Compliance Mandates Around the World Have Elevated the Importance of Tax

Sorting out indirect tax issues was not traditionally at the top of any IT organisation’s to-do list. Today that’s changed and new VAT compliance mandates being introduced at an increasing rate around the world have elevated its status.

It’s more important than ever that IT decision makers and in-house tax and finance professionals engage and have meaningful, strategic discussions about how – and also why – to accelerate their digital transformation. This will enable them to not only respond but also to prepare for invasive new tax mandates.

Each time a product or service is sold in a new country or under the watchful eye of evolving national tax regimes, enterprises must respond. They must ensure their VAT recognition and reporting processes are aligned to new and evolving mandates for continuous controls on e-invoicing and other critical sales and purchase processes and documents.

Get the e-book

A cascade of tax compliance mandates

Multinational companies continue to leverage new technologies to optimise borderless supply chains. The spectacular growth of e-commerce and a new generation of technologies is opening global markets for even the smallest of micro-enterprises.

Global businesses and supply chains increasingly intersect new national mandates. Many of these mandates impose sophisticated real-time controls on business transactions and make compliance more complex than it’s ever been before. And the cost of non-compliance can be high.

Non-compliance can affect an organisation in many ways – financial, operational, employee productivity, customer experience, legal, and even brand perception.

IT, tax and finance teams need to communicate and collaborate effectively to fully understand their compliance obligations in each of the markets where they operate. If they can’t companies will likely find their digital transformations inhibited by disparate local point solutions that can be so entrenched, they can become impossible to replace.

With better collaboration between functions and alignment on tax, your entire organisation can achieve real operational efficiencies.

Download our e-book and read about

The opportunities that exist when tax and IT work together

How joined up thinking can reduce risk and uncover opportunities

A shared vision and modern tax solution

How better conversations drive a better compliance process

As tax compliances becomes increasingly interconnected with core business processes, organisations must make all aspects of tax reporting central to, and integrated with, core business activities.

A modern tax compliance solution must be engineered from the ground up to handle modern regulatory mandates. This especially applies to global manufacturers and retailers that do business in numerous countries around the world and must comply with mandates established by hundreds of tax authorities.

Read more and download the e-book

In 2020, the European Commission (EC) adopted a four-year plan to develop a fairer and simpler taxation framework. The Action Plan aspires to tighten up the tax system, ensure that digital platforms are made to follow transparency rules and utilise data better, reducing tax fraud and evasion.

In 2021, the Commission implemented e-commerce changes – another step in the modernisation process. Beginning in July of 2021, the Mini One Stop Shop (MOSS) system was expanded to the One Stop Shop (OSS) and Import One Stop Shop (IOSS).

The implementation of OSS expanded the use of the union and non-union schemes. This allows European and non-European business-to-consumer sellers of digital services and goods to simplify their reporting practices. Meanwhile, IOSS allows businesses to register and import goods into the EU with a value not exceeding €150.

In 2022, there are plans to release legislation under the “VAT in the digital age” Action Plan. Much like its predecessors in 2020 and 2021, the core purpose of this plan is to tackle the issue of fraud and improve the way businesses engage with the VAT system. The Commission has announced three points it seeks to address in its legislation:

Specifically, one point of interest is the single EU VAT registration point, which aims to facilitate compliance among Member States. With this, the European Commission is requesting feedback on how businesses think the I/OSS implementation has gone and on other potential legislative options for the future, including:

Extension of OSS to:

Cover all B2C supplies of goods and services by non-established suppliers

Enable intra-Community supplies and acquisitions of goods, thereby avoiding VAT registration when transferring own goods cross-border

Include B2B supplies of goods and services while leaving in place the current VAT refund mechanism

Include B2B supplies of goods and services while also introducing a deduction mechanism for OSS

Reverse charge made available for all B2B supplies carried out by non-established suppliers

Removing the €150 threshold for IOSS so that it applies to distance sales of goods of any value

Making IOSS mandatory for:

All distance sales of imported goods

All distance sales of imported goods above an EU turnover threshold (e.g. €10,000)

Marketplaces only

The European Commission began a period of public consultation on 21 January regarding adapting VAT rules in a digital economic landscape. They are seeking feedback on how the EC should adapt VAT tax processes and how they can incorporate technology to solve principal issues in tax, such as fraud and the complexity of its systems. The Commission is accepting feedback in this public consultation period until 15 April 2022 – submissions can be made here.

Sovos will continue to monitor the development of this legislation throughout the year as more information about its structure and impact is released, as these changes are sure to be impactful upon the European VAT landscape.

Insurance is a dynamic sector in constant flux to accommodate with insured’s needs. An increase in holidays abroad following WWII saw the need for Assistance insurance for any unforeseen events that occurred away from the insured’s home country. Council Directive 84/641/EEC regulated Assistance insurance for the first time, and a new class of insurance was created. This was in addition to the 17 previously regulated classes outlined in Directive 73/239/EEC of non-life insurance and was called Assistance (Class insurance 18).

Travel insurance evolution

Initially, the insured was covered by a policy that provided aid for any event travelling abroad (loss of passport, assistance with any problem in the car etc). The insurer created a range of support with call centres, supplier networks and additional services to help solve difficulties when travelling abroad.

Subsequently, following the insured’s requirements, insurance companies and travel agents created travel insurance that includes a wide range of services. These consist of several protections within different classes of business. This is where the tax complexity of travel insurance policies begins. It’s an amalgamation of coverages, and the application of the correct fiscal treatment needs to be analysed in each territory.

Correct tax treatment in travel insurance

When weighing the correct application of tax for travel insurance, businesses must consider the following: location of risk (LoR), class of businesses and the correct tax approach.

Business travel: The LoR of the employer’s policy to cover their employees will be located where the business is located.

Individuals: The LoR will be the territory in which the policyholder is habitually resident unless the policy covers travel or holiday risks for four months or less. In this case, the LoR is the Member State where the policyholder took out the policy.

Class of business affected: As mentioned previously, one of the complexities of travel insurance is determining the classes of business affected. It’s common to see, in these policy types, multiple coverages such as medical assistance cover, loss or damage to baggage, travel delays or cancellations, loss of documents or money, personal accident, repatriation etc. Insurers must adequately identify these coverage details to ensure the compliant tax treatment is used.

Taxability: This step is crucial. The correct treatment of the policies could vary the liabilities to be paid, the different taxes and/or levies and parafiscal charges to be included in the tax calculation. This means that the tax treatment can change by country. It’s necessary to identify the tax liability or exemption based on the class of business and the geographical location.

Insurers must understand the importance of the vital details associated with travel insurance. Determining LoR, class of business affected and taxability ensures the correct amount is paid and submitted to the proper jurisdictions.

Many multinational companies find VAT compliance challenging, especially when trading cross-border.

With the increase in real-time reporting across Europe and differing VAT registration and reporting requirements, VAT compliance now requires significant resources and specialist knowledge to ensure compliance and avoid costly penalties.

As your business expands, so do your VAT obligations. This is why many organisations, turn to managed service providers to ease the burden of VAT compliance, audits and fiscal representation.

This e-book discusses the many elements of VAT compliance including:

VAT registration

Fiscal representation

How to determine VAT obligations

Filing VAT returns

Preparing for an audit

Managing VAT changes

VAT compliance advice from JD Sports’ Indirect Tax Manager

How JD Sports manage VAT compliance with Sovos’ Managed Services

John Dowd, Indirect Tax Manager at sport-fashion retailer JD Sports discusses how he managed cross-border VAT compliance with the help of Sovos’ managed services

“For us at JD Sports and me personally I’m looking for a partnership, something long term, as it takes time and costs money to change advisors. I’m looking for a long-term relationship over a number of years with a VAT service provider.

“I want my advisor to have specialist knowledge, for us that’s retail and cross-border supply chains, overseas tax authorities, and I want to see new talent joining the team. I prefer a single point of contact to make it easier to move things along and of course, competitive pricing, and Sovos ticked all of these boxes for us.”

John Dowd, Indirect Tax Manager at JD Sports

The many elements of VAT compliance

VAT compliance has many elements, beginning with an understanding of place of supply rules to determine where VAT registration is required. Fiscal representation might be required to register in EU Member States.

Once VAT registration is underway, the next step is to determine EU VAT obligations by mapping the supply chain for the country of registration. There are also additional requirements to consider including exemptions, recovering VAT, Intrastat and varying continuous transaction controls (CTCs) mandates.

Submitting VAT returns to ensure compliance is a never-ending process. Each country has its own VAT return regulations and additional declaration requirements.

The VAT compliance cycle also includes preparation for VAT audits. Tax authorities can carry out audits for a variety of reasons so it’s important businesses prepare for audits and ensure they are able to manage the process successfully.

How Sovos VAT Managed Services can help with VAT compliance

Sovos’ end-to-end, technology-enabled VAT Managed Services can ease your compliance workload and mitigate risk where-ever you operate today, while ensuring you’re ready to handle the VAT requirements in the markets you intend to dominate tomorrow.

Whilst the UK leaving the European Union (EU) on 31 December 2020 seems like a long time ago, UK businesses still have to deal with changes to the processes in place when importing goods from suppliers in the EU.

Customs Declarations

Throughout 2021, goods imported into Great Britain from the EU were subject to several easements from a customs perspective. This was to reduce the burden of completing full customs declarations and dealing with all of the consequences of importing goods that were previously not subject to import documentation and controls.

UK businesses were unprepared, partly due to impacts from the COVID-19 pandemic, so these simplifications were extended a few times during 2021. As of 1 January 2022, goods moving between the EU and Great Britain will be subject to full customs declarations and controls. Subsequently, there is no longer the ability to defer customs declarations as was previously the case.

Additionally, any customs duty due on goods will be due at the time of entry rather than when the customs declaration is submitted, as was the case in 2021. Businesses can achieve delayed payment of the customs duty by applying for a duty deferment account with HMRC. In some instances, it can be achieved without the need for a financial guarantee to be lodged, so it is worth considering.

Due to the negotiations between the UK government and the EU on the Northern Ireland Protocol, imports of non-controlled goods from Ireland and Northern Ireland will not be subject to these changes. The previous easements will still apply. This means that customs declarations can be delayed for up to 175 days. The UK government will make further announcements once the discussions on the Protocol have been completed. We will update further when that happens.

Import VAT

Regarding import VAT, Postponed Import VAT Accounting (PIVA) remains available and, whilst not compulsory, it is recommended, as it provides a valuable cashflow benefit. It applies to imports from all countries and not just the EU. Unlike in some EU countries, it is not automatically applied and has to be claimed when the import declaration is submitted. Therefore, the importer must advise whoever submits the declaration to complete it accordingly. If it is not claimed, import VAT is payable at the time of entry and will have to be recovered on the VAT return – HMRC continues to issue the C79 certificate when VAT is paid at the border, and it is required evidence to recover VAT.

Businesses will also need to remember to download the monthly PIVA statement from HMRC’s website – this is required to determine the amount of import VAT payable on the VAT return. This needs to be done within six months as it is not available after that time.

Intrastat declarations

Another change is regarding Intrastat reporting for imports into Great Britain from the EU. Arrivals declarations were required during 2021 to provide the UK government with trade statistics, given that importers could delay submitting full customs declarations. Intrastat arrivals are now only required for goods moving from the EU to Northern Ireland – this is because Northern Ireland is still considered part of the EU for goods.

The EU-UK Trade and Cooperation Agreement provisions have to be considered when importing goods from the EU especially regarding the origin of the goods and whether the import is tariff-free. This has been in place since 1 January 2021, but there are practical changes that are considered further in our article which discusses the origin of goods and claiming relief on trade between the EU and UK. These changes mean that imports from the EU are treated in the same way as imports from any other country, except for goods from Ireland and Northern Ireland, which are still subject to special arrangements.

Take Action

Keen to know how changes between the EU and UK will impact your VAT compliance obligations? Contact us to find out more.

The EU-UK Trade and Cooperation Agreement (TCA) provides for tariff-free trade between the United Kingdom (UK) and the European Union (EU) but does not work in the same way as when the UK was part of the EU.

Before Brexit, if the goods were in free circulation within the EU, they could be moved cross-border without incurring any additional customs duty. Therefore, the origin of the goods was not relevant for this intra-EU movement. If the goods originated from outside the EU, customs duty would have been paid as required when they first entered into free circulation but was not payable again.

This difference creates issues for UK businesses where they import finished goods into the UK first before being sold to the EU. As the goods are not being processed in the UK, they cannot be of UK origin and will be subject to double duty unless specific duty mitigations measures are taken.

The same tariff-free trade between the EU and the UK can be achieved under the TCA, but it depends on meeting the detailed rules within the agreement. The key is in the origin of the goods and whether they qualify under the terms of the TCA. This ensures that only eligible goods are tariff-free and removes the risk of goods entering from outside the Free Trade Area without paying customs duty.

The requirement for goods to be of relevant origin to benefit from zero tariffs on imports under the TCA has been in place since 1 January 2021.

Claiming and evidencing relief

If goods meet the appropriate rules of origin, preference can be claimed on the customs declaration when they are imported. Thus, the claim is made by the importer of the goods. However, it is not as simple as completing the appropriate box on the declaration; there is a requirement for the proper evidence to be held.

To claim tariff preference, the importer needs to have one of the following proofs of origin:

A statement on origin – this must be made out by the exporter to confirm the product originates in the UK or EU; or

Importer’s knowledge – this option allows the importer to claim tariff preference based on their knowledge of where the goods they’re importing originate.

If they are relying on a statement of origin, the exporter will have to prove that the goods are of appropriate origin to qualify.

End of easement

In 2021, there was a light touch approach towards holding evidence when the customs declaration was made. The TCA allowed for a declaration to be made and the evidence to be obtained later to reduce the burden on business. There is still a requirement to provide the appropriate evidence on request, so businesses must ensure that it will be available if necessary.

There may be checks that the goods are of appropriate origin to be free of duty under the TCA. With effect from 1 January 2022, there is a need to have the appropriate evidence that the goods meet the origin requirements when the declaration is lodged. Therefore, businesses will need to ensure that the appropriate documents are immediately available should they be requested.

Post import claims for relief

Businesses should note that it is not obligatory to claim preference at the time of entry of the goods as claims can be made up to three years later, as long as there is valid proof of origin. It is beneficial to claim preference at the earliest possible time to benefit cash flow and provide certainty of the cost of the goods.

Therefore, businesses will need to ensure that they determine origin of goods correctly and have the appropriate evidence to support the goods being tariff-free.

It’s important to remember that the rules for trade between Northern Ireland and the EU are different because of the Northern Ireland Protocol.

Take Action

Get in touch with Sovos to discuss your company’s obligations for cross-border trade.

Meet the Expert is our series of blogs where we share more about the team behind our innovative software and managed services.As a global organisation with indirect tax experts across all regions, our dedicated team is often the first to know about new regulatory changes and the latest developments on tax regimes worldwide to support you in your tax compliance.

We spoke to Khaled Cherif, senior client representative here at Sovos to discover more about Insurance Premium Tax (IPT) and, in particular, the complexities of France and the French overseas territories.

Can you tell me about your role and what it involves?

I joined Sovos as part of the IPT team in June 2017. My role is senior client representative and I mostly work with our French and Italian clients, which is around 54 organisations.

I am the first point of contact so my role along with the rest of the team is to provide clients with all the assistance that they require, including helping them with filing their liabilities and ensuring they are compliant with the relevant regulations.

Can you explain IPT in France and what is particularly complex about the country’s IPT regulation and requirements?

IPT in France is quite complex as there are many parafiscal charges that can apply to insurance premiums. There are also multiple IPT rates depending on the type of risk being covered. This can range from 7% IPT rate to as high as 30%. As well as the different IPT rates there are also 10 parafiscal charges that could be due on insurance premiums and again all with varying rates.

There are also French overseas territories to be considered. There are two groups of French overseas territories, the Départements and Régions d’Outre-Mer (DROMs), and Collectivités d’Outre-Mer (COMs).

What top tips do you have for insurers that have IPT obligations in France and other EU countries?

It’s important to understand the differences in IPT requirements with the French overseas territories.

DROMs (French Guyana, Guadeloupe, Martinique, Mayotte, and Reunion) are treated the same as mainland France for premium tax purposes. Premiums covering risks located in these territories should be declared in the same way, except for Guyana and Mayotte where the IPT rates applicable are reduced by half.

For COMs the local tax authority for the territory can levy taxes on insurance premiums. Most have set up their own IPT regimes, often requiring insurers to appoint a fiscal representative. In some COMs territories the tax ID issued for Mainland France can be used.

As many French and international organisations have subsidiaries in overseas French territories it’s important to understand how the different IPT rates and filings affect compliance. Not being based in the territory where IPT needs to be filed can make things complicated, so working with local partners or representatives can ease the burden.

How can Sovos help insurers?

Sovos has a team with global IPT expertise, meaning we can help organisations understand their IPT requirements wherever they operate, including in France and the French Overseas Territories.

Sovos has in-depth knowledge of local requirements, laws and regulations as well as local partners and representatives to assist with IPT requirements.

During the last decade, the Vietnamese government has been developing a feasible solution to reduce VAT fraud in the country by adopting an e-invoice requirement for companies carrying out economic activities in Vietnam. Finally, on 1 July 2022, a mandatory e-invoicing requirement is scheduled to enter into force nationwide.

2020 e-invoicing mandate postponement

Despite the postponement of the original starting date for the mandatory nationwide e-invoicing obligation, which was first intended to enter into force in July 2020, the Vietnamese government quickly established a new deadline.

Later that year, in October 2020, the new timeline was communicated through Decree 123, delaying the e-invoicing mandate until 1 July 2022. This new deadline is also in line with the implementation dates for the rules concerning the e-invoicing system envisaged in the Law on Tax Administration.

Ongoing regional readiness plan

Vietnam’s General Taxation Department (GTD) announced its plan to work first with the local tax administrations of six provinces and cities: Ho Chi Minh City Hanoi, Binh Dinh, Quang Ninh, Hai Phong and Phu Tho to start implementing technical solutions for the new e-invoice requirements and the construction of an information technology system that allows the connection, data transmission, reception, and storage of data. According to the GTD’s action plan, by March 2022, these six cities and provinces should be ready for the e-invoice system’s activation.

The GTD announced that, from April 2022, the new e-invoicing system will continue to be deployed in the remaining provinces and cities.

Finally, under this local implementation plan, by July 2022, all cities and provinces in Vietnam must deploy the e-invoicing system based on the rules established in Decree 123 and the Circular that provides guidance and clarification to certain aspects of the new e-invoicing system.

Next steps for businesses

Taxable persons operating in Vietnam will be required to issue e-invoices for their transactions from 1 July 2022 and must be ready to comply with the new legal framework. Enterprises, economic organisations, other organisations, business households and individuals must register with the local tax administration to start using e-invoices according to the rules established in the mentioned Decree 123.

Vietnam is finally moving forward to adopt mandatory e-invoicing. However, there is plenty of work related to the necessary technical documentation and local implementation of the new e-invoicing system. We will continue to monitor the latest developments to determine whether the GTD can meet all the requirements in time for the mandatory e-invoicing roll-out.

Take Action

Need help staying up to date with the latest VAT and compliance updates that may impact your business? Get in touch with our team of experts today.

We recently launched the 13th Edition of our annual Trends report, the industry’s most comprehensive study of global VAT mandates and compliance controls. Trends provides a comprehensive look at the world’s regulatory landscape highlighting how governments across the world are enacting complex new policies and controls to close tax gaps and collect the revenue owed. These policies and protocols impact all companies in the countries where they trade no matter where they are headquartered.

This year’s report looks at how large-scale investments in digitization technology in recent years have enabled tax authorities in much of the world to enforce real-time data analysis and always-on enforcement. Driven by new technology and capabilities, governments are now into every aspect of business operations and are ever-present in company data.

Businesses are increasingly having to send what amounts to all their live sales and supply chain data as well as all the content from their accounting systems to tax administrations. This access to finance ledgers creates unprecedented opportunities for tax administrations to triangulate a company’s transaction source data with their accounting treatment and the actual movement of goods and money flows.

The European VAT landscape

After years of Latin America leading with innovation in these legislative areas, Europe is starting to accelerate the digitization of tax reporting. Our Trends report highlights the key developments and regulations that will continue to make an impact in 2022, including:

VAT reporting processes become digital and more frequent – Existing VAT reporting is becoming more granular and more frequent in many EU Member States, with the majority quickly evolving towards real-time controls with or without electronic invoice mandates.

Italy has mandatory e-invoicing via a data exchange platform previously introduced for public procurement messaging.

Since 2017 in Spain, all companies must report inbound and outbound invoices within four days.

In Hungary, suppliers have had to report their sales invoices in real-time since 2018.

Public procurement standards will play a major role in the design of various continuous transaction control (CTC) models – Frameworks such as PEPPOL are increasingly adopted by public administrations as large buyers of goods and services – the standards and platforms used for these transactions will increasingly be repurposed for electronic invoicing as a key enabler of VAT digitization.

“Own the Transaction” CTC model becomes more popular – More tax administrations aim not only to receive reporting data from business transactions but use legislation to become the invoice exchange platform themselves.

This trend is gaining traction after Turkey and Italy introduced it as core concepts in their CTC legislation, while countries like France and Poland are introducing similar models.

SAF-T is here to stay – The OECD’s Standard Audit File for Tax (SAF-T) will remain an inspiration for European tax administrations not only to enforce VAT via real-time or near-real-time controls, but to obtain copies of taxpayers’ entire accounting books on their own systems for broader tax controls and audit support as well.

EU E-commerce VAT package and digital services – Changes introduced in July 2021 to the One Stop Shop (OSS) and the launch of an Import One Stop Shop (IOSS) concept have drastically changed requirements for all e-commerce vendors and marketplaces selling low-value goods or digital services to European consumers.

According to Christiaan van der Valk, lead author of Trends, governments already have all the evidence and capabilities they need to drive aggressive programs toward real-time oversight and enforcement. These programs exist in most of South and Central America and are rapidly spreading across countries in Europe such as France, Germany and Belgium as well as Asia and parts of Africa. Governments are moving quickly to enforce these standards and failure to comply can lead to business disruptions and even stoppages.

This new level of imposed transparency is forcing businesses to adapt how they track and implement e-invoicing and data mandate changes all over the world. To remain compliant, companies need a continuous and systematic approach to requirement monitoring.

Trends is the most comprehensive report of its kind. It provides an objective view of the VAT landscape with unbiased analysis from our team of tax and regulatory experts. The pace of change for tax and regulation continues to accelerate and this report will help you prepare.

Take Action

Contact us or download Trends to keep up with the changing regulatory landscape for VAT.

Identifying the Location of Risk in the case of health insurance can be a tricky subject, but it’s also crucial to get it right. A failure to do so could lead to under-declared tax liabilities in a particular territory and the potential for penalties to be applied once these deficits are identified and belatedly settled. We examine the situation from a European perspective.

Legal background

The starting point in this area is the Solvency II Directive (Directive 138/2009/EC). Notably, Article 13(13) outlines the different categories of insurance risks that are used to determine risk locations. As health insurance doesn’t fall within the specific provisions for property, vehicles and travel risks, it is dealt with by the catch-all provision in Article 13(13)(d).

This Article refers to the ‘habitual residence of the policyholder’ or, where the policyholder is a legal person, ‘that policyholder’s establishment to which the contract relates’. We will consider these scenarios separately, given the distinction between individuals and legal persons.

Where the policyholder is an individual

For natural persons, the situation is generally straightforward. Based on the above, the key factor is the habitual residence of the policyholder. The permanent home of the policyholder tends to be relatively easy to confirm.

More challenging cases can arise where someone moves from one risk location to another. For example, when an individual purchases insurance in a particular country, having lived there for a significant period before moving to another country soon afterwards, the Location of Risk will be the original country. As EU legislation does not go into detail on the point, examples of no apparent habitual residence will be dealt with on a case-by-case basis.

Where the policyholder is a legal person

In this scenario, we have to consider the ‘policyholder’s establishment to which the contract relates’ in the first instance. The establishment is treated quite broadly, as evidenced by the European Court of Justice case of Kvaerner plc v Staatssecretaris van Financiën (C-191/99), which pre-dates Solvency II.

Notwithstanding the above, the habitual residence of the insured should be used to identify the risk location even where the policyholder is a legal person in certain circumstances. This will occur when the insured is independently a party to an insurance contract, giving them a right to make a claim themselves rather than through the corporate policyholder.

This logic can also potentially be extended to dependents of the insured person added to the policy and who can also separately claim under the contract. They will also create a risk location, although this will often be in the same country as the insured person. Ultimately, the compliant approach will be dictated by the overall set-up of the policy.

If any insurers writing business in Europe have any questions on the location of risk rules, whether concerning health insurance or any other insurance, then Sovos is best placed to provide advice to ensure taxes are being correctly declared.

On 30 January 2022, the Zakat, Tax and Customs Authority (ZATCA) published an announcement on its official web page concerning penalties for violations of VAT rules, and it is currently only available in Arabic. As part of the announcement, the previous fines have been amended, ushering in a more cooperative and educational approach for penalizing taxpayers for their non-compliance with VAT rules than previously.

What’s the new approach?

If ZATCA officials detect a violation during a field visit, the taxpayer will first be given a warning about the violation without any penalty. The ZATCA aims to raise awareness instead of penalizing taxpayers for their first violation. Taxpayers will be granted three months to comply and make necessary changes in their processes.

If non-compliance continues after the first inspection, the taxpayer will be fined 1.000 Riyals, roughly 267 USD. The penalty charge will gradually increase if the taxpayer fails to comply with the rules and doesn’t make necessary changes within three months after the notice.

The fine for each additional repetition time will be as follows: 5.000 Riyals for the third time, 10.000 Riyals for the fourth time and 40.000 Riyals for the fifth time. If the same violation is repeated 12 months after its discovery, it is considered a new violation, and the process will begin with a warning without a fine.

What are the violations of e-invoicing?

According to the announcement, the violations of e-invoicing rules will be penalized per the new procedure described above. The instances that require a notice/fine are slightly different than the initial violations described previously and highlighted as follows:

Not issuing and storing invoices electronically

Not including a QR code

Non-compliance with keeping electronic invoices and electronic notes in the form stipulated

Not notifying the authority of any malfunction that hinders the issuance of electronic invoices

Deleting or modifying electronic invoices after their issuance

Including any of the prohibited functions in the e-invoicing solutions

Violation of any other provision of electronic invoicing.

What´s next?

The ZATCA states that the new approach ensures proportionality between the violation and the penalty imposed on taxpayers while giving taxpayers a chance to comply within a specific time frame. Considering that the introduction of both VAT and mandatory e-invoicing is fairly recent in the country, there are certain aspects that are unclear for taxpayers. This approach will educate businesses and is expected to be welcomed by stakeholders.

Towards the end of 2021, the tax authority in Turkey published a draft communique that expands the scope of e-documents in Turkey. After minor revisions, the draft communique was enacted and published in the Official Gazette on 22 January 2022.

Let’s take a closer look at the changes in the scope of Turkish e-documents.

Scope of e-fatura expanded

The gross sales revenue threshold will decreased reduce. The threshold limit has been lowered from TRY 5 million to TRY 4 million and above for the 2021 financial period. A lower threshold of TRY 3 million and above will apply for 2022 and subsequent fiscal periods.

The use of the e-fatura is now mandatory for taxpayers in the e-commerce sector when exceeding a certain threshold. The communique introduced a gross sales revenue threshold of TRY 1 million and above for 2020 and 2021 financial periods; and TRY 500.000 for 2022 and all subsequent fiscal periods.

Taxpayers who run a business in the real estate and/or motor vehicle sector by carrying out construction, manufacturing, purchase, sale, and rental transactions, as well as taxpayers who act as intermediaries in these transactions must use the e-fatura application if their gross sales revenue exceeds TRY 1 million and above for 2020 and 2021 financial periods; and TRY 500.000 for 2022 and all subsequent fiscal periods.

Taxpayers who provide accommodation services by obtaining investment and/or operation certificates from the Ministry of Culture and Tourism and Municipalities must use the e-fatura application.

Taxpayers meeting these thresholds and criteria must start using the e-fatura application from the start of the year’s seventh month following the relevant accounting period.

In terms of accommodation service providers, if they provide services as of the publication date of this communique, they must start using the e-fatura application from 1 July 2022.

For any business activities that start after the publication date of the communique e-fatura must be used from the beginning of the fourth month following the month in which their business activities began.

E-arsiv invoice scope expanded

Taxpayers not in scope of e-arşiv invoices have been obliged to issue e-arşiv invoices if the total amount of the invoices to be issued exceeds TRY 30.000 including taxes (in terms of invoices issued to non-registered taxpayers, the total amount including taxes exceeds TRY 5.000) from 1 January 2020.

With the amended communique, the Turkish Revenue Administration (TRA) lowered the total amount of the invoice threshold to TRY 5.000, and thus more taxpayers will be required to use the e-arsiv application. The new e-arsiv invoice threshold applies from 1 March 2022.

E-delivery note scope expanded

Another change introduced by the communique was the expansion of the scope of e-delivery notes. The gross sales turnover threshold for mandatory e-delivery notes has been revised to TRY 10 million, effective from the 2021 accounting period. In addition, taxpayers who manufacture, import or export iron and steel (GTIP 72) and iron or steel goods (GTIP 73) are required to use the e-delivery note application. E-fatura application registration is not applicable to those taxpayers.

The EU E-Commerce VAT Package came into effect on 1 July 2021. And with it, the need for operational change, business disruption and plenty of accounting complexity.

A key component of the package is the Import One Stop Shop (IOSS) – a new way for companies to meet their EU VAT obligations when trading cross-border.

In this e-book we explain IOSS’s key concepts and common use cases so you can better understand and take advantage of IOSS and how you apply it to your business.

IOSS is expansive, complicated and rewrites the rules for companies selling into and within Europe. This e-book aims to simplify that for you. We cover:

The basics

Intermediary requirements

Key considerations for your business

How to ensure IOSS compliance

How we can help

Get the e-book

We spend ample time on each of these topics so that you feel confident understanding whether IOSS is the right option for your business.

Our e-book starts with an easy-to-understand primer on IOSS. This includes how IOSS operates, its many rules and what has happened. The e-book also explains more on IOSS intermediaries as well as their purpose and when they can be used.

Find out more about the IOSS registration process, including its effects on:

Customer experience

VAT registration

VAT simplification

Record keeping

Data collection and invoicing

Contingency planning

Commercial matters

We answer some important questions you should consider about IOSS registration:

Will you need to appoint an intermediary?

How will you appoint one?

How will you get set up for IOSS registration – will you do this yourself or search for help?

How will you submit monthly returns and pay the VAT or use a partner?

How can you ensure record keeping data is in the right format and up to date?

How will you respond to tax authority audits?

Whatever your eventual IOSS decision is, our e-book will help you make an informed decision for the good of your business.

Whatever your VAT implications, Sovos has the expertise to help you navigate your global events and the complexities of cross-border VAT obligations.

Our VAT Managed Services ease your compliance workload while mitigating risk wherever you operate today. In addition, we ensure you’re ready to handle the VAT requirements in the markets you intend to lead tomorrow.

The Tax Bureaus of Shanghai, Guangdong Province and Inner Mongolia Autonomous Region have all issued announcements stating they intend to carry out a new pilot program for selected taxpayers based in some areas of the provinces. The pilot program will involve adopting a new e-invoice type, known as a fully digitized e-invoice.

Introduction of a new e-invoice type

Many regions in China are currently part of a pilot program that enables newly registered taxpayers operating in China to voluntarily issue VAT special electronic invoices to claim input VAT, mostly for B2B purposes.

The new fully digitized e-invoice is a simplified and upgraded version of current electronic invoices in China. The issuance and characteristics of the fully digitized invoice are different from other e-invoices previously used in the country.

Characteristics of the fully digitized e-invoice

The fully digitized invoice is supervised by the local Taxation Bureaus as part of the pilot program

The legal effect and basic purpose are the same as those of existing paper invoices

Fully digitized invoices can be delivered in the form of data messages, which eliminates specific format requirements such as PDF or OFD

The basic content includes dynamic QR code, invoice number, invoice date, buyer information, seller information, quantity, unit price, amount, tax rate, tax amount, total, total price, and tax

After the pilot program taxpayer has passed a “real-name verification” they can immediately use the electronic invoice service platform to issue invoices without the need to use special equipment for tax control (e.g., UKey device)

Pilot taxpayers can automatically deliver fully digitized invoices through the tax digital account of the electronic invoice service platform and can also deliver fully electronic invoices themselves via email or other means

Verification of fully digitized e-invoices

Relying on the national unified electronic invoice service platform, tax authorities will provide selected taxpayers for this pilot program with services such as issuance, delivery, and inspection of fully digitized e-invoices 24 hours a day. Taxpayers will be able to verify the information of all electronic invoices through the electronic invoice service platform or the national VAT invoice inspection platform.

What’s next for e-invoicing in China?

This new pilot program has been effective in Shanghai, Guangzhou, Foshan, Guangdong-Macao Intensive Cooperation Zone, and Hohhot since 1 December 2021. Despite the lack of an official timeline for implementation, it’s expected that the scope of this pilot program will be extended in 2022 to cover new taxpayers and regions in China, paving the way for nationwide adoption of the fully digitized e-invoice.

Many tax authorities are increasing their focus on the insurance industry in an effort to close tax revenue gaps, with many introducing Insurance Premium Tax (IPT) and other indirect taxes for insurance. Globally, IPT is fragmented across over 200+ countries and achieving compliance can be a complex process requiring specialist knowledge.

Insurers, especially those operating across multiple territories, can find keeping up to date with the latest IPT rates, rules and regulations to ensure compliance challenging.

This guide provides a helpful snapshot of the indirect tax rules that apply to insurance premiums across Europe.

The guide provides a useful reference of indirect rules across Europe including:

Albania, Andorra, Austria, Belarus, Belgium, Bosnia and Herzegovina, Bulgaria, Croatia, Cyprus, Czech Republic, Denmark, Estonia, Finland, France, Georgia, Germany, Gibraltar, Greece, Guernsey, Hungary, Iceland, Ireland, Isle of Man, Italy, Jersey, Kosovo, Latvia, Liechtenstein, Lithuania, Luxembourg, Malta, Moldova, Monaca, Montenegro, Netherlands, Norway, Poland, Portugal, Romania, San Marino, Slovakia, Slovenia, Spain, Switzerland, United Kingdom.

Insurance Premium Tax compliance

The digitization of tax is a trend that will undoubtedly continue. Organisations need to prepare for any changes to reporting as this will impact compliance obligations for the countries they operate in.

Tax authorities have increased their focus on the insurance industry to ensure IPT and parafiscal taxes are collected correctly, accurately, and on time.

Operating in multiple countries inevitably means also having to comply with many local regulations in line with IPT statutory and parafiscal filing. Compliance regimes can be simple or complex, but the difficulty is that they’re varied.

As a result of the 2020 Finance Law implementation, which transfers the management and collection of import VAT from customs to the Public Finances Directorate General (DGFIP), France has implemented mandatory reporting of import VAT in the VAT return instead of having the option to pay through customs as is typically the process. This change came into effect on 1 January 2022, with additional VAT reporting changes in France, including the Declaration of Exchange Goods (DEB) split where the Intrastat dispatch and EC sales list are now separate reports.

This new import procedure is mandatory for all taxpayers identified for VAT purposes in France. Registered taxpayers may no longer opt to pay import VAT to customs and must report all import VAT via the VAT return. This is a departure from the prior process, where taxpayers needed to receive prior authorisation to implement a reverse charge mechanism to pay import VAT through the VAT return. Now, this process is automatic and mandatory, and no authorisation is required.

Consequently, taxpayers with import transactions into France must now register for VAT purposes with the French tax authorities. Additionally, the French intra-community VAT number of the person liable for payment of import VAT must be listed on all customs declarations.

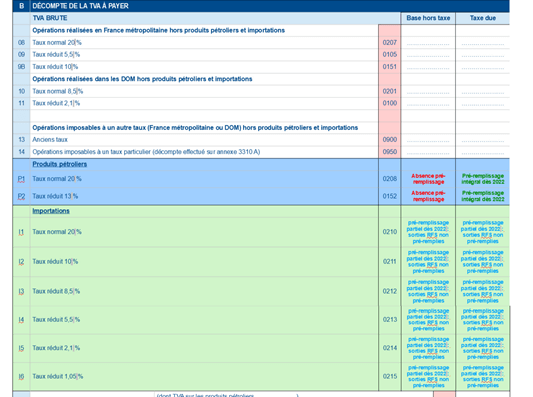

Changes to the VAT return

Changes to the French VAT return include (see Figure 1):

New fields to report import VAT and petroleum products

New numbering system for most of the return

Pre-filled information on imports – lists the amount of import VAT collected from customs items previously declared to the Directorate-General of Customs and Indirect Taxes (DGDDI). Taxpayers will have the ability to edit the pre-filled import amounts before submission

Pre-filled information will be populated from the 14th of the month following the due date

VAT returns containing import VAT will be due the 24th day of the month following the filing period

Figure 1: Draft extract of 2022 FR VAT Return

Impact on Taxpayers

From 31 December 2021, “foreign traders” who imported goods and then made local sales under the domestic reverse charge are now required to register as a result of the import portion of the transaction and will still apply the reverse charge to their sales. This will now require a new VAT declaration to be submitted.

Additionally, until 31 December 2021, a foreign company that imported goods into France and made local sales under the reverse charge had to recover the import VAT paid under the Refund Directive (EU companies) or the 13th Directive (non-EU companies). For Refund Directive claims, there would have been a cash advantage for France because either companies did not submit claims (small value) or because claims were rejected for non-compliance. For claims under the 13th Directive and the two previous considerations, there was also the issue of “reciprocity” which prevented claims from some counties such as the US, for example. Under the new regime, all import VAT is reclaimed, leading to a potential budget shortfall.

Take Action

To find out more about what we believe the future holds, download Trends and follow us on LinkedIn and Twitter to keep up-to-date with the latest regulatory news and updates.

TRENDS AND UPDATES ON VAT COMPLIANCE

Trends 13th Edition 2022

TRENDS AND UPDATES ON VAT COMPLIANCE

Trends 13th Edition 2022

Welcome to the 13th edition of Sovos’ annual Trends report where we put a spotlight on current and near-term legal requirements across regions and VAT compliance domains.

This report provides a comprehensive look at the regulatory landscape as governments across the globe are enacting complex new policies to enforce VAT mandates. It examines the demanding and unprecedented insight now required into your economic data so that regulatory authorities enforce standards and close revenue gaps.

This year’s report examines the evolution of law and practice around the four emerging megatrends that Sovos experts identified in the 12th edition. These trends, many of which revolve around tax compliance and controls being ‘always on’, have the potential to drive change in the way organizations approach regulatory reporting and manage compliance.

Authored by a team of international tax compliance experts, we provide extensive recommendations on how companies can prepare for and thrive through these changes.

Get the report

The four mega-trends that we examine are:

Continuous Transaction Controls (CTCs) – Countries with existing CTC regimes are seeing improvements in revenue collection and economic transparency. Now, other countries in Europe, Asia and Africa are moving away from post-audit regulation to adoption of these CTC-inspired approaches. The report highlights how countries like France and Hungary have accelerated their transition to CTCs, and how many jurisdictions are combining invoice controls with CTC transport documents, thereby expanding their real-time reach from financial to physical supply chains.

A shift toward destination taxability for certain cross-border transactions – Cross-border services have historically often escaped VAT collection in the country of the consumer. Due to a large increase of cross-border trade in low-value goods and digital services over the past decade, administrations are taking significant measures to tax such supplies in the country of consumption or destination.

Aggregator liability – With the increase of tax reporting or e-invoicing obligations across different taxpayer categories, tax administrations are increasingly looking for ways to concentrate tax reporting liability in platforms that naturally aggregate large numbers of transactions already. Ecommerce marketplaces and business transaction management cloud vendors will increasingly be on the hook for sending data from companies on their networks to the government, potentially even inheriting liability for paying their taxes. The report notes how the July 2021 introduction of sweeping changes in e-commerce VAT legislation via OSS and IOSS are confirming this trend.

E-accounting and e-assessment – Combining CTCs with obligations to synchronize entire accounting ledgers makes onsite audit necessary only in cases showing major anomalies across these rich data sources. Over time, the objective is for VAT returns and other tax reports to be prefilled by the tax administration based on taxpayers’ own, strongly authenticated source system data. A brief deep-dive into the origins and potential future of SAF‑T shows how this trend is evolving to become a solid companion to CTCs globally.

CTCs have emerged as the primary concern for multinational companies looking to ensure compliance despite growing diversity in VAT enforcement approaches. Tax authorities are steadfast in their commitment to closing the VAT gap and will use all tools at their disposal to collect revenue owed. This holds especially true in the aftermath of COVID-19, when governments are expected to face unprecedented budget shortfalls.

The potential costs and risks associated with the trends highlighted in the report cannot be effectively mitigated with a reactive or opportunistic approach. The digital transformation of tax administration can – if approached as just an evolution of the legacy ‘post audit’ VAT world – significantly contract the digital transformation of businesses. This report suggests an analysis framework that companies can use to ensure ongoing VAT compliance whilst maximizing the opportunities of modern information and communication technologies for their own benefit.

In addition, Trends includes a major review of the country and regional requirement profiles. These profiles provide a snapshot of current and near-term planned legal requirements across the different VAT compliance domains.

The Northern Ireland Protocol regarding goods moving from Great Britain to Northern Ireland continues to cause problems, leading to calls to suspend it via Article 16. But at the same time, some NI politicians are looking to capitalise on the possibility of inward investment by companies that can benefit from being in both the UK and the Single Market at the same time. This will be an interesting circle to square.

For goods moving from Great Britain to the EU, it has been necessary to review supply chains and VAT compliance, especially where the GB supplier is required to import the goods. Here we have the issue of theory clashing with reality, requiring plans to be revised.

Many UK suppliers selling goods into the EU decided that a good approach would be to obtain a VAT number in the Netherlands and then import the goods under an Article 23 licence to defer the import VAT to the VAT return – a straight-forward scheme to set up and manage. However, under the Union Customs Code, anyone who imports goods into the EU is required either to be established in the EU or to appoint an “indirect customs agent” who is established in the EU.

Upon accepting such an appointment, the EU entity becomes jointly liable with the importer for the VAT and duty that is due. Not surprisingly, it is difficult to find businesses that will offer such a service. In 2020, the body representing freight forwarders in Germany suggested that no such appointments should be accepted because of the financial risk. For many UK businesses, the only solution has been to establish a company in the EU, often the Netherlands, to import in their name.

Brexit also caused issues for GB businesses that supply equipment required to be installed in factories or other premises – such as parts of manufacturing production lines.

Within the Single Market there is a simplification for such supplies. The vendor can move the goods to another Member State to install them with the customer accounting for the acquisition tax due on the goods. This is because there is no need for the supplier to have a local VAT number in the Member State where the goods are installed.

Following Brexit, suppliers shipping goods from Great Britain to the EU for installation are no longer able to use this simplification. Instead, the GB supplier must now import the goods into the EU and then make a sale. If the goods are imported and installed in a Member State where the extended reverse charge applies to the sale, there will be a cash flow issue regarding the paid import VAT. Claims need to be made under the 13th Directive and, if the Member State concerned applies the concept of “reciprocity”, then the claim may be denied.

“Reciprocity” allows a Member State to refuse VAT refunds to taxpayers from third countries which do not allow VAT refunds to taxpayers of the Member State. The Member State normally publishes a list of third countries that can submit claims where reciprocity is invoked.

Pre Brexit, there was no need for the UK to be on such a list, so this now represents a real risk. Some Member States, including Spain, added the UK to their list immediately following Brexit. If these subtle complexities are not considered before a transaction is agreed the cashflow consequences could be severe – so planning is essential.

Businesses also have to ensure that they are prepared for changes which came into effect on 1 January 2022.

Under the EU-UK Trade and Cooperation Agreement, goods exported from Great Britain to the EU with a UK origin are free of import duty. In some situations, exporters require information from their suppliers about the origin of the goods they are supplying.

Until 31 December 2021, an exporter of goods from Great Britain to the EU did not need to hold a supplier’s declaration when making a statement on origin to be used by the customer to claim the zero-duty rate on imports into the EU. It is enough that the exporter is confident that the origin rules are met and make every effort to get supplier declarations retrospectively.

Suppose a UK exporter finds that a supplier statement is not available retrospectively. In that case, they must inform the EU customer who will have to consider the impact on the imports they have made.

If an exporter cannot comply with an official request for verification of the origin of the goods being the UK, the EU customer will be liable to pay the full duty rate retrospectively.

From 1 January 2022, an exporter must hold a supplier’s declaration, when required, when making the statement on origin declaration to the customer or the full rate of Customs Duty is payable. This significant change to the rules will impact all businesses exporting to the EU, including e-commerce retailers selling goods above EUR150.

Take Action

Get in touch about the benefits a managed service provider can offer to ease your business’ VAT compliance burden.