statement by the 10th of the month following the date of supply that the goods have been transported by the acquirer or on the acquirer’s behalf. The written statement must include the following:

Date of issue

Name and address of the acquirer

Date and place of the arrival of the goods as well as the Member State of destination

Quantity and nature of the goods

Where it is a means of transport, its identification number

Identification of the individual accepting the goods on behalf of the acquirer.

How to ensure VAT compliance

In the case of the Ex Works clause:

Agree in the contract/purchase order that your customer is required to provide you with all required documents within an internal scheduled deadline; and

Keep this documentation according to the Statute of Limitation of each EU Member State where you trade.

If you don’t feel reassured by your customer, change the agreement and Incoterms clause before the supply takes place.

Need help with VAT compliance?

Still have questions about VAT exempt supplies and the Incoterms Ex Works clause? Speak to our tax experts.

Part II of V – Oscar Caicedo, Vice president of product management for VAT Americas, Sovos

Government-mandated e-invoicing laws are making their way across nearly every region of the globe, bringing more stringent mandates and expectations on businesses. Inserted into every aspect of your operation, governments are now an omni-present influence in your data stack reviewing every transaction in real time as it traverses your network. Real-time monitoring has also brought about real-time enforcement that can range in severity from significant fines to shutting your business down completely. All of this has created a new reality for IT leaders who need a strategy to deal with these global changes. We asked our vice president of product management for VAT, Oscar Caicedo to offer his guidance on how this will affect IT departments and how they can best prepare.

Q: With government authorities now in companies’ data and demanding real or near real-time reporting, what impact will this have on IT departments?

Oscar Caicedo: For me, this breaks down into four distinct categories:

1. Business Process Architecture – As regulatory entities become more advanced, it is important to look at the overall functional business process, not only the technical mechanism to report. Many business processes were solidified much before current capabilities were readily available. It is important to revisit the business process to be able to determine the best technical path forward.

2. Source of Truth – With the complex environment IT departments must navigate, you need to redefine the expectations of data/process source of truth. Back-end system ecosystems were not built with current compliance/regulatory needs in mind. In mature markets, where governments continue to advance technical capabilities, it is critical to have a clear strategy to protect against source-of-truth risks. Otherwise, local regulatory entities tend to become the ultimate source of truth.

3. Data Aggregation/Reconciliation – A lack of clarity on the source of truth for each functional business process can lead to major risks. Registering data in real time with local regulators was the initial challenge. The current challenge is ensuring all systems involved are maintained in sync and are always fully harmonized. IT departments must recognize it is now a must-have to navigate the current environment.

4. Master Data – Data in back-end systems was already complicated enough to support in a centralized manner. Once real-time regulatory needs were introduced, the data issue got exponentially larger. Data structures, data libraries and extraction programs are all attempts to solve the problem, but normally these attempts fail due to gaps in understanding what is mandatory vs. optional. Clear guidance on the local needs is critical before deciding on a technical strategy.

Q: To meet government mandates and ensure operations continue uninterrupted, what should IT prioritize? What approach would you recommend?

Oscar Caicedo: I would prioritize a clear regulatory understanding of the markets/geographies in which you operate. This seems obvious, but it is not always the case. Ninety-nine percent of the time when I speak with a large multinational organization, they are not clear on the needs of the local market. Efforts to centralize or take a cohesive approach fail because key IT decision makers didn’t understand the regulation.

In addition, you need to focus on business processes and the data requirements to make them successful and solve the problem end to end. The challenge does not end with registering data. The problem ends when you have the proper visibility, maintenance, support, reconciliation and intelligence to be fully prepared.

Don’t take chances. The regulatory environment is very dynamic, so it is important to ensure the proper testing of all business scenarios needed to operate. Failure to have clear testing scripts can lead to surprises in production environments, which can carry large implications for the operation.

Finally, consolidate as much as possible. This means simplifying end points, communication protocols, data structures, etc. This will allow for a more efficient way to manage the mandated processes in the different jurisdictions.

A lot has changed in the world of government mandated e-invoicing. Continued investment in technology by government authorities has put regulators in the position to demand greater transparency along with more detailed and real-time reporting. To meet these demands, companies are looking to their IT organizations. The good news is you don’t need to go it alone. Sovos has the expertise to guide you through this global evolution based on our experience working with many of the world’s leading brands.

Take Action

Need help keeping up with global mandates? Get in touch with Sovos’ team of tax experts.

Imagine this scenario.

Your business partner changes the rules on you mid-stream and your ability to conduct business with them is now contingent on changing your entire reporting structure to meet their new demands.

Oh yeah, I should also mention the time frame to meet these demands is extremely tight and if you don’t, you can forget about doing business in their region until you get it right. And if at any point moving forward you fail to live up to these standards, they can fine you or shut you down.

Sound farfetched? It isn’t. It’s exactly what is playing out in major economic markets from Brazil to Italy and parts of Asia and Africa. You see, governments have caught up to businesses when it comes to technology, and in many ways, they have moved past them when it comes to digitization.

What does this mean for you?

It means that governments have now taken on a more proactive approach to reviewing financial transactions and are demanding real-time reporting. As part of that, they have implemented real-time enforcement to ensure that it’s meeting the proper mandated specifications. To accomplish this, they have taken up permanent residence within your data stack. And make no mistake, when it comes to e-invoicing, they are calling the shots.

A bit of background.

Governments throughout the world are implementing mandated e-invoicing for its ability to facilitate compliance and track fraud quickly and efficiently. After the fact reporting, which had been the norm until now, was more difficult to enforce and took lengthy and costly audits to recoup what was rightfully owed. Many organizations didn’t take the penalties seriously and would simply set aside some money to deal with these inconveniences as they emerged.

This approach resulted in a tax gap that is continuing to grow. In 2019, the VAT gap of the European Union’s 28 member states was over 134.4 billion euros for all member states combined. This had become unsustainable and unacceptable to many governments and thus a new technology that focused on digitization was made to ensure that all legally owed revenue was being collected timely and in full. Failure to comply would lead to faster and more impactful enforcement measures.

This trend is growing rapidly with countries across the globe adopting new mandates and methodologies for tracking and enforcing the rules. In the next five years nearly every country that employs the VAT system of taxation is expected to update their systems to some degree.

Make no mistake. Due to the demands for real-time information, this is an IT problem, not a tax issue. For multinational companies that do business in dozens of countries, there could be some painful moments along the way if they don’t plan early and develop a sound strategy for each of the locations in which they have operations.

Here is my advice for meeting government mandates and ensuring operations continue uninterrupted.

IT should focus on the end goal: implementing a centralized approach to managing these government mandated e-invoicing laws to ensure a globally consistent approach to all digital filings. I can’t overstate the importance of implementation synergies as requirements increase and expand. This is only going to get more complex as time goes on.

And perhaps most importantly, don’t be afraid to ask for help. This is complicated stuff that is changing by the day. This is not the time or the issue to try going it on your own.

Take Action

Reach out to our experts for more help and information.

Part I of V – Steve Sprague, chief commercial officer, Sovos

Government-mandated e-invoicing laws are making their way across nearly every region of the globe, bringing more stringent mandates and expectations on businesses. Inserted into every aspect of your operation, governments are now an omni-present influence in your data stack reviewing every transaction in real time as it traverses your network. Real-time monitoring has also brought about real-time enforcement that can range in severity from significant fines to shutting your business down completely. All of this has created a new reality for IT leaders who need a strategy to deal with these global changes. We asked our chief commercial officer, Steve Sprague to offer his guidance on how this will affect IT departments and how they can best prepare.

Q: With government authorities now in companies’ data and demanding real or near real-time reporting, what impact will this have on IT departments?

Steve Sprague: CIOs need to make a choice – do they pivot with these changes and adopt a centralized approach to their data, systems, business processes and applications, or do they run a decentralized platform where every country is left to make their own decisions? More than 95% of companies have implemented a decentralized approach as these mandates have grown country by country. However, as Latin America has grown from only three countries instituting these mandates in 2014 to more than 14 countries implementing them now, and with another 30 countries around the globe beginning the process of implementing similar regimes, including economies across Asia and Europe, like France and Germany – a decentralized approach leads to several long-term problems, including:

• Limited visibility outside of the country

• Multiple tools and vendors across different countries

• Disjointed processes with a focus on fulfilling local obligations only

• Solving the “problem at hand” vs. looking at the bigger picture

• Poorly defined roles and responsibilities

• Inconsistent approach to implementing additional countries

Q: To meet government mandates and ensure operations continue uninterrupted, what should IT prioritize? What approach would you recommend?

Steve Sprague: IT should focus on the end goal: implementing a centralized approach to these government mandated e-invoicing laws to ensure a globally consistent approach to all digital filings. There will be cost reduction as the number of vendors and tools are consolidated, and risk will be further mitigated through increased standardization and visibility. I can’t overstate the importance of implementation synergies as requirements increase and expand. This is only going to get more complex as time goes on. The clarity of roles and responsibilities is the other benefit to IT teams, as this approach will lead to clearly defined areas of focus for the team. Finally, alignment of analytics through one data hub will now be possible, providing a centralized dashboard for your global operations.

A lot has changed in the world of government mandated e-invoicing. Continued investment in technology by government authorities has put regulators in the position to demand greater transparency along with more detailed and real-time reporting. To meet these demands, companies are looking to their IT organizations. The good news is you don’t need to go it alone. Sovos has the expertise to guide you through this global evolution based on our experience working with many of the world’s leading brands.

Take Action

Need help keeping up with global mandates? Get in touch with Sovos’ team of tax experts.

France is implementing a decentralised continuous transaction control (CTC) system where domestic B2B e-invoicing constitutes the foundation of the system, adding e-reporting requirements for data relating to B2C and cross-border B2B transactions (sales and purchases).

Under this upcoming regime, data or invoices can be directly sent to the Invoicing Public Portal ‘PPF’ (Portail Public de Facturation, so far known as Chorus Pro) or to a Partner Dematerialization Platform ‘PDP’ (Plateformes de Dématerialisation Partenaires). In addition, there are also Dematerializing Operators (Operateurs de dématérialisation) that are connected to either the PPF or a PDP.

Requirements for these portal and platforms have been published.

New details on requirements for portals and obtaining PDP status

The Ministry of Economy published Decree No. 2022-1299 and Order of 7 October 2022 on the generalisation of e-invoicing in transactions between taxable persons for VAT and the transmission of transaction data (together known as ‘new legislation’), providing long-awaited details for PDP operators and PPF.

The new legislation introduces rules concerning the application process for PDP operators. Although French establishment isn’t required, PDP operators must fulfill a number of requirements, such as operating their IT systems in the EU.

France is implementing a model where third-party service providers are authorised to transmit invoices between the transacting parties. With the mandatory use of the PPF or PDPs for exchanging e-invoices, trading parties cannot exchange invoices between them directly. Therefore, PDPs must be able to receive and send invoices in structured formats, whether the ones supported by the PPF (CII, UBL, or FACTUR-X) or any other required by their clients. Also, to ensure interoperability, PDPs are expected to connect with at least one other PDP. Besides this requirement, it’s stated by the new decree that PDPs must be able to send e-invoices to PDPs chosen by their recipients which implies a complete interoperability between PDPs.

Transitional period for submitting PDF invoices

It was previously announced that taxpayers could submit PDF invoices for a transitional period. The new legislation outlines the transitional period as until the end of 2027. During this period PDPs and PPF must be able to convert the PDF into one of the structured formats.

New details on e-invoicing and e-reporting in France

The new legislation also provides information about the content of e-invoices, which has new mandatory fields, and the content of transaction and payment data to be transmitted to the tax authority.

It also announced frequencies and dates of data transmission. Deadlines for transaction and payment data transmission are based on the tax regimes of taxpayers. For example, taxpayers subject to the normal monthly regime should transmit payment data within ten days after the end of the month.

With the aim of having traceability over documents, the lifecycle statuses of the domestic B2B e-invoices are exchanged between the parties and transmitted to the PPF. Lifecycle statuses that are mandatory (“Deposited”, “Rejected”, “Refused” and “Payment Received”) are listed in the new legislation.

Further details regarding the Central Directory, which consists of data to properly identify the recipient of the e-invoice and its platform, are provided within the Order.

The road ahead for service providers

PDP operator candidates can apply for registration as of Spring 2023 (precise date still to be confirmed), instead of September 2023 as previously set. From January 2024, a six-month test run is expected to be conducted for enterprises and PDPs before the implementation in July 2024.

Postponement of EFD-REINF Deadline for Events Referring to Withholding IRPF, CSLL, PIS and COFINS

The publishing of Normative Instruction RFB n. 2.133, of 27 February 2023 postpones the deadline of the obligation to submit EFD-REINF (Digital Fiscal Record of Withholdings and Other Fiscal Information) events related to withholding:

IRPF (Personal Income Tax)

CSLL (Social Contribution on Net Income)

PIS (Social Integration Program)

COFINS (Contribution for the Financing of Social Security)

This postponement refers to taxpayers who are currently obliged to submit the DIRF (Withholding Income Tax Return) and were required to comply with the EFD-REINF obligation from March 2023.

The obligation to submit the EFD-REINF for these taxpayers will now begin from 8:00 am on 21 September 2023, in relation to taxable events that occur from 1 September 2023.

The postponement is to allow time for taxpayers to carry out adjustments to their computerised systems and for the Brazilian Federal Revenue Agency to finalise the necessary tests to guarantee the consistency of the rules for validating the information captured in the record.

Since 2007, the Brazilian government has imprinted high efforts in digitizing the relations between revenue offices and taxpayers, by introducing electronic instruments to ensure taxpayers provide accurate and timely information on the collection of the various existent taxes, duties, charges, and contributions.

One result of such efforts was the creation of the Public Digital Bookkeeping System (Sistema Público de Escrituração Digital) or SPED. This platform is where taxpayers submit fiscal and accounting information using different electronic instruments referred to as SPED modules.

There are significant upcoming changes to one of the modules, the Digital Fiscal Record of Withholdings and Other Fiscal Information (Escrituração Fiscal Digital de Retenções e Outras Informações Fiscais), known as EFD-REINF.

The latest regulatory updates within this module concern steps towards the substitution of other records by the EFD-REINF, with important changes taking place in 2023.

Main changes in the EFD-REINF

In August 2022 version 2.1.1 of the EFD-REINF layout was introduced, expanding the reach of events covered by the record. The current 1.5.1 version is valid until February 2023 and from March 2023 layout version 2.1.1 must be used.

The main change is the inclusion of the ‘R-4000’ series events. These events cover the registration of withholdings on income tax (IR), Social Contribution on Net Income (CSLL), Social Integration Program (PIS), and Contribution to the Financing of Social Security (COFINS), among other fiscal contributions.

Another relevant change is the removal of the requirement to submit the EFD-REINF ‘without movement’. Previously, only a certain group was permitted for this exemption if they didn’t generate any records to be reported in the respective declaration period but this has now been expanded to all taxpayers in scope of the EFD-REINF.

New obliged taxpayers

Earlier this year, RFB Normative Instruction n. 2.096 of 2022 postponed mandatory submission of the EFD-REINF for the fourth and last group of taxpayers: entities that are part of the ‘Public Administration’ and entities classified as ‘International Organisations and Other Extraterritorial Institutions’. Since August 2022 this group is now obliged to comply.

However, the same regulation established that from 1 March 2023 taxpayers currently obliged to submit the DIRF (Withholding Income Tax Return) will be required to comply with the EFD-REINF obligation. This is an extensive list found in article 2 of RFB Normative Instruction n. 1.990 of 2020, which includes individuals and legal entities that have paid or credited income for which Withholding Income Tax (IRRF) has been withheld and certain entities of the Federal Public Administration, among others.

Finally, the annual submission of the DIRF will be abolished regarding events that occur from 1 January 2024, meaning that taxpayers won’t be required to submit it in 2025. Until then, the information declared in the DIRF and EFD-REINF will coexist.

Compliance challenges

Keeping up with the mosaic of fiscal requirements within the federal, state, and municipal levels in Brazil normally requires engaging the services of an expert or risk incurring high penalties. Modifications to fiscal obligations are implemented regularly in the country, which means companies must ensure readiness to comply.

A complement to eSocial (which covers tax withholdings on wages), EFD-REINF reports withholdings made to individuals and corporations resulting from the application of the income tax and social security taxes (CSLL, INSS COFINS, PIS/PASEP). It also applies to payments received by sport associations and revenues generated by sport events.

EFD-REINF replaces reporting obligations that the Brazilian taxpayers have to comply with under the EFD-Contribucoes.

Who must comply?

Legal entities:

That provide and contract outsourcing services in accordance with art. 31 of Law No. 8,212 of July 24, 1991

Who are responsible for withholding the social security taxes PIS/Pasep, the Cofins and the CSLL

Opting for payment of social security contribution on gross revenue (CPRB)

Entities considered rural producers and agro-industries when subject to substitutive social security contribution on the gross revenue from the commercialization of rural production

Sports associations that have professional soccer teams receiving revenues related to sponsorship, licensing of use of brands and symbols, marketing, advertising and broadcasting of sports shows

Sponsors that provide resources to those sports association

Entities marketing any sport event held in Brazil, involving at least one sport association that owns a professional soccer team

Entities and individuals that have paid or credited income on which the federal income tax has been withheld by themselves or as representatives of third parties

How is the EFD-REINF structured?

There are three groups of reports, or “events,” that must be submitted to the tax administration:

Table Events (Eventos de Tabela): Intended to optimize and validate the information that identifies the taxpayer and some administrative and legal processes that may affect them (if they exist).

Non-Periodic Events (Eventos Não Periódicos): Information related to transactions that do not occur on a regular basis and therefore should only be reported when they occur.

Periodic Reports (Eventos Periodicos): Events related to periodic information that should be reported on a regular basis by the taxpayer. These include:

Withholdings for Social Security tax for services received

Withholdings for Social Security tax for services provided

Revenues received by sport associations

Revenues Transferred by sport associations

Social Security tax on gross receipts

Withholding taxes (IR, CSLL, Cofins, PIS/PASEP)

When does it go into effect?

The EFD- REINF is being rolled out in three stages.

May 1, 2018: Companies with revenues greater than 78 million Real annually

November 1: Companies with revenue less than 78 million Real

May 1, 2019: All public entities

What are the penalties for non-compliance?

Events that are incomplete, or reported with errors, will a face fines totaling 3% of the amount involved, with a minimum of $100 Real in the case of legal entities, and half of the above amounts when the taxpayer is an individual. Fines for late reports will range between from $500 Real to $1,500 Real per month or fraction of month.

With half a billion consumers, the EU market represents huge growth options for e-commerce companies. Maximize this potential through a seamless B2C service with fast delivery and no unexpected customer VAT charges.

Sovos Compliance Services Portal for e-commerce allows easy access to all simplified EU VAT reporting schemes:

IOSS (Import One-Stop-Shop)

Simple customs clearance

VAT collected at point of purchase

Reclaim VAT on returned goods

Union OSS

Low-cost Compliance for intra-EU trade

Essential for anyone with >€10k intra-EU sales & all non-EU businesses holding stock in EU

Report EU B2C goods and services through a single VAT Return

Non-Union OSS

Compliance simplicity for digital services from outside the EU

Stay ahead of current and future compliance obligations.

Monitor 60+ countries to track the diverse range of emerging legal frameworks and evolving specifications.

Simplify compliance vendor relationship management with a single, global point of contact.

Ensure invoices continue to flow, so your business and its supply chains run smoothly.

Minimize the need for ad hoc IT involvement and investment in compliance updates.

Save time, eliminate labor-intensive manual updates, and enhance accuracy.

Stop worrying about ever-changing different country formats and processes.

Reduce your total cost of compliance.

Sovos Compliance Services Portal for E-Commerce

IOSS Intermediary Services

Validation Checks

Service Levels to Suit Your Budget

Registrations Services

Return Filing

Dashboard View of all Your VAT Registrations and Returns

Secure Data Upload & Mapping

Audit Assistance by VAT Compliance Experts

Intermediary Service Supporting Global Businesses

Companies not established in the EU (unless established and supplying from Norway) are required to appoint an Intermediary to facilitate the reporting and payment of VAT under the IOSS scheme.

Sovos is set up to act as an Intermediary on behalf of your business. We will ensure that you reap the benefits of the simplification while safeguarding against the risk of penalties and expulsion for non-compliance.

Intermediaries assume joint responsibility for:

Reporting and payment of VAT under IOSS

Record keeping

Improve the Quality of Your Data

The Sovos Compliance Services Portal empowers you to take control of your sales data. Once you’ve mapped it into our portal, our tool allows you to run your own validation checks and correct any errors before our team of experts completes the filing. Our VAT Compliance for E-commerce solution gives you peace of mind that your data is secure and that your (I)OSS VAT return is accurate and reliable.

Stay Compliant and Mitigate Business Risks

Future proof your VAT compliance profile, ensure your goods are delivered in a timely manner to your customers and do not get stuck at the border. Sovos Compliance Services Portal is underpinned by the deep knowledge and expertise of our Compliance Services & Consulting teams.

Our solution means you can:

Take advantage of the benefits of (I)OSS schemes

Access support for trading complexity: multi-country warehousing, stores and B2B

Leverage a single provider for periodic and continuous ‘real-time’ reporting

Streamline your processes

Reduce risk of managing VAT Compliance manually

Managed services

Technology enabled VAT managed services

A blend of human expertise and software to ease your VAT compliance workload and reduce risk wherever you operate today while ensuring you can easily flex to handle VAT requirements in the markets you intend to dominate tomorrow.

On 30 August 2022, the Ministry of Finance published draft legislation amending the Regulation on the use of the National e-Invoice System (KSeF). The purpose of the draft amendment is to adapt KSeF’s terms of use to the specific conditions that apply to the local government units and the VAT groups that will operate as a new type of VAT taxpayer from 1 January 2023.

The current regulatory status in Poland

The concept of VAT groups was introduced in Poland in October 2021. VAT groups are a legal form of cooperation, a type of taxable entity that exists solely for VAT purposes. On joining a VAT group, a group member becomes part of a new separate VAT taxpayer possessing one Polish tax identification number (NIP).

The regulation on the use of KSeF didn’t take into consideration the uniqueness of the legal nature of the VAT group, as well as the VAT settlements in the local government units. Based on current regulation, the governmental units are treated as a single VAT taxpayer, using one NIP number.

Similarly, in the case of VAT groups, separate VAT taxpayers who create one new taxpayer (a VAT group) use one NIP number. The proposed changes resulted from the ongoing public consultations that took place in December 2021. Additionally, the change was also requested in May 2022 by the Union of Polish Metropolises.

Proposed amendments to the current e-invoice regulation

The draft law provides the possibility to grant additional limited rights for the local government units and members of VAT groups. Moreover, local government units and VAT groups will be able to grant administrative rights, to manage permissions in KSeF, to a natural person who is their representative.

Thanks to such delegated rights, there will be an option to manage authorisations for the local government unit and for the entity that is a member of a VAT group. Moreover, it is significant that a person with such authorisation will not have simultaneous access to invoices in other units within the local government or within other members of a VAT group.

For local government units and VAT groups, granting or withdrawing authorisation to the natural person must be performed electronically. It’s not possible to submit a paper form to notify the competent tax authority.

Remaining issues for KSEF and enforcement date

As mentioned, the proposed amendments are in response to concerns that were raised by the impacted entities. However, they don’t meet all the needs of local government units and VAT groups. For instance, the question of how to assign an inbound electronic invoice to a particular internal unit or member of a VAT group remains open. This is because invoices contain only the data of the taxpayer, which in this case is the local government unit or a VAT group, and not data of the internal unit or member of a VAT group.

The regulation will enter into force 14 days after the date of publication. However, provisions that apply to VAT group members will be effective from 1 January 2023.

With the deadline rapidly approaching, here’s a brief recap.

The Customs Handling of Import and Export Freight (CHIEF) system, which is now nearly 30 years old (it was introduced in 1994), will close in two phases:

Phase one: After 30 September 2022, the ability to make import declarations will end

Phase two: After 31 March 2023, the ability to make export declarations will end

The Customs Declaration Service will serve as the UK’s single customs platform, with all businesses needing to declare all imported and exported goods through the Customs Declaration Service (CDS) after 31 March 2023.

CDS benefits and key changes

As mentioned on the HMRC website, the Customs Declaration Service toolkit gives traders access to the many benefits of the upcoming changes. In summary:

Benefits

Using the latest technology, CDS delivers an enhanced service and user experience

CDS has the capacity and capability to grow in line with the government’s growth agenda, alongside plans to increase the volume of international trade

CDS offers a host of specialist functions and interfaces. Underpinned by modern, cloud-based architecture, it’s fully agile and adjustable

Businesses can declare all goods on one platform simultaneously, regardless of the customer journey. This process reduces operational costs and lessens the administrative burden of running two separate customs systems

Declaration data is transparent and free of charge – businesses can easily access real-time import and export data and check tariffs and financial statements online using dedicated digital dashboards

CDS is designed to be completed digitally.

CDS changes

CDS captures some information differently, and the way the business inputs data is different (additional information and supplementary documents will be required for some commodity codes imported into the UK)

There will be additional methods to make payments of customs duties as follows:

Cash accounts

Duty deferment accounts

Immediate payments

Guarantee accounts

Individual guarantees

CDS enables you to update customs agent permissions online

What does this mean in practice?

To be able to use CDS and import goods into the UK from 1 October 2022 and to export from 1 April 2023, businesses are required to have the following:

A Government Gateway Account -> user ID and password

If they’re already signed up for CDS because they’re using postponed accounting for import VAT and download their certificates via CDS

If they’re not using postponed accounting on imports, paper C79 will no longer be sent and will be available digitally moving forward

Any training or information the business needs to provide to staff

Any changes to the finance processes, for example setting up a new Direct Debit for a duty deferment account, or how to pay into its cash account

Whether the business details (email and business address) match HMRC records or if they need updating

Take Action

Want to know more about how changes to the UK’s customs systems will impact your business and its compliance? Contact us to find out more.

Update: 30 November 2022 by Charles Riordan

ANAF Reverses Position on Grace Period Extension

Romania SAF-T Filing declarations are changing. The draft order extending the grace period for SAF-T will not be implemented. The President of ANAF has confirmed that decision.

The extension originally supported large taxpayers who have had to submit SAF-T since 1 January 2022. ANAF now states that large taxpayers have, on the whole, complied with the original deadlines. This renders the extension “not appropriate.”

ANAF will follow an unofficial policy of leniency for SAF-T submissions. According to a spokesperson, the agency will first give notifications to delinquent taxpayers. Next, they will issue warnings. Fines are a last resort.

The initial six-month grace period for SAF-T hasn’t been formally extended, but it remains in force. Taxpayers will not receive penalties for late or missed filings while the grace period exists.

The grace period applies for six months after the obligation to file SAF-T arises. This obligation begins:

1 January 2022, for “large taxpayers” who were categorised as such in 2021;

1 July 2022, for “large taxpayers” who were only categorised as such in 2022;

1 January 2023, for “medium taxpayers” who were categorised as such in 2021;

1 January 2025 for all taxpayers not in the above categories as of January 1, 2022.

On 1 August 2022, the Romanian National Agency for Fiscal Administration (ANAF) published a draft order extending the current grace period for Standard Audit File for Tax (SAF-T) declarations from six months to twelve months. The order will take effect upon approval and publication in the Official Gazette. At the time of writing, approval and publication are expected shortly.

The Romanian tax authority initially granted the grace period due to the complexity of the country’s SAF-T filing. The SAF-T must include available data from master files, source documents, general ledger entries, and, on a separate cadence, data related to fixed assets and inventory. Because of this complexity, ANAF instituted a six-month grace period, during which taxpayers would not be penalised for late or incorrect filings. The ANAF also implemented SAF-T in phases, with the large taxpayers obliged to file before mid-sized and small taxpayers.

ANAF has acknowledged, however, that even large taxpayers have struggled to meet the technical requirements of the SAF-T declaration. Therefore, with the initial six-month grace period set to expire, ANAF proposes to extend it to alleviate the burden on filers.

The grace period, as before, takes effect from the date a taxpayer is obliged to submit the SAF-T declaration. The obligation for different categories of taxpayers begins:

1 January 2022: for “large taxpayers” who were categorised as such in 2021

1 July 2022: for “large taxpayers” who were only categorised as such in 2022

1 January 2023: for “medium taxpayers” who were categorised as such in 2021

1 January 2025: for all taxpayers not in the above categories as of 1 January 2022.

Romania SAF-T grace period extension

This means that taxpayers who are obliged to file SAF-T in 2022 will now have grace periods extending into 2023 (e.g. 1 January 2023 for “large taxpayers” who were categorised as such in 2021; 1 July 2023 for “large taxpayers” who were only categorised as such in 2022).

The language of the amendment doesn’t limit the twelve-month grace period to large taxpayers, so it is presumed that the grace period will apply to other taxpayers as well. This amendment would extend the grace period for medium taxpayers into 2024 and all others into 2026. Further clarifications on this point may be released in the future.

The rollout of SAF-T in Romania has been eventful, with multiple revisions to both the schema itself and taxpayer obligations. Taxpayers doing business in Romania must ensure that they stay abreast of the latest developments with this declaration, as there will undoubtedly be more to come.

Take Action for Romanian SAF-T

Need to comply with the latest changes in Romanian SAF-T? Speak to our team. Follow us on LinkedIn and Twitter to keep up-to-date with the latest regulatory news and updates.

In Italy, the discipline of transfer pricing states that in intra-group transactions between entities from different countries, where one is resident in Italy, transactions must take place on an arm’s length basis. In other words, transactions are based on freely competitive prices and under comparable circumstances.

Companies carefully treat the transfer pricing adjustments from a corporate income tax perspective. However, less attention is paid from a VAT perspective.

It’s worth mentioning that in most cases, the transfer price adjustments are profitability adjustments (rather than price) of the transactions carried out between associated companies.

However, treating the transfer pricing adjustments as outside the scope of VAT might cause problems in case of a tax authority audit and re-qualification of the transactions.

Italian tax authority clarifications

The issue of transfer pricing adjustments for VAT purposes is not expressly regulated by the Italian legislator, other EU Member State legislators or from an EU VAT legislative point of view. In the absence of an ad hoc provision, reference is made to EU and local legislation, and private and public rulings on a case-by-case analysis.

Regarding public rulings, Italian tax authorities published several responses in 2021.

It is first necessary to verify the existence of a legal relationship with reciprocal benefits between the company and its foreign subsidiaries;

Then, within this relationship, whether there is a direct link between the transfers made through transfer pricing adjustments and any sale of goods and/or provision of services rendered by the company must be verified.

How will this affect my business?

In the 30 December 2021 ruling (no. 884), Italian tax authorities confirmed the adjustments in question were outside the scope of VAT following the transfer pricing adjustments. It stated for subsidiaries “the recognition of an extra cost aimed at lowering their operating margin“, wasn’t “directly related to the original supplies of finished products“.

In this case, at the time of the sale of the goods, the seller applied a provisional price.

That provisional price was then subject to adjustment on a quarterly basis, through the so-called “Profit True Up“. The result could consist either of a claim by the transferor against the transferee or, conversely, transferor’s debt.

In this specific case, Italian tax authorities found a “direct link between the sums determined in the final balance and the supplies” and concluded by determining the relevance of the transfer price adjustments made by the taxpayer for VAT purposes.

Final comments considering other tax authority approaches

Whether or not your business is operating in Italy, the above shows how important the potential VAT implications of transfer pricing adjustments are and the confusion for businesses on how to proceed in different scenarios.

At Sovos we’ve seen more local tax authority audits focused on clarifying if the treatment is valid from a corporate income tax and a VAT perspective.

After a review of the contracts and agreements between the companies and subsidiaries involved, it’s essential to understand whether the transfer pricing adjustments are:

A reallocation of costs or

Adjustments to:

Consideration for an underlying supply or import or

Remuneration for a service provided

Take Action

Speak to our team if you have questions about the latest approach from a VAT perspective on transfer pricing adjustments in Italy, the EU and the UK and the potential solutions to mitigate any risk of audit and penalties.

The European Commission (EC)’s action plan for fair and simple taxation – ’VAT in the Digital Age’- continues to progress. After a public consultation process, the EC has published Final Reports discussing the best options for the European market to fight tax fraud and benefit businesses with the use of technology.

The EC is expected to propose legislative amendments in the VAT Directive this autumn.

Conclusions on VAT reporting and e-invoicing pillar

The report focusing on VAT reporting and e-invoicing evaluates ‘Digital Reporting Requirements (DRR)’. This is any obligation for VAT taxable persons to periodically or continuously submit transaction data digitally to the tax authority, e.g. by use of SAF-T, VAT listing, real-time reporting or e-invoicing.

According to the report, the best policy choice would be the introduction of a DRR in the form of an EU-wide continuous transaction controls (CTC) e-invoicing system covering both intra-EU and domestic transactions. Member States with an existing e-invoicing system would be able to keep this in the short term via a standstill clause, provided they ensure interoperability with the new EU system. However, in the medium term of five to ten years, national e-invoicing systems would be required to converge to the EU system.

An EU-wide CTC e-invoicing system

The report clearly favours the policy option of a full EU harmonisation through a CTC e-invoicing system, meaning the invoice will be submitted to the authorities before or after issuance. The harmonisation focus seems to be primarily on form, with a suggestion of an EU-wide common protocol and format. Whereas important decisions regarding architecture risk being left to the Member States include whether the system will be clearance or simply reporting, whether to leverage an existing domestic B2G platform and the periodicity of the reporting etc. The only requirement on Member States seems to be accepting issued and transmitted e-invoices based on a common protocol and format.

The report suggests aligning the scope of requirements and excluding non-registered taxable persons and those covered by the SME VAT scheme. In the short term, only B2B and B2G transactions are covered, with B2C transactions remaining out of scope.

Finally, the report suggests that to ease the burden on businesses Member States must consider a number of measures such as jointly removing other reporting obligations, providing pre-filled VAT returns, supporting the investment in business automation (especially for SMEs) and providing public support to the adoption of the IT compliance systems

How this will be jointly coordinated isn’t discussed but it doesn’t sound like the EC expects such measures to be harmonised by the EU.

Future expectations

Although the report concludes implementing an EU-wide mandatory e-invoicing system is the best and most future-proof measure, how to design an effective e-invoicing system is not explained in the report and doesn’t seem to be in scope for harmonisation.

However, the design of the e-invoicing system may have an important impact on fiscal and economic results. As the independent expert report ʻNext Generation Model Decentralized CTC and Exchange’ (supported by EESPA, openPEPPOL and other key stakeholder groups) describes, the greatest benefits can only be realised when an e-invoicing system allows businesses to automate other processes as well as invoicing.

It’s a welcome start that the Commission is aiming for an EU-wide CTC e-invoicing scheme. It remains to be seen how effective this harmonisation will be. When Europe’s politicians return from this year’s summer break, we’ll start to gain more insight into the overall feasibility of the Commission’s views.

As a vendor that has implemented CTC and VAT compliance solutions around the world for several decades now, our desire would be for the debate to go beyond interoperability on a data level, so that Europe can take bold steps towards a future that preserves supply chain automation and technological innovation.

Take Action

To find out more about what we believe the future holds, download the 13th Annual Trends. Follow us on LinkedIn and Twitter to keep up-to-date with regulatory news and updates.

A parafiscal tax is a levy on a service or a product which a government charges for a specific purpose. It can be used to financially benefit a particular sector (public and private).

Unlike the drastic changes in Stamp Duty reporting within the Portuguese region, the parafiscal taxes have remained consistent and unchanged for many years. Sovos helps customers report the central parafiscal taxes within the region:

ANPC: National Authority for Civil Protection Contribution

INEM: National Institute of Medical Emergency Contribution

FGA: Motor Guarantee Fund Contribution

PR: National Road Safety Authority Contribution

ASF: Contribution to Insurance and Pension Fund Supervision Authority

The reporting of these taxes is varied and comprehensive which can become confusing for businesses unfamiliar with the requirements. The parafiscal charges, more notably INEM and ANPC, are reported on a monthly declaration structure, whilst PR and FGA are reported on a quarterly structure, and ASF is reported on a half-yearly basis.

ANPC and INEM: monthly reporting

The ANPC and INEM are reported quarterly, and premiums concerning the Azores, Continent (mainland Portugal), and Madeira must be split. This should be identified by the insurer and declared to the corresponding tax authorities.

The tax ANPC (also known as the National Authority for Civil Protection Contribution) can be applied in classes 3 – 13 and is commonly applied at 13% of the fire risk premium. However, this rate is not consistent for all classes of business and can fluctuate accordingly.

Moreover, the tax INEM (also known as the National Institute of Medical Emergency Contribution) can be applied to classes 1, 2, 3, 10 and 18 and at 2.5% of the taxable premium. The rate of 2.5% is consistent between all classes of business and reported on the compliant tax point with Portugal, which is the cash received date (much like ANPC, FGA, PR and ASF). Finally, an annual report for INEM needs to be reported directly to the tax authorities, confirming the total liabilities due throughout the fiscal year.

FGA and PR: quarterly reporting

The reporting of FGA and PR is completed quarterly and submitted on two separate returns. The tax PR is reported at 0.21% of the premium (relating to motor insurance) for classes of business 1, 3 and 10; whilst an FGA rate of 2.5% of the premium (relating to Compulsory Third Party Liability) is only applicable to class 10.

ASF: half yearly reporting

The ASF tax is applied at a tax rate of 0.242% of the taxable premium and is calculated on all classes of business. The rate of 0.242% is confirmed annually by ministerial order within Portugal. So, the tax authority can effectively change the rate annually. It’s also important to mention that a separate rate of 0.048% applies to life insurance and is included within this return.

Take Action

Need to ensure your business is fully compliant with the ever-changing IPT requirements in Portugal? Get in touch with Sovos’ tax experts.

On 22 July, the EU Commission opened four new infringement proceedings against the United Kingdom for allegedly breaching the 2021 Northern Ireland Protocol on conditions related to customs requirements, excise tax and VAT. The EU has brought seven proceedings against the UK over the Protocol since 2021.

The Northern Ireland Protocol

Following the UK’s departure from the EU in 2020, the parties agreed that customs checkpoints on the land border between Northern Ireland and the Republic of Ireland could lead to political instability. The Protocol was an attempt to avoid border posts between the two countries.

Instead, the Protocol ensures customs checks are done in Northern Irish ports before goods are released into the Republic of Ireland. This process effectively created a customs border on the Irish Sea. In addition, the Protocol allows Northern Ireland to follow EU rules on product standards and VAT rules related to goods.

Potential UK Protocol Amendments

The Protocol has been controversial in the UK, as it creates special rules for Northern Ireland that don’t apply in England, Scotland or Wales. Members of the UK’s governing Conservative Party – including Liz Truss, a frontrunner to replace Boris Johnson as UK Prime Minister – have recently introduced a Northern Ireland Protocol Bill that would allow the UK to amend the terms of the Protocol.

Among other things, the draft legislation seeks to remove dispute settlement from the jurisdiction of the Court of Justice of the European Union, authorises “green [fast track] channels” for goods staying within the UK, and allows for UK-wide policies on VAT. Proponents of the bill claim it is necessary to protect the “essential interest” of peace in Northern Ireland.

Protocol Amendment Controversy

However, European Union Representatives have condemned this draft legislation as a potential violation of international law. In its most recent infringement proceedings, the EU alleges that the UK has not substantively implemented parts of the Protocol at all.

In particular, the EU claims that:

The UK is not exercising proper controls over the movement of goods from Northern Ireland to Great Britain

The UK has not yet transposed into national law existing EU rules on excise duties for alcohol and alcoholic beverages; in addition, the UK has given no indication that it will transpose into law new EU rules on excise duties that take effect on 13 February 2023

The UK has not taken the necessary technical measures to implement the Import One Stop Shop scheme (IOSS) for Northern Ireland.

At the time of writing the Northern Ireland Protocol Bill has not yet been adopted by the UK Parliament. It awaits review in the House of Lords. The UK and the EU have stated that further negotiations over the Protocol would be the preferred option. The parties, however, remain far apart on the details.

The EU has set out two months for the UK to respond to the infringement action. Failing any new agreements, the action could lead to possible fines and/or trading sanctions between the parties. Taxpayers conducting cross-border trade between the UK and EU should ensure they stay on top of future developments.

Take Action

Need more information on IOSS and how it could impact your business’s compliance? Get in touch with our team.

Understanding European VAT Compliance

Your guide to making VAT compliance simple

There are many elements to understanding European VAT compliance; our tax experts continually review regulations, compliance rules and tax authority updates to understand VAT requirements across Europe and beyond. This e-book is the result of their research and is ready for you to download. It’s ideal for anyone involved in VAT compliance who is keen to learn more.

Helps you to understand VAT

Covers over 40 jurisdictions within and outside the EU

Download for free

Navigating cross-border and understanding European VAT compliance can be complicated. With requirements varying from country to country it’s important to be prepared for any upcoming changes to ensure continued compliance. The digitization of VAT continues, and our guide will help you understand and be ready for changes.

What this guide to understanding European VAT compliance covers

The guide provides information on understanding European VAT compliance including some of the biggest trends in VAT. We also look at some of the more complex VAT requirements including Intrastat, supply chain management, the EU e-commerce VAT package and VAT for events – all in one easy to understand e-book:

VAT compliance means ensuring that VAT is applied and submitted in the correct format and by the relevant deadline to the relevant tax authority.

Each Member State has its own VAT invoicing and reporting requirements. VAT requirements continue to change so it’s important to be aware of upcoming regulations and prepare in advance to remain compliant with the latest requirements.

VAT is a tax on final consumption, therefore it should not represent a cost to most businesses. VAT is more efficient and less detrimental to economic growth and competitiveness than other taxes

What is a VAT number in Europe?

To obtain a VAT number a company must register for VAT in the EU. Registering for VAT in the EU remains a complicated task, with each Member State having bespoke processes and procedures to obtain a VAT number. VAT reporting includes many elements, from registration to fiscal representation and filing returns. This guide explains the VAT reporting process, as well as upcoming changes that organisations should be aware of to remain VAT compliant.

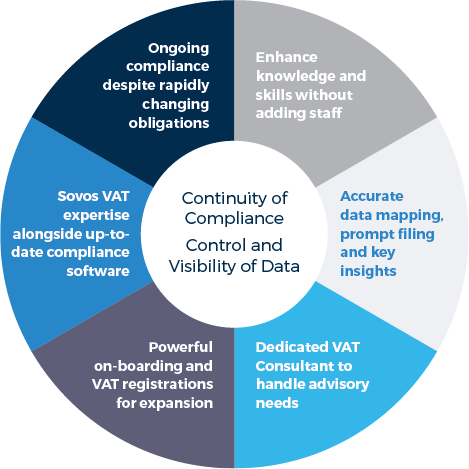

End-to-end, technology-enabled VAT Managed Services ease your compliance workload and mitigate risk wherever you operate today while ensuring you’re ready to handle the VAT requirements in the markets you intend to dominate tomorrow.

Sovos Managed Services can help with a range of VAT compliance requirements, including:

Registration – guidance on country-specific registration requirements to avoid delays

Audits – minimise management time, fees and exposure to penalties or interest

Filing VAT returns – ensure VAT returns are in the correct format and include information required by tax authorities

Managing VAT changes – navigate changes to minimise risk and ensure continued compliance with the latest regulations and updates

Consultancy services – always on-hand to advise and help with queries of any complexity

Give yourself VAT compliance peace of mind.

Ease your VAT compliance workload and mitigate risk wherever you trade with Sovos’ complete end-to-end offering, enabled by our comprehensive software, helping you stay up to date and reducing the burden on your team.

The Philippines continuous transaction controls (CTC) Electronic Invoicing/Receipting System (EIS) has been officially kicked off for the 100 large taxpayers selected by the government to inaugurate the mandate. Although taxpayers were still struggling to meet the new e-invoicing system’s technical requirements just before the go-live date, the Philippines upheld its planned deadline and went live with this pilot on 1 July 2022.

The Philippines roll-out has once again highlighted the challenges of complying with new mandates and shown that readiness is vital.

Together with one of the six initial pilot companies, which started testing early this year, Sovos has developed the first software solution to obtain approval by the EIS to operate e-invoice transmission through the government’s transmission platform. Sovos’ solution is up and running in the Philippines.

Release of new regulations

One day before the EIS go-live, the Philippines tax authority, BIR (Bureau of Internal Revenue), published Revenue Regulations n. 6-2022, 8-2022, and 9-2022, containing the new system’s policies and guidelines and documenting the rules and procedures adopted by the EIS.

While the regulations do not represent news for pilot taxpayers who have successfully implemented their CTC e-invoice reporting systems, the same might not be accurate for those preparing to comply with the new mandate. The legislation officially establishes the country’s e-invoice/receipt issuance and reporting initiative, first introduced in 2018 by the Tax Reform for Acceleration and Inclusion Act (TRAIN), and documents relevant information.

Who needs to comply?

As of 1 July 2022, 100 selected pilot taxpayers have been obliged to issue and transmit e-invoices and e-receipts through the EIS. The BIR is planning a phased roll-out for other taxpayers within the scope of the mandate, starting in 2023, but no official calendar has been announced yet.

Taxpayers covered by the mandate are:

Taxpayers engaged in the export of goods and/or services

Taxpayers engaged in electronic commerce

Taxpayers under the Large Taxpayers Service (LTS)

The mandate requires electronic issuance of invoices (B2B), receipts (B2C), debit and credit notes and transmission through the EIS platform in near real-time, that is, in up to three (3) calendar days counted from issuance date. Documents must be transmitted using the JSON (JavaScript Object Notation) file format.

Issuing and transmitting

Issuance and transmission can be done through the EIS taxpayer portal or using API (Application Programming Interface), in which taxpayers must develop a Sales Data Transmission System and secure certification before operating through the EIS. This entails the application for the EIS Certification and a Permit to Transmit (PTT) by submitting documentation with detailed information about the taxpayer’s system.

Although the regulations state that the submission of printed invoices and receipts is no longer required for taxpayers operating under the EIS, archiving requirements have not been modified. This means that during the 10-year archiving period, taxpayers must retain hard copies of transmitted documents for the first five (5) years, after which exclusive electronic storage is allowed for the remaining time.

Additionally, the legislation states that only the invoices successfully transmitted through the EIS will be accepted for VAT deduction purposes.

Taxpayers were not ready to comply

Many of the 100 pilot taxpayers struggled to comply with the country’s deadline. For this reason, the EIS has allowed alternations to the deadline for certain taxpayers, provided they submit a Sworn Statement detailing the reasons why they are not able to meet the requirement on time and a schedule with the date they intend to comply by, which are subject to the EIS’ approval.

Regarding non-compliance, the regulations state that the tax authority shall impose a penalty for delayed or non-transmission of e-invoices/receipts to the EIS and that unreported sales will be subject to further investigation.

What’s next?

After the pilot program kick-off and legally establishing the CTC framework, the government plans to gradually roll out the mandate to all taxpayers included in the scope in 2023. However, taxpayers who are not in the mandatory scope of the EIS may already opt to enrol in the system and be ready to comply beforehand.

Sovos was the first software provider to become certified, in conjunction with one of the pilot taxpayers, to transmit through the EIS, and is ready to comply with the Philippines CTC e-invoice reporting. Our powerful software combined with our extensive knowledge of the Philippines tax landscape helps companies solve tax for good.