On 30 August 2022, the Ministry of Finance published draft legislation amending the Regulation on the use of the National e-Invoice System (KSeF). The purpose of the draft amendment is to adapt KSeF’s terms of use to the specific conditions that apply to the local government units and the VAT groups that will operate as a new type of VAT taxpayer from 1 January 2023.

The current regulatory status in Poland

The concept of VAT groups was introduced in Poland in October 2021. VAT groups are a legal form of cooperation, a type of taxable entity that exists solely for VAT purposes. On joining a VAT group, a group member becomes part of a new separate VAT taxpayer possessing one Polish tax identification number (NIP).

The regulation on the use of KSeF didn’t take into consideration the uniqueness of the legal nature of the VAT group, as well as the VAT settlements in the local government units. Based on current regulation, the governmental units are treated as a single VAT taxpayer, using one NIP number.

Similarly, in the case of VAT groups, separate VAT taxpayers who create one new taxpayer (a VAT group) use one NIP number. The proposed changes resulted from the ongoing public consultations that took place in December 2021. Additionally, the change was also requested in May 2022 by the Union of Polish Metropolises.

Proposed amendments to the current e-invoice regulation

The draft law provides the possibility to grant additional limited rights for the local government units and members of VAT groups. Moreover, local government units and VAT groups will be able to grant administrative rights, to manage permissions in KSeF, to a natural person who is their representative.

Thanks to such delegated rights, there will be an option to manage authorisations for the local government unit and for the entity that is a member of a VAT group. Moreover, it is significant that a person with such authorisation will not have simultaneous access to invoices in other units within the local government or within other members of a VAT group.

For local government units and VAT groups, granting or withdrawing authorisation to the natural person must be performed electronically. It’s not possible to submit a paper form to notify the competent tax authority.

Remaining issues for KSEF and enforcement date

As mentioned, the proposed amendments are in response to concerns that were raised by the impacted entities. However, they don’t meet all the needs of local government units and VAT groups. For instance, the question of how to assign an inbound electronic invoice to a particular internal unit or member of a VAT group remains open. This is because invoices contain only the data of the taxpayer, which in this case is the local government unit or a VAT group, and not data of the internal unit or member of a VAT group.

The regulation will enter into force 14 days after the date of publication. However, provisions that apply to VAT group members will be effective from 1 January 2023.

With the deadline rapidly approaching, here’s a brief recap.

The Customs Handling of Import and Export Freight (CHIEF) system, which is now nearly 30 years old (it was introduced in 1994), will close in two phases:

Phase one: After 30 September 2022, the ability to make import declarations will end

Phase two: After 31 March 2023, the ability to make export declarations will end

The Customs Declaration Service will serve as the UK’s single customs platform, with all businesses needing to declare all imported and exported goods through the Customs Declaration Service (CDS) after 31 March 2023.

CDS benefits and key changes

As mentioned on the HMRC website, the Customs Declaration Service toolkit gives traders access to the many benefits of the upcoming changes. In summary:

Benefits

Using the latest technology, CDS delivers an enhanced service and user experience

CDS has the capacity and capability to grow in line with the government’s growth agenda, alongside plans to increase the volume of international trade

CDS offers a host of specialist functions and interfaces. Underpinned by modern, cloud-based architecture, it’s fully agile and adjustable

Businesses can declare all goods on one platform simultaneously, regardless of the customer journey. This process reduces operational costs and lessens the administrative burden of running two separate customs systems

Declaration data is transparent and free of charge – businesses can easily access real-time import and export data and check tariffs and financial statements online using dedicated digital dashboards

CDS is designed to be completed digitally.

CDS changes

CDS captures some information differently, and the way the business inputs data is different (additional information and supplementary documents will be required for some commodity codes imported into the UK)

There will be additional methods to make payments of customs duties as follows:

Cash accounts

Duty deferment accounts

Immediate payments

Guarantee accounts

Individual guarantees

CDS enables you to update customs agent permissions online

What does this mean in practice?

To be able to use CDS and import goods into the UK from 1 October 2022 and to export from 1 April 2023, businesses are required to have the following:

A Government Gateway Account -> user ID and password

If they’re already signed up for CDS because they’re using postponed accounting for import VAT and download their certificates via CDS

If they’re not using postponed accounting on imports, paper C79 will no longer be sent and will be available digitally moving forward

Any training or information the business needs to provide to staff

Any changes to the finance processes, for example setting up a new Direct Debit for a duty deferment account, or how to pay into its cash account

Whether the business details (email and business address) match HMRC records or if they need updating

Take Action

Want to know more about how changes to the UK’s customs systems will impact your business and its compliance? Contact us to find out more.

Update: 30 November 2022 by Charles Riordan

ANAF Reverses Position on Grace Period Extension

Romania SAF-T Filing declarations are changing. The draft order extending the grace period for SAF-T will not be implemented. The President of ANAF has confirmed that decision.

The extension originally supported large taxpayers who have had to submit SAF-T since 1 January 2022. ANAF now states that large taxpayers have, on the whole, complied with the original deadlines. This renders the extension “not appropriate.”

ANAF will follow an unofficial policy of leniency for SAF-T submissions. According to a spokesperson, the agency will first give notifications to delinquent taxpayers. Next, they will issue warnings. Fines are a last resort.

The initial six-month grace period for SAF-T hasn’t been formally extended, but it remains in force. Taxpayers will not receive penalties for late or missed filings while the grace period exists.

The grace period applies for six months after the obligation to file SAF-T arises. This obligation begins:

1 January 2022, for “large taxpayers” who were categorised as such in 2021;

1 July 2022, for “large taxpayers” who were only categorised as such in 2022;

1 January 2023, for “medium taxpayers” who were categorised as such in 2021;

1 January 2025 for all taxpayers not in the above categories as of January 1, 2022.

On 1 August 2022, the Romanian National Agency for Fiscal Administration (ANAF) published a draft order extending the current grace period for Standard Audit File for Tax (SAF-T) declarations from six months to twelve months. The order will take effect upon approval and publication in the Official Gazette. At the time of writing, approval and publication are expected shortly.

The Romanian tax authority initially granted the grace period due to the complexity of the country’s SAF-T filing. The SAF-T must include available data from master files, source documents, general ledger entries, and, on a separate cadence, data related to fixed assets and inventory. Because of this complexity, ANAF instituted a six-month grace period, during which taxpayers would not be penalised for late or incorrect filings. The ANAF also implemented SAF-T in phases, with the large taxpayers obliged to file before mid-sized and small taxpayers.

ANAF has acknowledged, however, that even large taxpayers have struggled to meet the technical requirements of the SAF-T declaration. Therefore, with the initial six-month grace period set to expire, ANAF proposes to extend it to alleviate the burden on filers.

The grace period, as before, takes effect from the date a taxpayer is obliged to submit the SAF-T declaration. The obligation for different categories of taxpayers begins:

1 January 2022: for “large taxpayers” who were categorised as such in 2021

1 July 2022: for “large taxpayers” who were only categorised as such in 2022

1 January 2023: for “medium taxpayers” who were categorised as such in 2021

1 January 2025: for all taxpayers not in the above categories as of 1 January 2022.

Romania SAF-T grace period extension

This means that taxpayers who are obliged to file SAF-T in 2022 will now have grace periods extending into 2023 (e.g. 1 January 2023 for “large taxpayers” who were categorised as such in 2021; 1 July 2023 for “large taxpayers” who were only categorised as such in 2022).

The language of the amendment doesn’t limit the twelve-month grace period to large taxpayers, so it is presumed that the grace period will apply to other taxpayers as well. This amendment would extend the grace period for medium taxpayers into 2024 and all others into 2026. Further clarifications on this point may be released in the future.

The rollout of SAF-T in Romania has been eventful, with multiple revisions to both the schema itself and taxpayer obligations. Taxpayers doing business in Romania must ensure that they stay abreast of the latest developments with this declaration, as there will undoubtedly be more to come.

Take Action for Romanian SAF-T

Need to comply with the latest changes in Romanian SAF-T? Speak to our team. Follow us on LinkedIn and Twitter to keep up-to-date with the latest regulatory news and updates.

In Italy, the discipline of transfer pricing states that in intra-group transactions between entities from different countries, where one is resident in Italy, transactions must take place on an arm’s length basis. In other words, transactions are based on freely competitive prices and under comparable circumstances.

Companies carefully treat the transfer pricing adjustments from a corporate income tax perspective. However, less attention is paid from a VAT perspective.

It’s worth mentioning that in most cases, the transfer price adjustments are profitability adjustments (rather than price) of the transactions carried out between associated companies.

However, treating the transfer pricing adjustments as outside the scope of VAT might cause problems in case of a tax authority audit and re-qualification of the transactions.

Italian tax authority clarifications

The issue of transfer pricing adjustments for VAT purposes is not expressly regulated by the Italian legislator, other EU Member State legislators or from an EU VAT legislative point of view. In the absence of an ad hoc provision, reference is made to EU and local legislation, and private and public rulings on a case-by-case analysis.

Regarding public rulings, Italian tax authorities published several responses in 2021.

It is first necessary to verify the existence of a legal relationship with reciprocal benefits between the company and its foreign subsidiaries;

Then, within this relationship, whether there is a direct link between the transfers made through transfer pricing adjustments and any sale of goods and/or provision of services rendered by the company must be verified.

How will this affect my business?

In the 30 December 2021 ruling (no. 884), Italian tax authorities confirmed the adjustments in question were outside the scope of VAT following the transfer pricing adjustments. It stated for subsidiaries “the recognition of an extra cost aimed at lowering their operating margin“, wasn’t “directly related to the original supplies of finished products“.

In this case, at the time of the sale of the goods, the seller applied a provisional price.

That provisional price was then subject to adjustment on a quarterly basis, through the so-called “Profit True Up“. The result could consist either of a claim by the transferor against the transferee or, conversely, transferor’s debt.

In this specific case, Italian tax authorities found a “direct link between the sums determined in the final balance and the supplies” and concluded by determining the relevance of the transfer price adjustments made by the taxpayer for VAT purposes.

Final comments considering other tax authority approaches

Whether or not your business is operating in Italy, the above shows how important the potential VAT implications of transfer pricing adjustments are and the confusion for businesses on how to proceed in different scenarios.

At Sovos we’ve seen more local tax authority audits focused on clarifying if the treatment is valid from a corporate income tax and a VAT perspective.

After a review of the contracts and agreements between the companies and subsidiaries involved, it’s essential to understand whether the transfer pricing adjustments are:

A reallocation of costs or

Adjustments to:

Consideration for an underlying supply or import or

Remuneration for a service provided

Take Action

Speak to our team if you have questions about the latest approach from a VAT perspective on transfer pricing adjustments in Italy, the EU and the UK and the potential solutions to mitigate any risk of audit and penalties.

The European Commission (EC)’s action plan for fair and simple taxation – ’VAT in the Digital Age’- continues to progress. After a public consultation process, the EC has published Final Reports discussing the best options for the European market to fight tax fraud and benefit businesses with the use of technology.

The EC is expected to propose legislative amendments in the VAT Directive this autumn.

Conclusions on VAT reporting and e-invoicing pillar

The report focusing on VAT reporting and e-invoicing evaluates ‘Digital Reporting Requirements (DRR)’. This is any obligation for VAT taxable persons to periodically or continuously submit transaction data digitally to the tax authority, e.g. by use of SAF-T, VAT listing, real-time reporting or e-invoicing.

According to the report, the best policy choice would be the introduction of a DRR in the form of an EU-wide continuous transaction controls (CTC) e-invoicing system covering both intra-EU and domestic transactions. Member States with an existing e-invoicing system would be able to keep this in the short term via a standstill clause, provided they ensure interoperability with the new EU system. However, in the medium term of five to ten years, national e-invoicing systems would be required to converge to the EU system.

An EU-wide CTC e-invoicing system

The report clearly favours the policy option of a full EU harmonisation through a CTC e-invoicing system, meaning the invoice will be submitted to the authorities before or after issuance. The harmonisation focus seems to be primarily on form, with a suggestion of an EU-wide common protocol and format. Whereas important decisions regarding architecture risk being left to the Member States include whether the system will be clearance or simply reporting, whether to leverage an existing domestic B2G platform and the periodicity of the reporting etc. The only requirement on Member States seems to be accepting issued and transmitted e-invoices based on a common protocol and format.

The report suggests aligning the scope of requirements and excluding non-registered taxable persons and those covered by the SME VAT scheme. In the short term, only B2B and B2G transactions are covered, with B2C transactions remaining out of scope.

Finally, the report suggests that to ease the burden on businesses Member States must consider a number of measures such as jointly removing other reporting obligations, providing pre-filled VAT returns, supporting the investment in business automation (especially for SMEs) and providing public support to the adoption of the IT compliance systems

How this will be jointly coordinated isn’t discussed but it doesn’t sound like the EC expects such measures to be harmonised by the EU.

Future expectations

Although the report concludes implementing an EU-wide mandatory e-invoicing system is the best and most future-proof measure, how to design an effective e-invoicing system is not explained in the report and doesn’t seem to be in scope for harmonisation.

However, the design of the e-invoicing system may have an important impact on fiscal and economic results. As the independent expert report ʻNext Generation Model Decentralized CTC and Exchange’ (supported by EESPA, openPEPPOL and other key stakeholder groups) describes, the greatest benefits can only be realised when an e-invoicing system allows businesses to automate other processes as well as invoicing.

It’s a welcome start that the Commission is aiming for an EU-wide CTC e-invoicing scheme. It remains to be seen how effective this harmonisation will be. When Europe’s politicians return from this year’s summer break, we’ll start to gain more insight into the overall feasibility of the Commission’s views.

As a vendor that has implemented CTC and VAT compliance solutions around the world for several decades now, our desire would be for the debate to go beyond interoperability on a data level, so that Europe can take bold steps towards a future that preserves supply chain automation and technological innovation.

Take Action

To find out more about what we believe the future holds, download the 13th Annual Trends. Follow us on LinkedIn and Twitter to keep up-to-date with regulatory news and updates.

A parafiscal tax is a levy on a service or a product which a government charges for a specific purpose. It can be used to financially benefit a particular sector (public and private).

Unlike the drastic changes in Stamp Duty reporting within the Portuguese region, the parafiscal taxes have remained consistent and unchanged for many years. Sovos helps customers report the central parafiscal taxes within the region:

ANPC: National Authority for Civil Protection Contribution

INEM: National Institute of Medical Emergency Contribution

FGA: Motor Guarantee Fund Contribution

PR: National Road Safety Authority Contribution

ASF: Contribution to Insurance and Pension Fund Supervision Authority

The reporting of these taxes is varied and comprehensive which can become confusing for businesses unfamiliar with the requirements. The parafiscal charges, more notably INEM and ANPC, are reported on a monthly declaration structure, whilst PR and FGA are reported on a quarterly structure, and ASF is reported on a half-yearly basis.

ANPC and INEM: monthly reporting

The ANPC and INEM are reported quarterly, and premiums concerning the Azores, Continent (mainland Portugal), and Madeira must be split. This should be identified by the insurer and declared to the corresponding tax authorities.

The tax ANPC (also known as the National Authority for Civil Protection Contribution) can be applied in classes 3 – 13 and is commonly applied at 13% of the fire risk premium. However, this rate is not consistent for all classes of business and can fluctuate accordingly.

Moreover, the tax INEM (also known as the National Institute of Medical Emergency Contribution) can be applied to classes 1, 2, 3, 10 and 18 and at 2.5% of the taxable premium. The rate of 2.5% is consistent between all classes of business and reported on the compliant tax point with Portugal, which is the cash received date (much like ANPC, FGA, PR and ASF). Finally, an annual report for INEM needs to be reported directly to the tax authorities, confirming the total liabilities due throughout the fiscal year.

FGA and PR: quarterly reporting

The reporting of FGA and PR is completed quarterly and submitted on two separate returns. The tax PR is reported at 0.21% of the premium (relating to motor insurance) for classes of business 1, 3 and 10; whilst an FGA rate of 2.5% of the premium (relating to Compulsory Third Party Liability) is only applicable to class 10.

ASF: half yearly reporting

The ASF tax is applied at a tax rate of 0.242% of the taxable premium and is calculated on all classes of business. The rate of 0.242% is confirmed annually by ministerial order within Portugal. So, the tax authority can effectively change the rate annually. It’s also important to mention that a separate rate of 0.048% applies to life insurance and is included within this return.

Take Action

Need to ensure your business is fully compliant with the ever-changing IPT requirements in Portugal? Get in touch with Sovos’ tax experts.

On 22 July, the EU Commission opened four new infringement proceedings against the United Kingdom for allegedly breaching the 2021 Northern Ireland Protocol on conditions related to customs requirements, excise tax and VAT. The EU has brought seven proceedings against the UK over the Protocol since 2021.

The Northern Ireland Protocol

Following the UK’s departure from the EU in 2020, the parties agreed that customs checkpoints on the land border between Northern Ireland and the Republic of Ireland could lead to political instability. The Protocol was an attempt to avoid border posts between the two countries.

Instead, the Protocol ensures customs checks are done in Northern Irish ports before goods are released into the Republic of Ireland. This process effectively created a customs border on the Irish Sea. In addition, the Protocol allows Northern Ireland to follow EU rules on product standards and VAT rules related to goods.

Potential UK Protocol Amendments

The Protocol has been controversial in the UK, as it creates special rules for Northern Ireland that don’t apply in England, Scotland or Wales. Members of the UK’s governing Conservative Party – including Liz Truss, a frontrunner to replace Boris Johnson as UK Prime Minister – have recently introduced a Northern Ireland Protocol Bill that would allow the UK to amend the terms of the Protocol.

Among other things, the draft legislation seeks to remove dispute settlement from the jurisdiction of the Court of Justice of the European Union, authorises “green [fast track] channels” for goods staying within the UK, and allows for UK-wide policies on VAT. Proponents of the bill claim it is necessary to protect the “essential interest” of peace in Northern Ireland.

Protocol Amendment Controversy

However, European Union Representatives have condemned this draft legislation as a potential violation of international law. In its most recent infringement proceedings, the EU alleges that the UK has not substantively implemented parts of the Protocol at all.

In particular, the EU claims that:

The UK is not exercising proper controls over the movement of goods from Northern Ireland to Great Britain

The UK has not yet transposed into national law existing EU rules on excise duties for alcohol and alcoholic beverages; in addition, the UK has given no indication that it will transpose into law new EU rules on excise duties that take effect on 13 February 2023

The UK has not taken the necessary technical measures to implement the Import One Stop Shop scheme (IOSS) for Northern Ireland.

At the time of writing the Northern Ireland Protocol Bill has not yet been adopted by the UK Parliament. It awaits review in the House of Lords. The UK and the EU have stated that further negotiations over the Protocol would be the preferred option. The parties, however, remain far apart on the details.

The EU has set out two months for the UK to respond to the infringement action. Failing any new agreements, the action could lead to possible fines and/or trading sanctions between the parties. Taxpayers conducting cross-border trade between the UK and EU should ensure they stay on top of future developments.

Take Action

Need more information on IOSS and how it could impact your business’s compliance? Get in touch with our team.

Understanding European VAT Compliance

Your guide to making VAT compliance simple

There are many elements to understanding European VAT compliance; our tax experts continually review regulations, compliance rules and tax authority updates to understand VAT requirements across Europe and beyond. This e-book is the result of their research and is ready for you to download. It’s ideal for anyone involved in VAT compliance who is keen to learn more.

Helps you to understand VAT

Covers over 40 jurisdictions within and outside the EU

Download for free

Navigating cross-border and understanding European VAT compliance can be complicated. With requirements varying from country to country it’s important to be prepared for any upcoming changes to ensure continued compliance. The digitization of VAT continues, and our guide will help you understand and be ready for changes.

What this guide to understanding European VAT compliance covers

The guide provides information on understanding European VAT compliance including some of the biggest trends in VAT. We also look at some of the more complex VAT requirements including Intrastat, supply chain management, the EU e-commerce VAT package and VAT for events – all in one easy to understand e-book:

VAT compliance means ensuring that VAT is applied and submitted in the correct format and by the relevant deadline to the relevant tax authority.

Each Member State has its own VAT invoicing and reporting requirements. VAT requirements continue to change so it’s important to be aware of upcoming regulations and prepare in advance to remain compliant with the latest requirements.

VAT is a tax on final consumption, therefore it should not represent a cost to most businesses. VAT is more efficient and less detrimental to economic growth and competitiveness than other taxes

What is a VAT number in Europe?

To obtain a VAT number a company must register for VAT in the EU. Registering for VAT in the EU remains a complicated task, with each Member State having bespoke processes and procedures to obtain a VAT number. VAT reporting includes many elements, from registration to fiscal representation and filing returns. This guide explains the VAT reporting process, as well as upcoming changes that organisations should be aware of to remain VAT compliant.

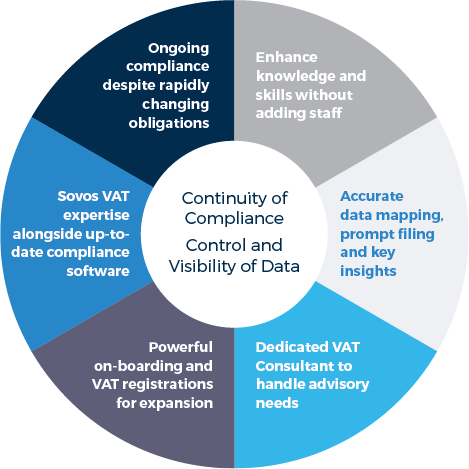

End-to-end, technology-enabled VAT Managed Services ease your compliance workload and mitigate risk wherever you operate today while ensuring you’re ready to handle the VAT requirements in the markets you intend to dominate tomorrow.

Sovos Managed Services can help with a range of VAT compliance requirements, including:

Registration – guidance on country-specific registration requirements to avoid delays

Audits – minimise management time, fees and exposure to penalties or interest

Filing VAT returns – ensure VAT returns are in the correct format and include information required by tax authorities

Managing VAT changes – navigate changes to minimise risk and ensure continued compliance with the latest regulations and updates

Consultancy services – always on-hand to advise and help with queries of any complexity

Give yourself VAT compliance peace of mind.

Ease your VAT compliance workload and mitigate risk wherever you trade with Sovos’ complete end-to-end offering, enabled by our comprehensive software, helping you stay up to date and reducing the burden on your team.

The Philippines continuous transaction controls (CTC) Electronic Invoicing/Receipting System (EIS) has been officially kicked off for the 100 large taxpayers selected by the government to inaugurate the mandate. Although taxpayers were still struggling to meet the new e-invoicing system’s technical requirements just before the go-live date, the Philippines upheld its planned deadline and went live with this pilot on 1 July 2022.

The Philippines roll-out has once again highlighted the challenges of complying with new mandates and shown that readiness is vital.

Together with one of the six initial pilot companies, which started testing early this year, Sovos has developed the first software solution to obtain approval by the EIS to operate e-invoice transmission through the government’s transmission platform. Sovos’ solution is up and running in the Philippines.

Release of new regulations

One day before the EIS go-live, the Philippines tax authority, BIR (Bureau of Internal Revenue), published Revenue Regulations n. 6-2022, 8-2022, and 9-2022, containing the new system’s policies and guidelines and documenting the rules and procedures adopted by the EIS.

While the regulations do not represent news for pilot taxpayers who have successfully implemented their CTC e-invoice reporting systems, the same might not be accurate for those preparing to comply with the new mandate. The legislation officially establishes the country’s e-invoice/receipt issuance and reporting initiative, first introduced in 2018 by the Tax Reform for Acceleration and Inclusion Act (TRAIN), and documents relevant information.

Who needs to comply?

As of 1 July 2022, 100 selected pilot taxpayers have been obliged to issue and transmit e-invoices and e-receipts through the EIS. The BIR is planning a phased roll-out for other taxpayers within the scope of the mandate, starting in 2023, but no official calendar has been announced yet.

Taxpayers covered by the mandate are:

Taxpayers engaged in the export of goods and/or services

Taxpayers engaged in electronic commerce

Taxpayers under the Large Taxpayers Service (LTS)

The mandate requires electronic issuance of invoices (B2B), receipts (B2C), debit and credit notes and transmission through the EIS platform in near real-time, that is, in up to three (3) calendar days counted from issuance date. Documents must be transmitted using the JSON (JavaScript Object Notation) file format.

Issuing and transmitting

Issuance and transmission can be done through the EIS taxpayer portal or using API (Application Programming Interface), in which taxpayers must develop a Sales Data Transmission System and secure certification before operating through the EIS. This entails the application for the EIS Certification and a Permit to Transmit (PTT) by submitting documentation with detailed information about the taxpayer’s system.

Although the regulations state that the submission of printed invoices and receipts is no longer required for taxpayers operating under the EIS, archiving requirements have not been modified. This means that during the 10-year archiving period, taxpayers must retain hard copies of transmitted documents for the first five (5) years, after which exclusive electronic storage is allowed for the remaining time.

Additionally, the legislation states that only the invoices successfully transmitted through the EIS will be accepted for VAT deduction purposes.

Taxpayers were not ready to comply

Many of the 100 pilot taxpayers struggled to comply with the country’s deadline. For this reason, the EIS has allowed alternations to the deadline for certain taxpayers, provided they submit a Sworn Statement detailing the reasons why they are not able to meet the requirement on time and a schedule with the date they intend to comply by, which are subject to the EIS’ approval.

Regarding non-compliance, the regulations state that the tax authority shall impose a penalty for delayed or non-transmission of e-invoices/receipts to the EIS and that unreported sales will be subject to further investigation.

What’s next?

After the pilot program kick-off and legally establishing the CTC framework, the government plans to gradually roll out the mandate to all taxpayers included in the scope in 2023. However, taxpayers who are not in the mandatory scope of the EIS may already opt to enrol in the system and be ready to comply beforehand.

Sovos was the first software provider to become certified, in conjunction with one of the pilot taxpayers, to transmit through the EIS, and is ready to comply with the Philippines CTC e-invoice reporting. Our powerful software combined with our extensive knowledge of the Philippines tax landscape helps companies solve tax for good.

VAT determination is challenging for any company with complex transactions in its supply chains. Business sectors such as manufacturing, pharmaceutical, construction, retail and logistics are particularly overburdened trying to manage this requirement.

Limitations in SAP functionality has created another level of complexity. Custom coding in SAP is often required to achieve reliable determination decisions and the need for ongoing customisation makes maintaining master data difficult.

These challenges typically prevent companies from achieving a desirable level of transparency across their determination process. When a business deals with complex transactions, often due to multi jurisdictional supply chains, accurate VAT determination is vital. Any errors at this point can lead to severe consequences for accounting accuracy and financial resilience.

Reduce Your Operational Burden

A powerful suite of SAP-certified add-ons automate VAT determination, simplifies master data maintenance and mitigates the compliance risks caused by inaccurate data.

Deliver enhanced SAP functionality that alleviates pressure for both tax and IT professionals to meet your ever-evolving VAT requirements.

Benefits of Automating Your VAT Determination

Reduce costs and complexity

Handle future changes without specialist SAP experts, and reduce the technical maintenance burden to free SAP-resources to focus on other projects

Reduce tax compliance risk

Deliver accurate and reliable tax decisions though intelligent, automated logic directly embedded within SAP processes

Mitigate tax audit risk

Identify errors by comparing general ledger and account balances with postings against specific tax codes

Fortify overall compliance

Drive accuracy of data in downstream processes for periodic reporting including VAT Returns, EC Sales Lists, Intrastat Declarations and SAF-T

Future-proof strategy

The trend towards digitisation continues with governments becoming increasingly present in your data. By partnering with Sovos, you gain greater clarity for VAT determination and peace of mind that your business is safeguarded from risk of future audits

Maximise operational efficiency

Increase invoicing accuracy with robust determination decisions, so billing teams don't need to correct and reissue invoices. Similarly, when invoices received by a company are accurate they can be processed without delay

The EU and the UK use the Economic Operators Registration and Identification System (EORI) to identify traders.

What is an EORI number?

Businesses and people wishing to trade in the EU and the UK must use the EORI number as an identification number in all customs procedures when exchanging information with customs administrations. The EU has one standard identification number across the EU, while the UK requires a separate GB EORI number for trade in the UK post-Brexit.

The purpose of having one standard ID in the EU is that it creates efficiency for both traders and the customs authorities. However, it’s vital to ensure all aspects of the system are considered.

Who needs an EORI number?

The primary need for an EORI number is to be able to lodge a customs declaration for both imports and exports. Guidance is that a trader should obtain an EORI number in the first country of import or export. Carriers will also require an EORI number.

EORI number format

The EORI number exists in two parts:

The country code of the issuing Member State; followed by

A code or number that is unique in the Member State

The UK has also adopted this format, with both GB EORI numbers for trade into Great Britain (GB) and an XI EORI number for trade via the Northern Ireland protocol. The UK and EU have online databases where it is possible to check the status of an EORI number.

GB and XI EORI numbers

Since the UK left the EU, it is now required to have a separate GB EORI number to import and export from GB. This number will not be valid in the EU. However, should businesses be trading from Northern Ireland, then due to the Northern Ireland protocol, it is possible to apply for an XI EORI number to import into the EU.

Initially, after the introduction of the XI prefix, there were several reported issues. They included tax authorities being unable to recognise XI EORI numbers or link them to existing EU VAT numbers. Often it is the case that businesses have found it simpler to cancel an XI EORI number and apply for an EU EORI number in a Member State, particularly if that Member State is the main point of entry for imports into the EU.

Practical issues around EORIs

Some of the most common issues we see at Sovos include:

Businesses not having an EORI before starting an import and goods being stuck at the customs border.

Traders being told they need an EORI number in every Member State of import – however, this is not the case, and usually the reason for the customs delay is another matter.

Businesses not linking the EU EORI to their other EU VAT registrations.

Traders being told they need an EU address for the EORI – this is normally related to indirect customs representation, which we covered in our last article.

Businesses thinking it’s possible to use their carrier’s EORI number.

How Sovos can help

Sovos provides an EORI registration service for traders who must apply for an EORI number. We can also link any existing EU VAT numbers to the EORI to ensure that customs declarations can be logged correctly, ensuring a smooth process and avoiding delays. You can find more information about EU VAT and the EU VAT e-commerce package here.

According to European Customs Law, non-EU established businesses must appoint a representative for customs purposes when importing goods into the EU. In particular, the Union Customs Code establishes that non-EU resident businesses must appoint an indirect representative.

At the end of the Brexit transitionary period, many UK businesses suddenly needed to appoint an indirect representative to clear goods into the EU. In this article, we will look in further detail at this requirement’s challenges.

Who can act as an indirect representative?

Indirect representation implies that agents are jointly and severally liable for any customs debt (import or export duties), which is why it’s harder for businesses to find freight companies and customs brokers willing to act on their behalf than for direct representation imports.

The conditions to be an indirect representative are that the customs agent must have a registered office or permanent establishment in the EU. An agent would require a Power of Attorney that enables them to act for the company. The main characteristic of indirect representation is that the agent will act in their own name but on behalf of the company that appointed them, essentially transferring the rights and obligations of customs procedures to the representative.

On the other hand, agents act in the name and on behalf of the company in direct representation.

Joint responsibility of the indirect representative

In addition to the customs implications, agents acting as the importer of record or declarant may also be considered liable for complying with regulatory requirements. For example, any error in the declarations (ex. Article 77 paragraph 3 Union Customs Code (UCC), if the agent was aware of incorrect information or if they “should have known better”).

The European Court of Justice recently expressed its opinion on this matter with the ruling on the case C-714/20, UI Srl. This ruling determined that the indirect representative is jointly and severally liable from a customs law perspective, but not for VAT (contrary to a previous interpretation of Article 77 (3) UCC). The court specified that it’s up to the Member States to expressly determine if other persons, such as indirect representatives, may be considered jointly and severally liable for VAT of their importer clients. However, according to the principle of legal certainty, this should be clearly expressed in the local legislation before courts can enforce said responsibility.

What are the options for UK businesses?

Making the final client importer of records using DAP Incoterms for sales rather than DDP (Delivered Duty Paid basis – where the seller is responsible for clearing the goods and payment of duties and taxes amongst other obligations). This will imply that the importing obligations are shifted to the buyer receiving the goods in the importing country. In practice, however, this may not be an option considering the additional administrative and economic burden this will impose on end customers.

To establish a presence in the EU. For example, setting up a subsidiary that can act as the importer of record, then find a customs agent that can act as a direct representative.

Appoint a representative in specific countries, such as the Netherlands, where the application for an Article 23 import license (which allows applying a reverse charge to the imports reported) may further diminish the representative’s liability. In conjunction with the recent decision of the European Court of Justice, this may make it easier for UK businesses to find an agent willing to represent them indirectly and limit fees and guarantees that they may be required to provide.

For these options, each alternative solution will have economic and administrative implications to be considered. It is recommended that businesses carefully review their overall strategy before deciding what can be adjusted to comply with customs formalities.

Take Action

Contact Sovos’ team of VAT experts for help with meeting VAT compliance obligations.

Serbia E-invoicing

Aligning with other Eastern European countries such as Poland and Romania, Serbia has forged a path towards mandating e-invoicing for B2B and B2G transactions.

This page has the updates you need to learn about Serbia’s electronic invoicing journey. Be sure to bookmark it to stay informed as rules and regulations change.

In Serbia, it has been mandatory to issue and receive electronic invoices for B2B transactions since 1 January 2023.

On the same date, select taxpayers became obliged to report their VAT to the Serbian tax authorities via the national e-invoicing system, Sistem eFaktura (SEF).

E-invoices must be in the UBL 2.1 format and securely stored for 10 years.

B2G e-invoicing in Serbia

Since 1 May 2022, all suppliers to the Serbian public sector must send invoices electronically, and from 1 July 2022, the Serbian public sector must send e-invoices to companies.

As a result, B2G and G2B transactions have been under an e-invoicing mandate since 2022.

Electronic invoices issued or received by a public entity, such as a government agency, are permanently stored in the Serbian electronic invoicing system (SEF).

Timeline of e-invoicing adoption

May 2021: Law on Electronic Invoicing came into force, introducing the SEF CTC platform

1 May 2022:All suppliers in the public sector must send invoices electronically, and the Serbian government must be able to receive and store them

1 July 2022: Serbian public entities are obliged to send e-invoices to companies

1 January 2023: E-invoicing is mandated for B2B transactions

28 November 2024: Law on Electronic Invoicing is amended to include changes to electronic recording of VAT, tax returns and penalties

Setting up e-invoicing in Serbia with Sovos

Compliance can be resource-heavy.

Consider the numerous mandates across every country you operate in, as well as the fact that these regulations change over time, and it becomes clear that it takes a lot of time, energy and headspace to stay compliant.

If you operate in Serbia and want to ensure you are on the right side of the rules, speak with Sovos. We can serve as your sole tax and e-invoicing compliance partner, freeing you up to focus on what truly matters.

No, B2C transactions are currently excluded from mandatory e-invoicing; however, plans are in place to integrate the current eFiscalization system with SEF.

Sovos recently hosted an online webinar on VAT recovery where we covered reciprocity agreements between the UK and EU Member States when making 13th Directive VAT refund claims. One of the questions that kept coming up is what are reciprocity agreements and why do they matter?

Reciprocity

When making 13th Directive refund claims, each EU Member State has different rules or conditions to meet before agreeing to a VAT refund. One of the conditions that EU Member States may require is a reciprocity agreement. A reciprocity agreement is a deal to reciprocate VAT refunds between two countries.

Therefore, VAT is only refundable when a similar tax is refundable for local businesses in the applicant’s country. For example, suppose a Spanish business was allowed to obtain a VAT refund in Norway through a similar scheme to the 13 Directive. In that case, Spain would likely have reciprocity with Norway and will allow the Norwegian businesses to make a 13th Directive Refund Claim in Spain.

There are currently around 19 EU Member States that require reciprocity agreements for non-EU businesses to make VAT refund claims. Of those, Greece and Slovenia currently only have reciprocity agreements with two countries (Norway and Switzerland), whilst Italy has three (Norway, Switzerland and Israel). When making EU VAT refund claims, businesses should review reciprocity and not assume they will automatically be approved.

UK businesses

Before Brexit, UK businesses could make VAT refund claims through the EU VAT Refund Directive (also known as the 8th Directive) which was built to allow reciprocity freedom for all EU Member States. However, post-Brexit, this mechanism for VAT refund claims no longer applied, and the UK fell within the 13th Directive Refund Scheme as a non-EU business.

Whilst the UK and EU have a Free Trade and Cooperation Agreement in place, there was no specific mention of reciprocity in VAT refund claims as these should be agreed between those particular EU Member States and the UK. Therefore, it may be more difficult for UK businesses, that make refund claims around the EU, to recover VAT incurred in some countries.

Regarding current reciprocity agreements with the UK, the only official announcements we have seen to date have been from Germany, Spain and Hungary. However, we are aware of ongoing discussions between the UK and other EU Member States.

HMRC states they will only refuse a claim if the reciprocal country has a scheme for refunding taxes but refuses to allow UK traders a refund. Therefore, HMRC is willing to allow VAT recovery in the UK for EU businesses providing UK businesses receive the same treatment as the EU. It would therefore be in the interests of EU Member States to allow VAT recovery for UK businesses for businesses in their own country to benefit from the same treatment.

Why does it matter?

Most EU Member States require reciprocity when making VAT refund claims. Therefore, the law of reciprocity is an integral factor when looking to make a VAT refund claim in any jurisdiction. It’s important to understand these reciprocity laws to prevent wasting time and money on making a VAT refund claim from a country that doesn’t allow it.

Our previous articles covered audit trends we have noticed at Sovos and common triggers of a VAT audit. This article discusses the best practices on how to prepare for a VAT audit.

Each country and jurisdiction may have different laws and requirements related to the VAT audit process. Tax authorities can carry out audits in person or by correspondence, the latter often being the case for non-established businesses in the country in question.

A business may be audited at random or because there are reasons for the tax authority to believe that there is a problem with the company’s VAT return.

Generally speaking, authorities use audits and inspections to verify the accuracy of taxpayers’ declarations, identify possible errors or underpayments, and approve refunds.

As discussed in our previous article, to understand how to best prepare for a VAT audit, it’s essential to identify the reason why the audit was initiated.

What items are needed for a VAT audit?

Although specific checklists are available depending on the country of the audit, there are several actions that a business can carry out to prepare for an VAT audit. The most important of which is to collect documents and answers in advance. Frequently requested items during an audit include:

VAT ledgers containing details of the transactions reported

Related copies of incoming and outgoing invoices and pro-forma for intra-community movement of own goods

Proof of transport of the goods: Two independent items should be provided in particular for intra-community dispatches, proving the right to apply the 0% tax rate (such as signed CMR consignment notes, bill of lading, carrier invoices, insurance policies, warehouse receipts, proof of payment for the transport of the goods, etc.)

Proof of payment of the transactions reported, with particular attention to the payment of purchase invoices and the repayment of credit notes issued to clients and customers

Contracts with suppliers

Description of the business activities and goods flow

It is important that records of the above-listed documents, where applicable, are kept in line with local record keeping requirements. The need to prepare these documents in advance and the ability to produce them quickly becomes essential when a company is, for example, due to request the refund of VAT credits, to submit a de-registration or has, in general, any reason to expect for an audit to be initiated.

Authorities can open a cross check of activities with the company’s customers and suppliers, which will be initiated in parallel to the audit to verify that the information provided from both sides is consistent. Therefore, it is recommended to inform suppliers about any ongoing audit, communicate any questions or clarify outstanding queries. If, for example, a correction of invoices appears to be necessary, these should be finalised already in preparation for the VAT audit.

The tax authorities may impose very short and strict deadlines once an audit is initiated. Although it may be possible to request an extension, it is not necessarily guaranteed to be granted. In certain circumstances, authorities may impose penalties for late responses. Providing a clear and understandable set of documents to the tax office queries is essential to avoid any detrimental effects.

Why it makes sense to plan ahead

The advantages of preparing for a VAT audit can be summarised as follows:

Minimise the resources required to collect the necessary documents once an audit is initiated

Quicker completion of the audit, avoiding the necessity to request deadline extensions and delays in receiving VAT refund, if applicable

Ability to identify, rectify and voluntarily disclose any error that might emerge from preliminary reviews of the documents collected ahead of the audit initiation

Potential penalties reduction

Whether a business decides to handle the audit in-house or request the support of an external advisor, it is essential to consider the consequences of the audit, especially if high amounts of VAT to recover are at stake. In the event of an audit, the main objective should be to resolve it successfully and quickly, limiting as much as possible any detrimental impact to the business.

Indonesia made e-invoicing mandatory for all VAT-registered taxpayers on 1 July 2016, expanding upon its initial e-Faktur rollout in Bali and Java from 1 July 2015.

With its own official e-invoicing system and mandate, Indonesia has plenty for taxpayers to learn and comply with. This page is the ideal starting point for understanding Indonesia e-invoicing.

After experiencing challenges in its tax control system, Indonesia adopted an e‑invoicing system locally known as e‑Faktur Pajak. Leveraging data reported in real-time via continuous transaction controls (CTCs) allows the Indonesian tax authorities to reduce occurrences of fraud whilst helping to close the tax gap.

Introduced in 2014 and effective from 2016, Indonesia’s e‑invoicing system seeks to combat the tax gap. Indonesia’s solution was the implementation of an invoice clearance system, where invoices must be approved by the local tax authority prior to being sent to a customer.

E-invoicing is mandatory for all corporate VAT taxpayers. It’s compulsory for all invoices to be processed and issued electronically through the government’s official system, eFaktur.

Also known as tax invoices, e-invoices in Indonesia are typically issued for:

Delivery of taxable goods (Barang Kena Pajak)

Rendering of taxable services (Jasa Kena Pajak)

Advance payment of taxable goods or services

eFaktur e-invoices should be created by applications approved by Indonesia’s Director of Taxation (DGT). Options include client desktop, web-based and host-to-host applications. Electronic invoices need to be secured using an electronic signature, and taxpayers need electronic certificates to verify their identity—the latter need to be renewed every two years. Validated invoices receive a QR code from the DGT as proof of authenticity.

It’s worth noting that the VAT return submission has been integrated with eFaktur, and VAT returns are typically required to be submitted monthly via the platform.

Timeline of e-invoicing adoption in Indonesia

Indonesia’s e-invoicing journey has plenty of key moments:

1 July 2014: e-Faktur is introduced

1 July 2015: e-Faktur becomes mandatory for VAT-registered taxpayers in Bali and Java

1 July 2016: e-Faktur Pajak became effective for all VAT-registered taxpayers based in the country

1 October 2020: New e-Faktur Pajak version 3.0 released

31 July 2024: The development of a Core Tax System (PSIAP) is announced to automate and digitise tax administration services

Penalties: What happens if I don’t comply with e-invoicing in Indonesia?

Indonesia penalises taxpayers who fail to meet their compliance obligations. For example, if a tax invoice is not issued (or is issued late or invalid), the taxpayer will be fined 1% of the VAT base.

All VAT-registered businesses in Indonesia must send and receive e-invoices via the e-Faktur platform. They must submit invoices for validation before sending to the buyer.

Yes, the e-Faktur system is integrated with VAT reporting. The introduction of e-faktur v3.0 in October 2020 enabled the auto-population of VAT returns for taxpayers in the scope of the local e-invoicing mandate.

Setting up e-invoicing in Indonesia with Sovos

E-invoicing is a global trend, though your requirements differ by country. Indonesia is far into its e-invoicing journey, while some countries have yet to even announce any official plans.

Doing business internationally is tough, especially when you add compliance to the mix. Working with Sovos means choosing a single vendor to handle tax compliance, wherever you operate.

Let us take care of your compliance burden so you can continue to focus on growing your business.

Israel is set to implement a continuous transaction controls (CTC) model that will require businesses to submit invoice data in electronic format for the tax authority to validate.

The mandate, set to come into force in May 2024, will require invoice data to be validated by the country’s tax authority before being sent to the final recipient. Read on for an overview of Israel e-invoicing requirements – we encourage you to bookmark the page to stay updated as the mandate develops.

At a glance: Characteristics of invoicing data submission in Israel

CTC Type CTC Clearance

Format JSON

Allocation Number Assigned by the ITA

E-invoicing Not mandatory

Electronic Signature Not applicable (though needed in case of e-invoicing)

Archiving Not applicable

Electronic invoicing laws in Israel

From 5 May 2024, Israel will make clearance CTC clearance mandatory. Authorised dealers (taxpayers) will have to clear invoices above a threshold of NIS 25,000 (before VAT), obtaining an allocation number acquired by the SHAAM – a computer system provided by the Israeli Tax Authority (ITA).

The invoice value threshold will be gradually reduced annually until 2028, ending at NIS 5,000 pre-VAT. Nevertheless, suppliers may report invoice data to the tax authority for clearance and request an allocation number for any amount.

Besides CTC clearance, e-invoicing rules remain in place and do not change with the new CTC requirements. Electronic invoices are still optional.

Since 2019, public entities in Poland have been mandated to receive and process e-invoices. While currently optional for suppliers of public entities, the transmission of e-invoices will be required for B2G and B2B transactions when the mandate is implemented (this was planned for 1 July 2024 until it was postponed in January 2024).

CTC clearance model

Israel’s model will include a clearance system from 5 May 2024. Businesses that exceed a specific threshold will be required to obtain an allocation number for invoices regarding B2B transactions. They can do so by issuing the invoice to the tax authority before sending it to the final customer.

Without receiving this number and including it on invoices, businesses will not be able to deduct input VAT.

Israel B2B e-invoicing

Israeli CTC clearance covers B2B transactions between authorised dealers.

However, e-invoicing is not mandatory under the new CTC clearance system. In case invoices are issued in electronic format (structured or unstructured format, including PDF), they must be cleared by the ITA and assigned with an allocation number before exchanged with the trading party.

Without receiving this number and including it on invoices, businesses will not be able to deduct input VAT.

Benefits of using e-invoicing in Israel

Although CTC Clearance mandate does not require e-invoicing, there are numerous benefits for businesses that electronically issue and receive invoices, including:

Cost savings through the reduction of paper, postage and manual labour

Saving time by using automated and structured processes

Streamlining operations through interoperable, uniformed initiatives and systems

Fewer issues and risks through the validation and authentication of data

Timeline of e-invoicing clearance in Israel

While combating fraudulent invoices has been discussed in Israel for a long time, the implementation of the upcoming CTC model is a relatively recent development.

February 2023: The 2023-2024 state budget and economic plan are approved, outlining a clearance CTC model

June 2023: The ITA announces plan for CTC implementation

July 2023: The ITA publishes technical specifications for the upcoming CTC model

October 2023: Clearance model is postponed from 1 January 2024

1 January 2024: The original date that the clearance e-invoicing model would be implemented

1 January 2024: The ITA platform becomes operational

5 May 2024: CTC clearance comes into effect

January 2025: Invoice threshold lowers to NIS 20,000 pre-VAT

January 2026: Invoice threshold lowers to NIS 15,000 pre-VAT

January 2027: Invoice threshold lowers to NIS 10,000 pre-VAT

January 2028: Invoice threshold lowers to NIS 5,000 pre-VAT

What is the future of e-invoicing in Israel?

While electronic invoice data will be required as part of the CTC initiative, Israel does not yet have a specific electronic invoicing mandate requiring dealers to issue invoices electronically.

Currently, Israel’s e-invoicing rules – which are classified as post-audit – include e-signing, content remarks and prior notification to the tax authority.

Israel has the potential to go the way of countries like Romania and Spain, mandating the use of e-invoices across transactions with governments and businesses. There is no official word on Israel’s future e-invoicing plans beyond the current CTC mandate.

What happens if I don’t comply?

If an allocation number is not requested for the invoice by the supplier, the buyer cannot deduct its VAT based on that invoice.

Setting up e-invoicing in Israel with Sovos

Sovos’ continuous transaction controls (CTC) software was purpose-built to help customers stay on top of their obligations wherever they do business, even as the rules change.

Currently, e-invoicing is permitted in Israel, provided it is prominently stated on the invoice that it is a ‘computerized document’ and prior notification is made to the ITA. A digital signature compliant with the local law is required to ensure the integrity and authenticity of the electronic invoice.

Storage of e-invoices must be within Israel – unless derogation has been granted. Both issuance and storage of e-invoices can be outsourced to third parties like Sovos.

Taxpayers opting to use e-invoices must comply with the abovementioned rules, as well as the CTC clearance requirements rolling out in 2024.

As CTCs and e-invoicing continue to grow in global adoption, it is vital to partner with a provider that closely monitors the decisions of tax administrations and understands the regulations you face. Sovos can help to stay compliant wherever you do business.

No, e-invoicing is not mandatory in Israel. Israel’s continuous transaction controls (CTC) mandate involves the electronic submission of invoice data and is set to come into effect on 5 May 2024.

Electronic invoice data must include specific information when submitted to the tax authority, including invoice ID, VAT number, invoice date, invoice amount and accounting software number. They also need to be given an allocation number by the ITA for the buyer to use this invoice for a tax deduction, as per the CTC clearance mandate.

Within the CTC mandate, the use of emergency allocation numbers is instituted as a contingency measure to address potential failures in its computer systems. In anticipation of such events, taxpayers must acquire and store these emergency numbers.

Israel’s mandated CTC clearance platform requires electronic invoice data to be submitted to and approved by the Israeli Tax Authority in real time. The authority will assign an allocation number and verify or reject the invoice data. Once validated, the allocation number will be returned to the seller so it can be issued to the buyer (in electronic or paper format).

It’s no surprise that inflation is on the forefront of everyone’s mind, with prices continuing to sky-rocket month by month. Data from the United Kingdom shows that the Consumer Prices Index (CPI) inflation jumped to a 40-year high of 9% in the past 12 months. Governments around the world are looking for ways to reduce the burden for consumers to keep global economies afloat. One method – implementing VAT rate cuts to certain goods and services – looks to be coming out on top as multiple countries around the world announced emergency budget sessions or introduced proposals to temporarily cut VAT rates.

Temporary VAT rate cuts are generally quick and easy to implement, which is why they are favored by governments globally. These cuts essentially allow for a boost to the economy by providing consumers with an overall higher amount to spend, incentivizing consumers to spend now while rates are lower.

Country proposals for VAT rate cuts

As expected, many countries have already announced VAT rate cuts or measures to stimulate their economies:

United Kingdom: Reports indicate that the Labour Party is pushing for an emergency budget session to demand VAT rate cuts for the hospitality industry. Previously, due to Covid-19, the UK implemented a temporary reduced rate of 13.5% on hospitality services which ended last month. Leaders suggest that the temporary rate reversal has cost the industry and should be re-implemented.

Slovenia: The Slovenian Parliament is currently reviewing a proposal to reduce energy and digital newspapers and journals from the standard VAT rate to 5%. This comes as inflation in Slovenia hits 6.9%.

Germany: German consumer groups are calling for VAT rate cuts on food, which had been previously ruled out due to restrictions in the EU VAT Directive.

Bulgaria: The Bulgarian government has proposed temporarily reducing VAT rates on domestic heating and bread for one-year, effective 1 July 2022.

Poland: Earlier this year Poland enacted VAT rate cuts for energy and certain basic food products. However, these rate cuts are only in place until 31 July 2022. The Polish government has indicated that these measures may be extended to continue to combat inflation.

Bahrain: A group of ten MPs are advocating for a suspension of the 10% VAT rate in Bahrain to help ease inflation rises, which was presented to the Bahrani government earlier this week.

Ireland: The Irish government has agreed to an extension for the reduced 9% VAT rate for the hospitality sector, now ending on 1 March 2023.

Additional countries such as Estonia, Netherlands, Latvia, Greece, and Turkey are also taking measures to implement VAT rate cuts to fight the ever-rising costs for consumers.

These VAT rate cuts coincide with new measures passed recently by the European Commission allowing Member States to apply reduced rates to more items, including food. Though many Member States seem to be moving towards taking advantage of this new flexibility on VAT rate reductions, it’s expected that as costs continue to rise more Member States and countries around the world will introduce VAT rate cuts to ensure consumer spending doesn’t continue to trend downward.

Take Action

To find out more about what we believe the future holds, download the 13th Annual Trends. Follow us on LinkedIn and Twitter to keep up-to-date with regulatory news and updates.