Rollout dates

From September 2026, France will implement mandatory e-invoicing via a central platform and connected service providers as well as a complementary e-reporting obligation.

With these comprehensive requirements, alongside the B2G e-invoicing obligation that is already mandatory, the government aims to increase efficiency, cut costs, and fight fraud.

This extended timeline is welcomed by many companies, providing more time to better understand and prepare for the far-reaching consequences of this reform for their business processes, IT systems and tax compliance strategy.

However, businesses should start preparing now. Here are the key dates:

From 1 September 2026

All companies headquartered or with established operations in France will have to accept e-invoices through the CTC system from their suppliers.

Issuing e-invoices according to the CTC regime will become mandatory for the largest enterprises (some 300 entities) and will apply also to a further 8,000 mid-sized companies – “Entreprises de taille intermédiaire”

The e-invoicing mandate does not apply to B2C and cross-border invoices though there is an obligation to report those transactions.

From 1 September 2027

All remaining medium and small companies will be in scope of the mandate.

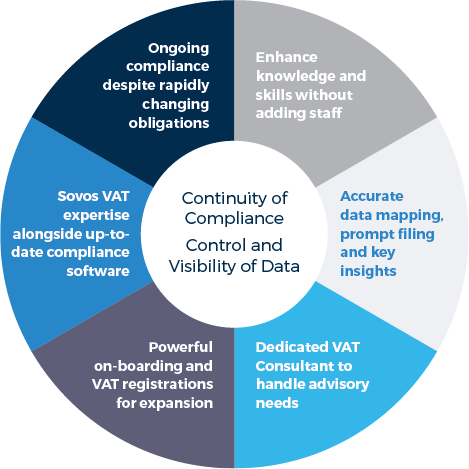

How can businesses prepare for the mandate?

The mandate presents challenges for businesses. There is a lot to consider, and most businesses current IT and manual processes aren’t equipped to handle this change.

The French e-invoicing mandate is still evolving and there are many elements remaining before the scheme is introduced.

In this e-book, we will cover in depth how business can achieve compliance:

- An overview of the French mandate

- The latest update to the timeline

- Partner Dematerialization Platform (PDP) registration requirements

- What’s on the horizon for the French Mandate

- Challenges for your organisation – what buyers and suppliers need to consider to prepare their business processes

- How Sovos can help businesses prepare for France’s e-invoicing mandate

Many businesses will need help to achieve compliance with the new mandate.

Sovos has unmatched experience with continuous transaction controls and e-invoicing mandates all over the world. Our scalable global platform has evolved to encompass new mandates, handling the needs of today, and the future.

Download e-book

A Quick Guide to E-invoicing and Real-Time Reporting

Tax regulations in Eastern European countries are complex but that shouldn’t be a reason not to do business there. If you’re responsible for VAT compliance, this ebook provides key details of the varying VAT digitisation mandates and business requirements across the region:

A Quick Guide to E-invoicing and Real-Time Reporting

Tax regulations in Eastern European countries are complex but that shouldn’t be a reason not to do business there. If you’re responsible for VAT compliance, this ebook provides key details of the varying VAT digitisation mandates and business requirements across the region: