Note: On 17th of December 2025 the French Tax Authorities (DGFiP) confirmed Sovos as a certified Plateforme Agréée (PA). This means that Sovos is among the select few certified providers authorized to facilitate e-invoicing compliance in France, reflecting our solution’s robustness and our long-standing commitment to regulatory compliance.

France’s e-invoicing mandate, combined with the e-reporting obligation, provides the tax authorities with access to transaction data. This is to increase efficiency, cut costs and fight fraud. Whether you are a buyer or supplier, the mandate’s effect on businesses and their operational processes, financial systems and people is extensive.

This France e-invoicing guide will explain:

How e-invoicing in France works

Who needs to comply and when

Key information about penalties and non-compliance

E-invoicing in France: Requirements and regulations

The French mandatory e-invoice system relies on a network of private certified service providers who connect taxpayers by facilitating the exchange of e-invoices and, additionally, connect the taxpayers to the French administration’s centralized platform (PPF) thus allowing the reporting of relevant invoice data.

The French mandate consists of 3 main obligations: e-invoicing, e-reporting of invoicing data and exchange of e-invoices lifecycle statuses.

E-invoicing: all B2B domestic supplies in France carried out between established entities, including branches of foreign companies, are subject to the e-invoicing obligation, i.e., only established entities will be impacted by this obligation.

E-reporting: the e-reporting obligation is applicable to both established as well as non-established VAT registered entities, although with varying degrees of coverage. This obligation will cover transactions not under scope of the e-invoicing obligation such as B2C supplies and cross-border transactions.

E-invoice lifecycle statuses: transmitted by the PAs providing real-time visibility on the statuses of electronic invoices being exchanged in the ecosystem. Particularly concerning transactions for which tax is payable on collection, taxpayers are required to report payment statuses as well.

The accredited PAs, who exchange the electronic invoices between taxpayers and report invoice data to the PPF, must support 3 mandatory core-set formats for the exchange of electronic invoices – UBL, CII or Factur-X (a mixed human-readable and structured format) – although other structured formats may be used.

E-invoices must include all mandatory fields as defined in the Code Général des Impôts as well as those required by commercial laws.

Exchanging e-invoices directly between trading parties who are not registered as Platforme Agréées is not allowed. Invoices must be exchanged between parties through certified service providers.

E-reporting frequencies are based on the VAT regimes that taxpayers are subject to. Taxpayers subject to the monthly VAT periodic reporting regime are required to e-report invoice data every 10 days.

E-invoicing and e-reporting in France: Implementation timeline

August 2023: The French Directorate General of Public Finances (DGFiP) postponed the implementation of the country’s e-invoicing mandate

December 2023: The Finance Law for 2024 is adopted, establishing new implementation dates for the e-invoicing mandate

June 2024: French authorities published a new version of the e-invoicing mandate External Specifications file

February 2026: Testing/voluntary phase begins. This is highly promoted by the French Tax Authority, as this phase is seen as a “ramp up period” to ensure that all businesses are ready to comply with the mandatory phase from Sept 2026

September 2026: All businesses must be able to accept e-invoices. It also becomes mandatory for large & intermediate-size businesses to issue e-invoices (& comply with e-reporting regulations).

September 2027: It also becomes mandatory for all other businesses to issue e-invoices (& comply with e-reporting regulations).

Register for e-invoicing in France with Sovos

Sovos can help your business comply with the French mandate with a range of services:

Tax compliance services – to control, sign, archive and format invoicing data according to the legal requirements as well as create SAF-T (FEC) reporting for both suppliers and buyers

Sovos PA – Sovos is a confirmed Plateforme Agréée (PA)

Connectivity services – through Sovos or via our partners to deliver e-invoice, e-reporting and lifecycle status data

France’s e-reporting requirements are established alongside the new e-invoicing mandate, with the reporting frequency based on the taxpayers’ applicable VAT regime. The e-reporting requirement will complement the e-invoicing mandate by facilitating the transmission of data on B2C and cross-border B2B transactions.

In France, an electronic invoice is defined as an invoice which is issued and transmitted in paperless form, following a structured format.

France’s e-invoicing requirements come into effect during 2026-2027, depending on business size. However, from September 2026, all companies must be able to receive e-invoices through an accredited service provider (a PA).

Exchanging e-invoices directly between trading parties is not allowed. Originally it was intended that either a registered service provider (PA) or the centralized platform (Portail Public de Facturation – PPF) would transmit the e-invoice to the buyer party, which would then be able to leverage either a PA or the PPF for receiving the invoice.

However, the French Tax Authorities announced on 15 October 2024 that the PPF’s role has been significantly reduced and they will no longer handle the exchange of invoices for all companies across the country. As such, the French State’s “own free-of-charge” PA utility service will not become available to French businesses.

Therefore, all companies in scope are required to select a PA. Without the PPF being available as a free invoice exchange platform, it is estimated that 4+ million companies will now have to rely on PA-enabled accounting software to receive those transactions.

PAs are private service providers accredited by the tax authority to intermediate data flows between trading partners and the PPF. They will act as the interface between companies and the French government and will be directly involved in issuing and receiving invoices. Following the announcement, on 15th October 2024, that the PPF will no longer be acting as a free invoice exchange platform, all companies in scope are required to select a PA.

Following a rigorous evaluation process by the French Tax Authority (DGFiP), Sovos was granted its “Plateforme Agréée” (PA, formally known as a “PDP”) status, with the registration number n°0004, subject to conditions. This conditional registration recognized Sovos as one of a select few providers authorized to participate in the next phase of the DGFiP certification program, reflecting our solution’s robustness and our long-standing commitment to regulatory compliance.

These conditions required all PAs to successfully complete the official testing process organized by the DGFiP, which commenced on Tuesday, October 14th, 2025, and lasted up 3 months. Following validation by the DGFiP, final and definitive PA certification was granted to Sovos on 17th of December 2025.

There are a growing number of tax authorities that have implemented e-invoicing globally, including France, Italy, Saudi Arabia and India. There are also many countries working on implementing e-invoicing including Germany and Spain.

Italy was the first country in the region to introduce a clearance e-invoicing model with the Sistema di Interscambio (SdI) platform. Seeking to close one of Europe’s most significant VAT gaps, the government has steadily improved its Continuous Transaction Controls (CTC) system.

Beginning with B2G e-invoicing in 2014 and extending to cover domestic B2B and B2C e-invoices in 2019, Italy became the first EU country to make B2B e-invoicing mandatory through a clearance process.

This page will:

Explain how Italy’s e-invoicing works

Help you understand how to comply with the e-invoicing regulations

Answer your questions about the Sistema di Interscambio

Have questions? Get in touch with a Sovos Italy e-invoicing expert.

Issuing e-invoices requires creation in a structured format and transmission is via the Sistema di Interscambio

The Fattura PA – the tax authority’s XML schema format – is the required format for issuing e-invoices

For B2B e-invoices, businesses can choose how to ensure the integrity and authenticity of invoices, but there is a strong market preference for Qualified Electronic Signatures. However, B2G e-invoices must be electronically signed.

Exchange of National Health Service purchase orders is through the NSO platform and referenced accordingly in the e-invoice.

E-archiving invoice requirements include the obligation to:

Execute a signing and time stamping process for e-invoices in an archive

Maintain a documented description of the archive and the archiving process (Manuale della Conservazione)

Put in place a clear delegation plan setting up the responsibilities around the archiving process

Since 1 July 2022, all cross-border transactions must be reported through the SdI in the FatturaPA format. Taxpayers can continue to exchange cross-border invoices in any agreed way.

Scope of e-invoicing in Italy

B2B e-invoicing in Italy applies to:

Domestic B2B transactions between Italy resident/established taxpayers

Almost all Italy resident/established taxpayers

Included in 2022: Taxpayers who adopt the flat-rate tax regime (regime forfettario) and amateur sports associations and third sector entities with revenue up to EUR 65,000

From 1 Jan 2024: Microenterprises with revenues or fees up to EUR 25,000

B2G e-invoicing in Italy applies to:

All taxpayers supplying goods/services to public administration entities

E-invoicing in Italy: Mandate Rollout Dates

6 June 2014: Phased roll-out of mandatory B2G e-invoicing starts in Italy

1 July 2018: Clearance mandate goes into effect for manufacturers and distributors of petrol and diesel intended for use as a motor fuel in cars and road vehicles

1 September 2018: Mandate starts for tax-free sales to non-EU individuals acting as final customers

1 January 2019: Mandate becomes a requirement for domestic B2B and B2C transactions in Italy, with minor sector-specific exceptions

1 February 2020: Exchange of purchase orders for the supply of goods to entities associated with the National Health Service through the NSO platform becomes compulsory and reference in the e-invoice becomes a requirement

1 January 2021: Introduction of pre-populated VAT returns and enforcement of new FatturaPA schema

June 2021: Enforcement of the new requirements for the creation and archiving of electronic documents

October 2021: Voluntary transition phase for e-invoicing between Italy and San Marino began

1 July 2022:

Italian businesses must report information on cross-border transactions to the SDI in the FatturaPA format. As a result, Esterometro was abolished on 30 June 2022

E-invoicing using the FatturaPA format becomes mandatory between Italy and San Marino, with the Italian SdI as the access point for Italian taxpayers and the HUB-SM platform as the SdI counterpart on San Marino’s side

Scope of the B2B e-invoicing mandate in Italy broadened to include:

Taxpayers who adopt the flat-rate regime (regime forfettario)

Amateur sports associations and third sector entities with revenue up to EUR 65,000

January 2024: E-invoicing scope to include microenterprises with revenues or fees up to EUR 25,000

1 July, 2030: Italian VAT-registered businesses must comply with VAT in the Digital Age (ViDA) requirements, which include mandatory e-invoicing and digital reporting for Intra-Community B2B transactions.

Penalties: What happens if you don’t comply

Failure to issue an invoice or issuing an invoice that doesn’t meet the XML format will result in a penalty between 90-180% of the associated VAT amount.

Issuing a purchase invoice to a client without adhering to mandate requirements will result in a penalty of 100% of the associated VAT amount.

After a grace period (expired for the supply of goods and services), there will be no payment for invoices issued to entities associated with the National Health Service if no prior purchase order has been transmitted through the NSO platform and referenced in the e-invoice

Register for e-invoicing in Italy with Sovos

Sovos ensures compliance with all SdI e-invoicing and VAT requirements in Italy including CTC e-invoicing, reporting and e-archiving. All you need to do is work with us and you can use our solution that connects directly with the SdI.

E-invoicing in Italy is mandatory for the majority of the B2B, B2C and B2G invoices. Suppliers performing activities classified as “Commercio al minute e attivitá assimilate” are exempt from the obligation of issuing e-invoices, unless their customers so request them; on the other hand, those suppliers are required to electronically transmit a daily aggregate report (It.: Scontrino Elettronico). Reporting of cross-border transactions through the SDI in the FatturaPA format is also mandatory.

How does e-invoicing work in Italy?

The tax authority requires all invoices in the Fattura PA XML schema format. Transmission of e-invoices happens through the Sistema di Interscambio. E-invoices must be cleared by the tax authority. The Italian tax authority delivers the legal cleared e-invoice to the recipient.

How do you securely connect with the SdI to issue invoices?

With ease. Our solution connects securely with the SdI, freeing you from the burden of knitting together different systems and platforms.

How do you comply with Conservazione sostitutiva?

The term conservazione sostitutiva refers to a long-term preservation process required for compliant archiving of e-invoices in Italy. E-invoices must be preserved after being archived by grouping them together in a so-called ‘package’, and providing that e-invoice package with a qualified digital signature or seal and a time reference.

This process must be completed no later than three months after the deadline for the submission of the annual fiscal declaration at the end of the fiscal year. E-invoice preservation is an integral feature of Sovos eArchive for invoices stored under Italian law.

While many governments and tax authorities are now on an e-Transformation journey, this trend began in Latin America in the early 2000s. Turkey followed suit a decade later when it began the digitization of its tax system.

Turkey is further along in its e-Transformation journey than most countries – including EU Member States, which are working towards digitization in their own way with the overarching VAT in the Digital Age initiative.

From e-invoicing to electronic self-employment receipts, Turkey now has a fully-fledged, established digital tax system with many moving parts. To understand Turkey’s e-Transformation, bookmark this page then read on.

CTC Type E-invoice clearance with both parties registered on the portal

Network Centralised – e-Fatura Portal delivers the e-invoices to Buyers for B2B transactions

Format UBL-TR format

eSignature Requirement Required – fiscal stamp or qualified electronic signature

Archiving requirement 10 years

E-arşiv Fatura Turkey

CTC Type E-invoice reporting (daily basis)

Network Decentralised – e-Fatura Portal does not deliver e-arşiv invoices; it’s the taxpayers’ responsibility

Format UBL-TR format or in a free format such as PDF and must also be available in paper form

eSignature Requirement Required – fiscal stamp or qualified electronic signature

E-Transformation in Turkey

Turkey stepped up its tax system through digitization in 2012 to help important information be gathered and transmitted with ease and accuracy. It’s further ahead than many other countries, with a variety of electronic systems and documents mandated for many taxpayers – all starting with its e-Ledger obligation.

Turkey joined the eEurope+ initiative and moved fast to ensure it was keeping up with tax digitization efforts, relieving its entire economic ecosystem where information is concerned. The aims of such changes are to reduce VAT fraud, increase governmental access to and control of data, standardise financial and accounting processes and reduce errors.

Now effectively utilising electronic versions of invoices, ledgers, delivery notes, self-employed receipts and more, there are a lot of challenges for taxpayers to overcome to remain compliant amidst Turkey’s e-Transformation.

Turkey’s ambition to electronically transform its tax ecosystem required the development and implementation of many products and services. This presented taxpayers with new requirements and, subsequently, new challenges.

Here are the products and services in Turkey’s e-Transformation system:

e-Fatura

e-Fatura is Turkey’s e-invoicing initiative. Mandated for companies with turnovers of over TRY 5 million, this obligation came into effect on 1 April 2014. There are also sector-based parameters for the nation’s e-invoicing mandate, ignoring the turnover threshold, qualifying the following for an electronic invoice obligation:

Companies licensed by the Turkish Energy Market Regulatory Authority

Middlemen or merchants trading fruits or vegetables

Online service providers facilitating online trade

Importers and dealers

Turkey’s e-invoicing initiative is a clearance model and two-way application, with issued invoices needing to be in the UBL-TR format and archived for 10 years. Sovos’ e-invoice solution enables compliance with e-Fatura requirements.

e-Arşiv Fatura

e-Arşiv Fatura is Turkey’s e-arşiv invoice initiative. Taxpayers registered in the e-Fatura system must also issue e-Arşiv invoices, either in the UBL-TR format or in a free format such as PDF.

Real-time clearance is not conducted for the issuance of these invoices, though an e-Arşiv report must be submitted electronically to the tax authority by the end of the following day. e-Arşiv invoices are always created electronically but must be available in paper form unless the buyer agrees to receive the document electronically.

e-İrsaliye is Turkey’s e-WayBill initiative. The use of e-İrsaliye documents became obligatory for taxpayers that surpass the TRY 10 million revenue threshold on 1 July 2023, though those outside of the scope can voluntarily switch to electronic WayBill documents.

There are two types of paper waybills, namely shipment and transportation. e-İrsaliye largely replaces the shipment waybill.

Information required in this type of e-document includes:

Supplier information

Issue date and document number

Buyer information

Type and quantity of the transported goods

Shipment date and time

Legally, there is no difference between paper waybills and eWayBills, though the electronic version requires both parties to be registered in the national system.

e-Defter

e-Defter is Turkey’s e-Ledger initiative. The Turkish tax authorities made the e-Ledger application mandatory for e-invoice users and taxpayers, subject to independent audit, in 2015.

These e-documents must be prepared in XBRL-GL format and include specific information in standard XML format – all signed with a financial seal. In addition to producing e-ledgers, taxpayers are required to create a ledger summary which is to be sent monthly to the TRA and archived for 10 years.

Electronic ledgers reduce the time it takes to collect data, save costs associated with the notarization process and ensure compliance with tax processes.

e-Mutabakat

e-Mutabakat is Turkey’s e-Reconciliation initiative. Reconciliation is the communication between accounts to mutually agree on the debit and credit between companies that are part of an agreement.

Turkey’s tax authority has ruled that companies are obliged to make reconciliations at particular times. The last day of the year is typically the day when the account between two parties will be closed unless an agreement or legal requirement states otherwise.

The BA-BS web application developed by the TRA for e-Reconciliation enables taxpayers to compare current agreements and unbalanced agreements before electronic submission of the BA-BA forms.

e-Müstahsil Makbuzu

e-Müstahsil Makbuzu is Turkey’s e-Producer Receipt initiative. This commercial e-document is issued by farmers or wholesalers to keep a record of the products they buy from farmers that don’t bookkeep.

Taxpayers that are obliged to issue producer receipts have had to issue electronic versions of the document, known as e-Müstahsil Makbuzu, since 1 July 2020. However, fruit and vegetable brokers or merchants have been required to issue e-Producer Receipts since 1 January 2020.

Those obliged to utilise e-Producer Receipts may be outside of the scope of e-Fatura, e-Arşiv Fatura and e-Defter requirements.

e-Serbest Meslek

e-Serbest Meslek is Turkey’s e-Self-Employed Receipt (e-SMM) initiative. This obligation came into effect on 1 February 2020 and applies to all self-employed individuals, including:

Architects

Engineers

Financial advisors

Lawyers

Screenwriters, writers, composers and painters

Self-employed doctors, dentists and veterinarians

e-SMM receipts can be created, submitted and reported electronically and carry the same legal weight as paper Self-Employment Receipts. They must be archived for 10 years.

While all the above are prominent e-documents, there are even more electronic documents in Turkey that you should know about. To learn more, read our e-documents overview.

Who is affected by e-Transformation?

E-Transformation includes many documents, each subject to specific thresholds and criteria based on their type. Additionally, certain documents are mandatory for particular sectors without any threshold criteria. E-invoicing is now mandatory for the majority of taxpayers, but it is important to understand which documents are required to be submitted to the tax authorities.

The TRA continues to announce new taxpayer groups in scope of the different document types, so it’s important that businesses stay up to date with the latest information to ensure they remain compliant.

What are the benefits of e-Transformation?

Turkey’s tax transformation aimed to deliver benefits to both the government and taxpayers.

The e-Transformation initiative aims to produce the following benefits:

Real-time collection of financial data

Reduce VAT fraud and the circulation of fake invoices

Increased standardisation to automate accounting processes

Improved efficiency and reduction of manual errors through data auto-population

Tax compliance and e-Transformation

Turkey’s e-Transformation has impacted tax compliance, successfully implementing real-time transmission of important financial data.

With data automatically being populated in documents, it reduces the possibility of error via manual input and fraudulent invoices being submitted. The reduction of the VAT gap has been a driving force for many countries, including Turkey.

Eliminating paper, cartridge, shipping and archiving costs associated with paper invoices is also an advantage to businesses and government.

With over 16 document regulations, Turkey’s e-transformation system requirements are extensive and complex. Understanding which regulations apply and keeping up with the latest tax compliance guidelines is key.

How Sovos can help with your e-Transformation journey

Sovos provided the first global e-Transformation solution suite, helping businesses of all shapes and sizes to meet the demands of Turkish tax mandates. Our platform meets all the requirements, standards and formats defined by the Turkish Revenue Authority.

Organisations choose Sovos as their global compliance partner, partly due to the convenience of having a single vendor to aid compliance wherever and however they do business.

A special integrator is an intermediary service provider authorised by the Turkish Revenue Administration. Special integrators have the authority to create electronic records on behalf of taxpayers.

The General Authority of Zakat and Tax’s (GAZT) previously published draft rules on ‘Controls, Requirements, Technical Specifications and Procedural Rules for Implementing the Provisions of the E-Invoicing Regulation’ aimed to define technical and procedural requirements and controls for the upcoming e-invoicing mandate. GAZT recently finalized and published the draft e-invoicing rules in Saudi Arabia.

Meanwhile, the name of the tax authority has changed due to the merger of the General Authority of Zakat and Tax (GAZT) and the General Authority of Customs to form the Zakat, Tax and Customs Authority (ZATCA).

The finalised rules include a change to the go live date of the second phase from 1 June 2022 to 1 January 2023. They revealed the time limit to report B2C (simplified) invoices to the tax authority´s platform for the second phase.

According to the final rules, the Saudi Arabia e-invoicing system will have two main phases.

Saudi Arabia E-Invoicing System: The First Phase

The first phase begins on 4 December 2021 and requires all resident taxpayers to generate, amend and store e-invoices and electronic notes (credit and debit notes).

The final rules state businesses must generate e-invoices and their associated notes in a structured electronic format. Data in PDF or Word format are therefore not e-invoices. The first phase does not require a specific electronic format. However, such invoices and notes must contain all necessary information. The first phase requires B2C invoices to include a QR code.

There are a number of prohibited functionalities for e-invoicing solutions for the first phase:

Uncontrolled access

Tampering of invoices and logs

Multiple invoice sequences

Saudi Arabia E-Invoicing System: The Second Phase

The second phase will bring the additional requirement for taxpayers to transmit e-invoices in addition to electronic notes to the ZATCA.

The final rules state the second phase will begin 1 January 2023 and will be rolled-out in different stages. A clearance regime is prescribed for B2B invoices while B2C invoices must be reported to the tax authority platform within 24 hours of issuance.

As a result of the second phase requirements, the Saudi e-invoicing system will be classified as a CTC e-invoicing system from 1 January 2023. All e-invoices must be issued in UBL based XML format. Tax invoices can be distributed in XML or PDF/A-3 (with embedded XML) format. Taxpayers must distribute simplified invoices (i.e. B2C) in paper form.

In the second phase, a compliant e-invoicing solution must have the following features:

Generation of a Universally Unique Identifier (UUID) in addition to the invoice sequential number

Tamper-resistant invoice counter that increments for each invoice and electronic note issued

Contain some functionalities which enable taxpayers to save e-invoices and electronic notes and archive them in internal and external archive

Generation of a cryptographic stamp for each e-invoice or electronic note

Generating a hash for each generated e-invoice or electronic note

Generation of a QR code

The second stage will furthermore bring additional prohibited functionalities for e-invoicing solutions on top of requirements mentioned in the first phase:

Time change

Export of stamping key

What’s next for Saudi Arabia’s e-invoicing system?

After publishing the final rules, the ZATCA is organising workshops to inform relevant stakeholders in the industry.

Some of the details remain unclear at this point, however the Saudi authorities have been very successful in communicating the long-term goals of the implementation of its e-invoicing system, as well as making clear documentation available and providing opportunities for feedback on the documentation published for each phase. We expect provision of the necessary guidance within the near future.

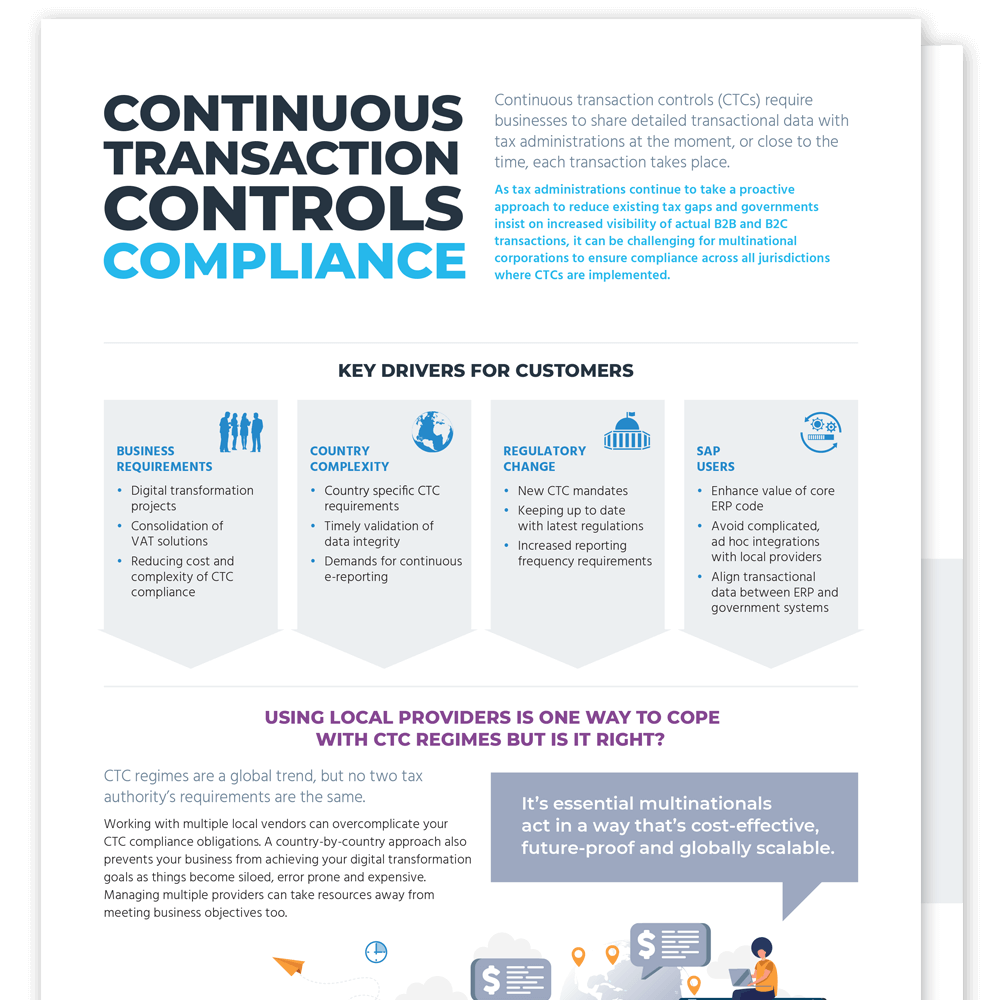

Manage Your CTC Obligations with a Global Compliance Solution Built On Local Expertise

Automate your CTC compliance management

Standardize on tax technology with continuous legal monitoring to power compliance across all business processes.

Tax administrations continue to insert themselves into the invoicing process or demand detailed records within a matter of hours or days of transactions. Sovos empowers you to comply with a cost-effective, secure, global solution to withstand the disruption of this global continuous transaction controls (CTC) trend.

Adopt a consistent global compliance strategy that scales across all jurisdictions and enterprise systems by connecting flexibly to a single provider, regardless of legal and business changes. Sovos’ VAT Compliance Solution Suite includes CTC services such as reporting and e-invoicing as integral components of a fully scalable solution suite and includes Sovos Periodic Reporting, SAF-T and Sovos eArchive.

Put CTC compliance in your digital financial core.

Stay ahead of current and future compliance obligations.

Monitor 60+ countries to track the diverse range of emerging legal frameworks and evolving specifications.

Simplify compliance vendor relationship management with a single, global point of contact.

Ensure invoices continue to flow, so your business and its supply chains run smoothly.

Minimize the need for ad hoc IT involvement and investment in compliance updates.

Save time, eliminate labor-intensive manual updates, and enhance accuracy.

Stop worrying about ever-changing different country formats and processes.

Reduce your total cost of compliance.

Managing CTC obligations

A complete global VAT compliance solution

Ease your journey to CTCs with Sovos for a scalable global VAT compliance solution built on local expertise to solve your CTC management obligations wherever you operate.

Learn more

Benefits of Sovos CTC software for SAP users

Shield ERP custom-code from change.

Empower customers to handle current and future CTCs.

Maintain ERP as a single source of truth by automating the alignment of transactional data between customer ERP and government systems.

Match acknowledgement / approval / rejection codes to original invoices and near real-time reports submitted.

The Turkish Revenue Administration (TRA) has published updated guidelines on the cancellation and objection of e-fatura and e-arsiv invoice. Two different guidelines are updated: guidelines on the notification of cancellation and objection of e-fatura and guidelines on the notification of cancellation and objection of e-arsiv.

The updated guidelines inform taxable persons about the new procedures for objection against an issued e-fatura and e-arsiv invoice. And how this must be notified to the TRA. Due to changes in the objection procedure, the e-arsiv schema has also changed. There has not yet been a change in the e-fatura schema, however it could also change in the near future. The updated guidelines state that the TRA platform can be used to notify the TRA about objection requests made against an issued e-fatura and e-arsiv invoice.

Why are the updated guidelines important?

From July 2021, electronically issued documents won’t be mentioned in the so called ‘BA and BS forms’. The BA and BS forms are generated to periodically report issued or received invoices when a total invoice amount is 5.000 TRY or more. All limited liability and joint stock companies are obliged to create and submit the forms to the TRA even if they don’t have any invoices to report.

The TRA recently published a new provision stating that electronically issued documents will not be shown in BA and BS forms and instead will be reported directly to the TRA in the clearance (e-fatura) and reporting(e-arsiv) process. Considering that the TRA receives the invoice data for electronically issued invoices in real-time, relieving taxpayers from reporting invoices through BA and BS forms creates a more efficient system in which the relevant data will be collected only once from taxpayers.

At its current stage, e-documents won’t be mentioned in these forms. However, in order for the TRA to have accurate invoice data about each taxpayer, it needs to be notified which are the final invoices and disregard any objected or cancelled documents when evaluating taxpayer data.

Although the cancellation process is already performed through the TRA platform for basic e-fatura and e-arsiv, objection requests are made externally (through a notary, registered letter or registered e-mail system), meaning the TRA does not have visibility of all objections. There could therefore be a risk that the TRA considers a cancelled document (due to objection) as issued which could result in discrepancies between the taxpayer records and the data that the TRA considers relevant for tax collection.

Therefore, taxpayers must now notify the TRA about objection requests to avoid any discrepancies between their records and BA and BS forms. The final goal of this application is that the BA and BS forms will be completely auto populated by the TRA in future.

How will the new process work?

According to the Turkish Commercial Code, any objections or cancellation requests must be made within eight days. Suppliers and buyers can raise an objection request which must be made externally (through a notary, registered letter or registered e-mail system) and registered in the TRA system.

For e-arsiv application, there are two ways for suppliers to notify the TRA about the objection request. They can either use the e-arsiv schema (automated) or register the request in the TRA portal. Buyers can see this request on the TRA platform and may respond, although they are not obliged to. Because e-self-employment receipts are also reported through e-arsiv application, the same objection rules apply.

For e-fatura, since there is no change in the schema, it is not possible for suppliers or buyers to notify the TRA using e-fatura schema. Currently, they can only notify the TRA about e-fatura objections through the TRA platform. Taxpayers can also respond to objection requests only through the platform.

What’s next?

The TRA has taken a step towards the digitalization of cancellation and objection requests. However, there is still not an automated way to perform these actions. Before the digitized objection process becomes reality in the country, the authorities must take a more sophisticated approach towards automating the process as well as introducing or amending applicable legislation.

Take Action

Get in touch to find out how Sovos tax compliance software can help you meet your e-transformation and e-document requirements in Turkey.

The Colombian electronic invoicing system is reaching maturity level. Since its inception in 2018, Colombia has been steadily consolidating and expanding the mandate to make it more stable, reliable and comprehensive.

As a result of the enactment of the recent Resolution 000013/2021, the Colombian tax administration (DIAN), officially expanded the electronic invoicing mandate to also include payroll transactions. This expansion follows the pattern established by Mexico, Brazil and other countries that already expanded the electronic invoicing mandate to payroll transactions as well.

The Support Document for Electronic Payroll is known locally in Colombia as Documento Soporte de Nomina Electronica or also simply as Nomina Electronica. It is a new digital document intended to support and validate the payroll related costs and deductions of income tax and the VAT credits (if applicable) when businesses make payments resulting from labor, legal, and other similar types of relations (pensions).

In simple terms, labour cost transactions should be reported under this new digital system for them to be valid. This is whenever employers make payments for wages, salaries, reimbursements, pensions etc.

Who is required to comply with the electronic payroll mandate?

Employers paying wages under a labor relation, where payments are reported as expenses for income tax purposes or as deductible taxes for VAT, need to comply. However, there are important exceptions derived from that legal framework. For instance, public offices, non-for-profit entities or taxpayers under the simplified regime are not currently required to comply. Consequently, they do not need to use such payments for deductions of income tax or VAT.

Schedule of deployment

The DIAN established an implementation schedule based on the number of employees the taxpayer has in the payroll. There are four stages or groups subject to the following deadlines:

Group

Deadline to start the generation and remittance of the document

Number of employees

From

Up to

1

1 September 2021

More than 250 employees101

2

1 October 2021

101

250

3

1 November 2021

11

100

4

1 December 2021

1

10

Deadline for remittance

As the Nomina Electronica is required to be reported monthly, the payments for each month should be reported by the 10th day of the next month as a result. The adjustment notes should be reported within the same deadline, once they have been made by the employer.

Reporting elements of the electronic payroll mandate

There are two basic types of reports that are parts of this mandate: the Support Document of the electronic payroll, and – when necessary – the Adjustment Note.

Support Document of Electronic Payroll or Nomina Electronica

This electronic document contains the information supporting the payments made to employees as wages and other compensations, deductions and the difference between them made by the employer, as reported in the payroll. The employer must then generate and transmit the document to the DIAN using the XML format established in the technical documentation included in the regulation 000037/2021.

Adjustment Notes

In this mandate there are no credit notes as we know them in the electronic invoice system of Colombia. However, when an employer needs to make corrections to the Support Document of Electronic Payroll reported to the DIAN, it can issue what we know as Adjustment Notes (or Notas de Ajuste) where the employer will be allowed to correct any value previously reported to the DIAN via the Nomina Electronica.

Content and structure of the reports

Employers must submit reports to the DIAN individualised for each beneficiary receiving payments from the employers. As a result, the report requires the provision of some mandatory information for the DIAN to validate. This includes the proper identification of the report itself, the reporting party, in addition to the employees, wages or other payments employees, date, numbering, software etc.

Another mandatory information element that is worth mentioning is the CUNE or Unique Code of Electronic Payroll Support Document. This is a unique identifier for each Electronic Payroll Support Document. It will allow exact identification of each report or the Adjustment Notes issued after it. However, there is some additional optional information that can be provided depending on the needs or convenience of the employer making the report.

From a technical perspective, neither the Support Document of the Electronic Payroll nor the Adjustment Notes are based on the UBL 2.1 structure used in Colombia for the electronic invoice. This is because the UBL standard does not include modules for payroll transactions or reports. Therefore, the DIAN has based its architecture in a different XML standard. Each report requires a digital signature. For that, the taxpayer can use the same digital certificate used for signing electronic invoices.

Generation, transmission and validation

The current regulations do not require that the Nomina Electronica or the Adjustment Notes should be generated by a particular software solution or by a software provider authorized by the DIAN. Taxpayers have the option to generate the report using their own solution. That is a market solution or a solution that the DIAN will provide for small taxpayers. However, all reports should strictly follow the technical documentation issued by the DIAN within the Resolution 000037/2021. The remittance of those documents is electronic, using the webservices specified by the DIAN.

After making the transmission, the DIAN then validates the document. They will then report back the corresponding application response to the taxpayer, indicating its acceptance and validation. Only then, will the amounts reported in the payroll document are valid expenses for the deduction.

Penalties and sanctions

Non-compliance with electronic payroll in Colombia will be subject to the same fines and penalties established for not complying with the electronic invoicing mandate, as defined in Art. 652-1 of the Tax Code of Colombia (Estatuto Tributario). But the most important implication of non-compliance is that any payment not reported by the employer, will not be allowed as expenses for income tax or VAT purposes when applicable.

An amendment in the General Communiqué No. 509 has announced healthcare service providers and taxpayers providing medical supplies and medicines or active substances must use the e-invoice application from 1 July 2021.

The mandated scope for transition to e-invoice and e-arşiv invoice applications in the healthcare industry

Published in the Official Gazette the implementation will cover healthcare service providers who have signed contracts with the Social Security Institution (SSI) and all taxpayers providing medicines and active substances and medical supplies.

This includes:

Hospitals, medical centres, branch centres, dialysis facilities

Other specialised treatment centers licensed by the Ministry of Health

Diagnosis, medical examination and imaging centres

Laboratories, pharmacies, medical device and material suppliers

Optometry organisations, auditory centres, spas

Private legal entities providing or producing human medicinal products, in addition to their unincorporated branches and pharmaceutical warehouses.

The transition process to e-invoice and e-arşiv invoice applications in the healthcare industry

Within this scope, organisations must use the e-invoice application as of 1 July. Organisations signing contracts with SSI after this date must use e-invoice prior to their issue of invoices to SSI.

From 1 January 2020 all organisations included in the e-invoice application scope have to apply the e-arşiv invoice on the date of e-invoice application. Any healthcare organisations included in the amendment will then have to apply the e-arşiv invoice on 1 July.

What are the benefits of e-invoice and e-arşiv invoice transition to the healthcare industry?

The digitisation process will minimise physical contact, a significant benefit following the Covid-19 outbreak. Furthermore, organisations will no longer have to prepare or store physical documents as they are stored electronically.

For organisations that issue invoices to SSI, transactions such as payment terms will become faster and more efficient via the e-invoice and e-arşiv invoice applications. In addition to the transfer of all invoice-related processes to the digital environment.

Organisations that carry out the e-issuance process via the TRA Portal or via a third-party integrator will benefit from easy access to documents, improved efficiency, and business continuity as a result.

Take Action

Get in touch to find out how Sovos tax compliance software can help you meet your e-transformation and e-document requirements in Turkey.

The new ‘Guidelines for the creation, management, and preservation of electronic documents’ (“Guidelines”) regulate different aspects of an electronic document. By following the Guidelines, businesses benefit from the presumption that their electronic documents will provide full evidence in court.

The postponement of the introduction of the Guidelines is a reaction from the AGID to claims of local organizations who have particularly expressed concern about the obligation to associate metadata with e-documents. The Guidelines set forth an extensive list of metadata fields for keeping alongside e-documents in a way that will enable interoperability.

Metadata requirements modified

In addition to delaying the introduction of the new e-document legislation, the AGID has also modified metadata requirements. They included new pieces of metadata and changing the description of some fields. The AGID has also corrected references – especially to standards – and rephrased statements to clarify some obligations.

The updated Guidelines and their corresponding Appendices are available on the AGID website.

Russia introduces a new e-invoicing system for traceability of certain goods on 1 July 2021. Federal Law No. 371-FZ will amend the Russian Tax Code to introduce the new procedure for the traceability system, which will bring the introduction of mandatory e-invoicing for taxpayers dealing with traceable goods.

Since its introduction, B2B e-invoicing in Russia has remained voluntary. However, this is changing as of this summer when the issuance and acceptance of e-invoices will be mandatory for taxpayers trading goods subject to the traceability system.

What is the traceability system?

The traceability system aims to monitor the movement of certain goods imported into Russia and the Eurasian Economic Union (EAEU). In the scope of the traceability system, each consignment of goods is assigned a registration number during import. This is then controlled at all transaction stages. Businesses within the scope of this new traceability system will need to include the registration number in invoices and primary accounting documents. They must also provide information on the transactions involving the traceable goods through VAT returns and related transaction reports.

Legal entities and individual businesses participating in the circulation of traceable goods are in scope of the traceability requirements. From 1 July 2021, invoices for these goods must be electronic. Buyers of goods subject to traceability must accept invoices in electronic form. Furthermore, the new requirement for mandatory electronic invoices for sales of traceable goods doesn’t apply to export/re-export sales and B2C sales.

What type of goods are subject to the traceability requirements?

The goods included in the list of traceable goods are currently:

Refrigeration and freezing equipment (refrigerators, freezers)

Industrial trucks (forklift trucks, bulldozers, graders, planners, power shovels, excavators, shovel loaders, tampers in addition to road rollers)

Washing and drying machines (household and for laundry facilities)

Monitors and projectors (not including receiving television equipment)

Electronic integrated circuits and elements

Baby strollers and child safety seats

What’s next for Russian regulation of electronic documents?

Considering that by the end of 2024 Russia aims to have 95% of invoices and 70% of waybills in electronic form, it’s likely more digitization changes are coming. The digitization of accounting records is another area the Russian tax authority is making progress on. It would therefore not come as a surprise to see more changes in the Russian legislation in the next couple of years.

Take Action

Get in touch to discuss the July 2021 e-invoicing requirements in Russia. Download VAT Trends to discover more about CTCs and how governments across the globe are enacting complex new policies to enforce VAT mandates.

It’s good to see light at the end of the tunnel. Nonetheless, it’s too little, too late for many smaller – but also plenty of larger – companies. Thousands couldn’t weather the storm because they were particularly dependent on human contact. Others were affected disproportionally simply because COVID-19 hit them just as they traversed a difficult period in their life cycle. As we see the first successes of anti-COVID-19 vaccines, businesses and markets are gaining confidence that by the last quarter of 2021, countries will be back at a new cruising speed. With a few notable exceptions, many of the world’s strongest economies will take years to recover from the aftermath.

Internet to the rescue – but flaws remain

As with all crises, the past year has accentuated weaknesses and accelerated failures. Whilst it must be acknowledged that the COVID-19 crisis would have been far worse without the internet and the current state of technology adoption worldwide, remaining pockets of legacy processes where companies were lagging in their digital transformation have become highlighted as employees struggled to balance health concerns with the imperative to keep things running in deserted offices and data centers.

One area where inefficiencies have been exposed is on-premises software. Many companies have started adopting cloud-based software to support different categories of workflows and connections with trading partners; however, many larger companies have been reluctant to move core enterprise systems – such as ERPs, logistics or reservation systems – to the cloud. The reason behind this reluctance is often that legacy systems have been highly customized. Whilst many enterprise software vendors offer public-cloud versions that present many benefits over on-premises deployment in theory, the practical challenges of adapting organizations and processes to ‘canned’ workflows designed around standard best practices have often outweighed them.

Another set of challenges are more intricate. Manual processes still dominate in order and invoice management across companies of all sizes globally. Where workflow software allows accounting personnel to access the system remotely, approvals and postings could be managed from home offices, but the prevalence of paper in many vendor and customer relationships still required people to manage scanning, printing, and mailing or – yes – faxing key documents from offices with limited access.

These problems will be harder to overcome, as expensive industrial-strength machines for the processing of paper documents cannot easily be put in home offices. The answer to this challenge doesn’t lie in creative ways to convert people’s kitchens into scan or print centers, but in finally taking the big leap towards end-to-end data integration.

The good, the bad and the ugly of tax as an automation driver

Interestingly, if COVID-19 isn’t enough of a reason to take that automation leap, businesses can expect a helping hand from tax administrations. Many countries had already started large-scale programs to push continuous transaction controls (CTCs). Such as mandatory real-time clearance of digital invoices. The current global health crisis is pushing tax administrations to accelerate these programs. We have seen announcements of plans towards such compulsory e-invoicing or digital reporting of accounting data in countries like France, Jordan and Saudi Arabia. In addition to several countries including Poland and Slovakia who stated their intent to follow in the footsteps of countries in Latin America and also European frontrunners like Italy and Turkey. Even in Germany, which has long resisted the call of CTCs, a significant political party has proposed decisive action in this direction.

These initiatives are still often motivated by the need to close tax gaps. However the need for resilience in revenue collection is clearly another driver. Also, examples from countries like Brazil have shown that CTCs massively improve governments’ ability to track and monitor the economic effects of a crisis down to the smallest sectoral detail. This gives them granular data that can be used for surgical fiscal policy intervention to guide the most severely affected activities through a crisis.

With all circumstances conspiring to give businesses a reason to get across that last mile towards full automation – the interface between their and their trading partners’ sales and purchasing operations – you would think that companies are now putting plans in place to get ready for a fully digital, much more resilient set of processes and organizational structures.

Unfortunately, the way that CTC mandates get rolled out and the way that companies respond to them have historically rather slowed down investment in business process automation and the adoption of modern cloud-based enterprise software.

CTC mandates are unbelievably diverse, ranging from a full online second set of accounting books to be maintained through – among other things – additional classification of supplies in the government-hosted system in Greece, to a completely different setup including service providers and transaction payment reporting being designed in France. Representatives from China are talking about blockchain-based invoicing controls, whilst countries like Poland and Saudi Arabia prepare for centralized, government-run invoice exchange networks. Mandate deadlines tend to be too short, and tax administrations make countless structural adjustments – each typically also with short deadlines and only available in local language – during implementation periods and for years thereafter.

Tax administrations could however claim with some legitimacy that deadlines are always too short, almost regardless of how much transition time taxpayers are granted, because many businesses structurally prepare too late. The global trend towards CTCs, SAF-T and similar mandates has been apparent to companies for years, yet many are ill-prepared; particularly many multinational businesses continue to consider that VAT compliance is a matter to be resolved by local subsidiaries, which step by step creates a massive web of localized procedures which rather than corresponding to corporate best practices were designed by tax administration offices.

Creating a virtuous circle towards tax automation during Covid-19

Which brings us back to why companies aren’t adopting flashy new releases of enterprise software packages in public cloud mode. Or further automating their trading partner exchanges, more quickly. All parties in this equation want the same thing. That is seamless and secure sharing of relevant data among businesses, and between businesses and tax administrations. However kneejerk reactions to regulatory mandates by businesses, and lack of tax administrations’ familiarity with modern enterprise systems, are creating the opposite effect. Companies panic-fix local mandates without a sufficient understanding of the impact of their decisions. Neither on their future ability to innovate and standardize. The enterprise resources come first to put systems in place post-haste. They then manage the problems stemming from adopting a patchwork of local tax-driven financial and physical supply chain data integration approaches. This comes from IT budgets that then don’t get spent on proper automation.

Several things can break this vicious circle. Businesses should change their way of addressing these VAT digitization changes as revolutionary rather than evolutionary. By being well informed and well prepared, it is possible to adopt a strategic approach to take advantage of CTC mandates rather than suffer from them. Tax administrations must do their part by adopting existing good practices in designing, implementing, and operating digital platforms for mandatory business data interchange purposes. The ICC CTC Principles are an excellent way to give the world economy that much-needed immunity boost, allowing businesses and governments to improve resilience while freeing up resources locked up in inefficient manual business and tax compliance processes.

But human expertise and technology can go hand in hand, with tech supporting teams and boosting productivity tenfold. As a result, for businesses, the only way to thrive in an increasingly digital world is to invest in the right technology.

For organisations operating globally, this is of particular importance as an extensive knowledge of governmental financial legislation in many countries is needed. Financial frameworks are complex to navigate and are constantly changing. Real-time VAT reporting is increasingly prevalent worldwide, with continuous transaction controls (CTCs) tightly constricting many different jurisdictions. Without automation, the hours required to manually keep pace with new rules would far exceed realistic human capacity.

For global companies, manually submitting the paperwork for audits and reports is neither sustainable nor sensible. But an additional problem for those operating in multiple jurisdictions is how to keep pace with ever changing rules and government regulations required for business transactions.

Digital governments

Global governments are reviewing how they measure and collect tax returns. The aim is to improve economic standards in their countries. Digitising return processes gives way for a much more forensic and accurate view of a nation’s economic health. So it’s unsurprising that automated invoicing and reporting has pushed its way to the top of the agenda in recent years.

How the approach is taken to upgrading many transactions and interactions is contingent on specific country viewpoints – certain jurisdictions enforce varying levels of CTCs, real-time invoicing, archiving and reporting of trade documentation. Therefore those operating internationally will feel the additional pressure to accurately track and comply with multiple and complex laws with threatening hefty non-compliance fines. Trading and operating within the law now requires intelligent technology and infrastructure.

Approaches across the globe differ; Latin America pioneered mandatory B2B clearance of e-invoices, and Brazil requires full clearance through a government platform. In Europe, the EU-VAT directive prohibits countries from introducing full e-invoicing – though Italy bucked this trend in 2019, following a lengthy derogation process. As economies shift to a data-driven business model, the move towards a digital tax regime is inevitable.

Machine learning

The VAT gap continues to confound governments across the globe. Therefore to combat it, many nations have created their own systems. In turn, this makes a patchwork of mechanisms unable to communicate with each other. To add to this, the slow adoption of e-invoices in many countries has caused a completely fractured picture – VAT information is still being reported periodically in many countries, with each jurisdiction setting its own standard. We’re a long way from consistency in global digitisation.

As more countries develop their own specific take on digitising invoicing, things look increasingly complex. New regulatory legislation continues to surface and keeping track can cause headaches and accidental noncompliance. Global firms must maintain a keen eye on developments as they happen in all the countries where they operate and its essential they apply systems which can track and update new legislation as it happens.

Flexible APIs

But tech also needs to give an accurate reflection of an entire business’ finances. It needs to link together all the different systems to accurately report tax. This is why flexible APIs are the first order of priority. Programmes with sophisticated APIs enable tax systems to ‘plug in’ to a business and gather vital information. In turn allowing firms to showcase the necessary data, display accurate results and avoid government penalties. It’s essential that technology can integrate with a number of billing systems, ERPs, and procure-to-pay platforms when approaching sensitive government interactions. The volumes of data created and handled are enormous, and increasingly out of the realms of human possibility.

Likewise, tech can assist in formatting information as per the requests of each country, which is essential for digital reporting. Technology exists to monitor and adjust invoice formats. For example, to suit the country a business is operating in and avoid non-compliance penalties. With time usually of the essence and in short supply, tools that automate admin and free up time for strategic elements of business finance pay for themselves in dividends. Effectively, as machines are increasingly ingrained in operations, manual analytics become more challenging. Both governments and businesses are leaning on automation and advanced technology to ease the resulting administrative burdens.

Automate to comply

A truly digital future is in the grasp of many economies, but it comes at a price. To capitalise on the rapid wave of digital transformation, businesses must arm themselves with technology. It’s time to manage the increasing realm of complex and data-driven regulations. It makes sense to invest in tech and automation to handle labour-intensive analysis and research, streamline processes, and alleviate the burdens faced by finance teams. That is without the need for costly expert staff or outsourced support. On the verge of a fully digital way of working, manually submitting the paperwork for audits and reports is no longer practical.

It is important to carefully select technology to synchronise and communicate vital information across a business’ IT infrastructure. In the current recession driven context, the pressure on finance teams is intense. The pressure to perform at their best, safeguard against any financial leaks and strictly monitor expenses and outgoings. In the face of adversity, tech can guide and support us – and could become business critical.

Investing in automation and tech doesn’t have to cost finance jobs. It can instead go hand in hand with human expertise. It can manage arduous and complex tasks. While also freeing up time and energy so businesses can concentrate on what they do best.

France is introducing continuous transaction controls (CTC). From 2023, France will implement a mandatory B2B e-invoicing clearance and e-reporting obligation. With these comprehensive requirements, alongside the B2G e-invoicing obligation that is already mandatory, the government aims to increase efficiency, cut costs, and fight fraud. Find out more.

France shows a solid understanding of this complex CTC subject, but some questions remain.

Introduction

France announces VAT changes spurred on by international reforms for continuous controls of VAT transactions (“Continuous Transaction Controls” or “CTCs”). The French government aims to increase efficiency, cut costs and fight fraud through the roll-out of mandatory B2B e-invoice clearance. This coupled with an e-reporting obligation gives the tax administration all relevant data for B2B and B2C transactions. This will start with large companies.

A mixed CTC system

In the report ‘VAT in the Digital Age in France’ ( La TVA à l’ère du digital en France), la Direction General des Finances Publiques – or DG-FIP – describes its aim to implement this mixed solution. Whereby mandatory clearance of e-invoices (ideally for all invoices, without exceptions such as threshold amounts etc) will lay the foundation.

This will provide the tax authority with data relating to any domestic B2B transaction. However, in order to effectively be able to combat fraud, including the carousel type, this is not enough; they need access to all transaction data. Therefore, data that the tax authority will not receive as part of the e-invoice clearance process – notably B2C invoices and invoices issued by foreign suppliers that will not be subject to a domestic French mandate, as well as certain payment data – will be subject to a complementary e-reporting obligation. (The requirement to report this latter data electronically does not mean that the underlying invoices must be e-invoices; parties can still transmit in paper between themselves.)

The Clearance architecture

The report describes how the DG-FIP has considered two potential models for the e-invoice clearance process. This is via the central Chorus Pro portal (currently the clearance point for all B2G invoices). These are the V and the Y model.

In the V model there is one public platform that serves as the clearance point; the central Chorus Pro platform is the only authorized platform via which the invoice can be transmitted to the buyer, or where applicable, the buyer’s service provider.

The Y model includes in addition to the central platform certified third-party service providers, which are authorized to clear and transmit invoices between the transacting parties. This alternative is the preferred option by the service provider community. For that reason – and as this model is more resilient because it is not exposed to a single point of failure – the report appears to favour the Y model.

Timeline

As to the timeline, starting in January 2023, all companies must be able to receive electronic invoices via the centralized system. When it comes to issuance, a similar roll out as for the B2G e-invoice mandate is envisaged, starting with large companies.

By 1 January 2023, large companies will be subject to the e-invoice issuance and also the e-reporting mandate

For medium-sized companies these obligations will apply from 1 January 2024

The smallest companies would have until 1 January 2025 to comply

Challenges and road ahead

The report lays a good foundation for the deployment of this mixed CTC system. However many issues will need to be clarified to allow for smooth implementation. Some of which quite fundamental.

The proposed model means that the French tax administration needs to think through the details of service provider certification.

The relationship between the proposed high-level CTC scheme with pre-existing rules around e-invoicing integrity and authenticity. The French version of SAF-T (FEC) and digital VAT reporting options need to be clarified. On that last topic, the French budget law for 2020 that initiated this move towards CTCs suggested that prefilled VAT returns are among the key objectives, even if this does not feature prominently in the DG-FIP report.

Some questions remain about the central archiving facility associated with the CTC scheme.

The proposed central e-invoicing address directory requires careful design (including maintenance) and implementation.

The report proposes a progressive and pedagogical deployment. This will ensure that businesses will manage this -for some radical – shift to electronic invoicing and reporting. The ICC’s practice principles on CTC are referenced, specifically noting the importance of early notice and ICC’s advice to give businesses at least 12-18 months to prepare. The first deadline comes up in just over two years’ time. It leaves only 6-12 months for the French tax administration to work out all details and get the relevant laws, decrees and guidelines adopted. This is if business should have what ICC believes is a reasonable time to adapt.

As anticipated, further information has been published by the Portuguese tax authorities about the regulation of invoices. Last weeks’ news about the postponement of requirements established during the country’s mini e-invoice reform, and the withdrawal of a company’s obligation to communicate a set of information to the tax authority, culminated in the long-waited regulation about the unique identification number and QR codes.

Back in 2019, the Law-Decree 28/2019 introduced the unique identification number and QR code as mandatory invoice content. Previously expected to be enforced on 1 January 2020, the details about what constitutes such a unique identification number and the content of the QR codes were missing. However, the Portuguese government has now published an Ordinance further regulating both requirements.

A new validation code

According to the Ordinance 195/2020, as of 1 January 2021, companies issuing invoices under Portuguese law must communicate the series used in invoices to the Portuguese tax authorities, prior to it being applied. Once the series has been communicated, the tax authority issues a validation code for each reported number series.

This validation code is later used as part of the unique identification number that has been named ATCUD. The ATCUD comprises the validation code of the series and a sequential number within the series in the format “ATCUD:Validation Code-Sequential number”. The ATCUD must be included in all invoices immediately before the QR code and be readable on every page of the invoice.

To obtain a validation code, taxpayers must communicate the following data to the Portuguese tax authority:

The identification of the document series;

The type of document, following the document types established in the SAF-T (PT) data structure;

The starting number of the sequential number used within the series;

The date when the taxpayer is expected to start using the series to which a validation code is required;

Once approved, the tax authority creates a validation code with a minimum size of eight characters.

According to the Ordinance, the sequential number that is also part of the ATCUD is a reference obtained from a specific field of the Portuguese version of the SAF-T file.

Although the Ordinance meant to introduce QR code details, it states that technical specifications will be published on the tax authority’s website. The Ordinance nevertheless says that a QR code should be included in all invoices and documents issued by certified software. It also states that the QR code should be included in the body of the invoice (on the first or last page) and be readable. Technical specifications for the QR code are available from the tax authority’s website.

Last week’s Ordinance doesn’t change the scope of companies that need to use certified software to issue invoices, nor does it change the certification requirements. However, Portuguese taxpayers must, once again, adapt their current business and compliance processes and are under pressure to change their systems before the 1 January 2021 deadline.

On 22 June, the joint Ministerial Decision that sets forth the myDATA framework was published. The decision specifies, among other things, the scope of application and applicable exemptions, the data to be transmitted, transmission methods and procedures, applicable deadlines and how transactions should be characterized.

Starting from January 2021, the required data must be reported to the myDATA platform in real-time. For information relevant to the year 2020, taxpayers have been awarded more breathing room: until the end of this year, the required data can be reported within 5 days after the issuance of an invoice, but not later than the 20th of the following month.

The implementation of myDATA will be performed in a phased manner, with ERP-based reporting of outbound and inbound data with their respective classifications starting from 1 October 2020. If a myDATA accredited e-invoicing service provider (according to the rules of the new framework) is used for e-invoicing, the reporting to myDATA through a service provider is possible from 20 July 2020.

A closer look at e-invoicing developments

To encourage businesses to adopt e-invoicing, the Ministry of Finance, through a draft bill published on 19 June, provided a number of incentives for businesses to use e-invoicing facilitated through service providers until the end of 2022.

The incentives provided are:

The statute of limitation for fiscal matters (the period during which a tax audit can take place) is reduced from 5 years to: a) 3 years for the issuer and b) 4 years for the receiver.

The deadline for processing tax refund claims is reduced to 45 days (from 90 days currently).

Twice the amount of the cost incurred for acquiring the technical equipment and software required for the implementation of e-invoicing is depreciated.

Twice the amount of the cost incurred for the issuance, exchange and archiving of e-invoices for the first year is recognized as a tax-deductible item.

Based on these recent developments, it is clear that the Greek government wishes to promote the adoption of e-invoicing in Greece but does not yet go so far as to make it mandatory. A decision specifying the details of the e-invoicing scheme is expected to be published by the IAPR in the very near future.

Update: 20 November 2023 by Dilara İnal

E-invoicing systems in the Middle East and North Africa are undergoing significant transformations, aiming to modernise the financial landscape and improve fiscal transparency. Recent updates have seen numerous countries implementing electronic invoicing solutions designed to streamline tax collection and reduce VAT fraud.

E-invoicing Trends in the Middle East

Saudi Arabia has made significant strides in e-invoicing, leading the way in the Middle East. The country has advanced to the second phase of its e-invoicing mandate where B2B invoices require clearance from the tax authority. As of November 2023, the Zakat, Tax and Customs Authority has announced eight waves of its Phase 2 integration – targeting taxpayers with varying annual turnover thresholds.

While Israel is not adopting a mandatory e-invoicing regime, the country is moving towards requiring taxpayers to submit their invoice data electronically. This move aims to tackle the issue of fictitious invoices. The Israeli invoicing model, a continuous transaction control (CTC) clearance system, is slated for a phased implementation starting in 2024.

The United Arab Emirates has also joined the movement, announcing its ‘e-billing system’ to implement mandatory e-invoicing for B2B transactions in phases.

In other jurisdictions in the region, Oman is poised to implement mandatory e-invoicing in 2024 and Bahrain has invited technology vendors to construct its central platform for an upcoming e-invoicing system. Lastly, Jordan is reported to be exploring the adoption of a mandatory e-invoicing regime.

E-invoicing Trends in North Africa

Egypt introduced a mandatory e-invoicing system for B2B transactions in 2020 with a phased roll-out schedule but, as of April 2023, all companies in Egypt are covered by this mandate. In addition to e-invoicing, there is an e-receipt system in Egypt for B2C transactions.

Tunisia’s mandatory e-invoicing system, which rolled out in 2016, covers B2G and some B2B transactions. Also, Morocco is expected to join the ranks of countries where mandatory e-invoicing applies.

With the VAT landscape in the Middle East and North Africa rapidly evolving, tax digitization regulations necessitate close and continuous monitoring.

Read our E-invoicing Guide for more in-depth information about electronic invoicing’s development and adoption, globally.

Update: 24 June 2020 by Selin Adler Ring

The concept of e-invoicing as a vehicle for increased tax control and cost reduction, continues to spread into new areas of the world. The number of countries adopting e-invoicing regimes are rising in the Middle East and North Africa as both governments and businesses by now are well-aware of the benefits. While some countries in these regions have already embraced e-invoicing, others are on their way to adopt Continuous Transaction Controls (CTC) systems. Even though the countries in these regions follow different approaches, the initial goal is the same: digital transformation of tax controls.

E-invoicing Trends in the Middle East

In the Middle East there are many moving pieces. The United Arab Emirates, Saudi Arabia, Oman and Qatar have already permitted e-invoicing. Following the introduction of VAT in January 2018, Saudi Arabia also started promoting a national electronic invoicing platform called ESAL. Oman and Qatar have yet to implement VAT but once they have, e-invoicing will be even more significant for these countries and they’ll take inspiration from other countries in the region that are moving towards CTC regimes.

In Jordan, the tax authority is conducting research to analyze CTC regimes in different countries, which is a strong signal that they too may very soon announce their intention to introduce a new CTC e-invoicing system.

Israel has recently revealed its new CTC regime plans and advised accounting software vendors to prepare for the upcoming CTC regime. After Israel’s adoption of a CTC regime, developments in the region will accelerate in a domino effect.

E-invoicing Trends in North Africa

Tunisia is a pioneer for e-invoicing. Since 2016, electronic issuing of invoices has been regulated in the Finance Law and e-invoicing is mandatory for larger taxpayers. The Tunisian e-invoicing regime requires e-invoices to be registered by a government appointed authority and therefore falls within the CTC framework.

Another country quickly moving towards a CTC framework is Egypt. The Egyptian Government has for some time been assessing best practices for CTC regimes. Finally, in April 2020, a decree mandating e-invoicing for all registered businesses was published in the country. However, the details of the e-invoicing system are yet to be disclosed. The technical controls and conditions to be adhered to and the stages of implementing the e-invoice system will be defined by the Egyptian Tax Authority.

Morocco has also been watching different e-invoicing systems. After Egypt’s e-invoicing initiatives, the Moroccan Government is a likely candidate to make a similar move towards mandating e-invoicing for taxpayers registered in the country.