The long-awaited Royal Decree, establishing invoicing and billing software requirements to secure Spanish antifraud regulations, has been officially published by the Spanish Ministry of Finance.

The taxpayers and SIF developers, defined further below in this article, must be aware of several new official deadlines set forth by the Spanish tax authority in the Royal Decree:

From 1 July 2025: Only ordinary SIF or Verifactu-approved billing systems may be used to prepare and submit invoices for the taxpayers under scope

Billing software developers and sellers must offer their product fully adapted within a maximum period of nine months from the approval of the Ministerial Order that specifies all the technical details, which is still to be approved

Therefore, companies that fall within scope must ensure their computer systems are adapted to this regulation as of 1 July 2025.

Looking for more information on tax compliance in Spain? This page can help.

Update: 10 February 2023 by Carolina Silva

Understanding Spain’s Verifactu system

The Spanish government is pursuing various routes for digitizing tax controls, including introducing software requirements on the billing system.

In February 2022, Spain published a Draft Royal Decree establishing invoicing and billing software requirements to secure Spanish antifraud regulations.

The Draft Decree ensures billing software meet the legal requirements of integrity, conservation, accessibility, legibility, traceability and inalterability of billing records. It sets standards for systems known as SIF (Sistemas Informaticos de Facturación).

To comply with SIF standards, taxpayers may use a Verifactu system – a verifiable invoice issuance system which is further detailed later in this article.

Since publishing the Draft Decree and concluding its public consultation, the Spanish tax authority has released draft technical specifications for the Verifactu system and a list of modifications to be introduced to the Draft Decree. One is the estimated date of entry into force of the billing software requirements.

What is a Verifactu billing system?

Among the many SIF requirements established in the Draft Decree is the capability to generate a billing record in XML format for each sale of goods or provision of services. This needs to be sent to the tax authority simultaneously or immediately before the issuance of the invoice.

The Draft Decree establishes two alternative systems taxpayers can adopt to comply with the technical standards of the SIF: the ordinary SIF and the Verifactu system.

A Verifactu system is a verifiable invoice issuance system, and its adoption is voluntary under the Draft Decree. Taxpayers who use computer billing systems to comply with invoicing obligations may choose to continuously send all the billing records generated by their systems to the tax authority.

A Verifactu billing system complies with all the technical obligations imposed by the Draft Decree., Taxpayers use the system to effectively send all billing records electronically in a continuous, automatic, consecutive, instantaneous, and reliable manner.

Benefits of the Verifactu billing system

A taxpayer opts for a “verifiable invoice issuance system” by systematically initiating the transmission of billing records to the tax authority. If the systems are Verifactu, invoices must include a phrase stating so.

There are several benefits for taxpayers who decide to opt for a Verifactu system:

As companies send the billing records to the tax authority, the formal acceptance response will automatically incorporate the information from such records into the taxpayer’s book of issued invoices.

Current deadlines

Taxpayers and SIF developers must be aware of several deadlines set forth by the Spanish tax authority. These are still part of the draft development of the SIF and official deadlines are outstanding:

From 1 July 2024: Only ordinary SIF or Verifactu-approved billing systems may be used to prepare and submit invoices. The Draft Decree deadline was 1 January 2024, but the Spanish authority postponed it following a public consultation.

Billing software developers and sellers must offer their product fully adapted within a maximum period of nine months from the regulation’s entry into force.

Also within nine months, the Spanish tax authority must ensure that the service for receiving billing records for the Verifactu systems becomes available.

What’s next?

Although still in draft form, it’s expected there will be official publication of the Draft Royal Decree – along with a Ministerial Order detailing the technical and functional specifications of the billing systems. Official publication of the Verifactu technical specifications is to come.

The Draft Decree explicitly states that its implementation is compatible with an electronic invoicing mandate which is also underway in Spain. Therefore, taxpayers must ready themselves to comply.

For an overview about other VAT-related requirements in Spain read this comprehensive page about VAT compliance in Spain.

Update: 24 February 2022 by Victor Duarte

The Spanish Ministry of Finance has published a draft resolution that will – once adopted – establish the requirements for software and systems that support the billing processes of businesses and professionals. This law will have a significant impact on the current invoice issuance processes. It will require implementing new invoice content requirements, including a QR code, and the generation of billing records by January 2024.

The regulation is also intended to adapt the Spanish business sector, especially SMEs, micro-enterprises, and the self-employed, to the demands of digitization. For this, it is considered necessary to standardise and modernise the computer programs that support the accounting, billing, and management of businesses and entrepreneurs.

Scope of the regulation

The regulation establishes the requirements that any system must meet to guarantee the integrity, conservation, accessibility, legibility, traceability and inalterability of the billing records without interpolations, omissions or alterations.

The new rules established in the regulation will apply to:

Taxpayers subject to corporate tax (IS), except for exempt or partially exempt entities.

Taxpayers subject to income tax for physical persons (IRPF) who obtain income from economic activities.

Taxpayers subject to income tax for non-residents (IRNR) with a permanent establishment in Spain.

Entities under the income allocation system carrying out economic activities.

Companies that do not fall within the above categories do not need to comply, but those who do must ensure their computer systems are adapted to this regulation as of 1 January 2024.

New invoice content requirements: ID and QR codes

Invoices generated by the computer systems or electronic systems and programs that support the billing processes of businesses and professionals must include an alphanumeric identification code and a QR code, generated per the technical and functional specifications established by the Ministry of Finance.

Billing system requirements

The computer systems that support billing processes must have the capability to:

Generate a billing record for each delivery of goods or provision of services, simultaneously or immediately before the issuance of the invoice.

The computer system must be able to send all the billing records generated to the State Tax Administration Agency (AEAT) in a continuous, secure, correct, complete, automatic, consecutive, instantaneous, and reliable manner.

The system must be provided with traceability, verifying the sequence of data creation. It will create an event log that collects all the system operations and incidents during its use.

The records created may not be altered by the user or any internal or external means.

The systems must add a fingerprint or ‘hash’ to the billing records, according to the specifications and the electronic signature.

To achieve these ends, all computer systems must certify that they ensure the commitment to comply with all the requirements established in this regulation through a “responsible statement”. The Ministry of Finance will establish the minimum content of this statement later in a new resolution.

Billing record content and its optional transmission

The billing records must comply with several content requirements laid down by the regulation.

The taxpayers using computer systems to comply with their invoicing obligations may voluntarily send all its billing records generated by the computer systems to the AEAT automatically by electronic means. The response of a formal acceptance message from the AEAT will automatically mean that these records have been incorporated into the taxpayer’s sales and income ledgers.

Tax administration audits

The AEAT may appear in person where the computer system is located or used and may require full and immediate access to the data record, obtaining, where appropriate, the username, password and any other security key that is necessary for full access.

The AEAT may request a copy of the billing records, which companies may provide in electronic format through physical support or by electronic means.

Application to the B2B e-invoicing mandate

The regulation doesn’t include any specific rule for the B2B e-invoice mandate draft decree currently being discussed in Congress and waiting for approval. However, if the mandate is approved, all the B2B e-invoices issued under this draft decree will have to comply with all the new rules established in this regulation.

Next steps

While this new regulation does not seem to take Spain further down the continuous transaction control (CTC) route, the proposal has clear similarities with Portugal’s invoice requirements.

The draft resolution establishing these is currently open for public consultation until 11 March 2022. Once this resolution is approved, the Ministry of Finance will publish the technical and functional specifications needed to comply with the new requirements and the structure, content, detail, format, design and characteristics of the information that companies must include in the billing records.

The Ministry of Finance will also publish the specifications of the signature policy and the requirements that the fingerprint or ‘hash’ must meet. Once these details are published, it will be clearer whether Spain is going down the Portuguese route or carving out its own path.

Take Action

Need help staying up to date with the latest VAT and compliance updates in Spain that may impact your business? Get in touch with Sovos’ team of experts today.

In 2020, the European Commission (EC) adopted a four-year plan to develop a fairer and simpler taxation framework. The Action Plan aspires to tighten up the tax system, ensure that digital platforms are made to follow transparency rules and utilise data better, reducing tax fraud and evasion.

In 2021, the Commission implemented e-commerce changes – another step in the modernisation process. Beginning in July of 2021, the Mini One Stop Shop (MOSS) system was expanded to the One Stop Shop (OSS) and Import One Stop Shop (IOSS).

The implementation of OSS expanded the use of the union and non-union schemes. This allows European and non-European business-to-consumer sellers of digital services and goods to simplify their reporting practices. Meanwhile, IOSS allows businesses to register and import goods into the EU with a value not exceeding €150.

In 2022, there are plans to release legislation under the “VAT in the digital age” Action Plan. Much like its predecessors in 2020 and 2021, the core purpose of this plan is to tackle the issue of fraud and improve the way businesses engage with the VAT system. The Commission has announced three points it seeks to address in its legislation:

Specifically, one point of interest is the single EU VAT registration point, which aims to facilitate compliance among Member States. With this, the European Commission is requesting feedback on how businesses think the I/OSS implementation has gone and on other potential legislative options for the future, including:

Extension of OSS to:

Cover all B2C supplies of goods and services by non-established suppliers

Enable intra-Community supplies and acquisitions of goods, thereby avoiding VAT registration when transferring own goods cross-border

Include B2B supplies of goods and services while leaving in place the current VAT refund mechanism

Include B2B supplies of goods and services while also introducing a deduction mechanism for OSS

Reverse charge made available for all B2B supplies carried out by non-established suppliers

Removing the €150 threshold for IOSS so that it applies to distance sales of goods of any value

Making IOSS mandatory for:

All distance sales of imported goods

All distance sales of imported goods above an EU turnover threshold (e.g. €10,000)

Marketplaces only

The European Commission began a period of public consultation on 21 January regarding adapting VAT rules in a digital economic landscape. They are seeking feedback on how the EC should adapt VAT tax processes and how they can incorporate technology to solve principal issues in tax, such as fraud and the complexity of its systems. The Commission is accepting feedback in this public consultation period until 15 April 2022 – submissions can be made here.

Sovos will continue to monitor the development of this legislation throughout the year as more information about its structure and impact is released, as these changes are sure to be impactful upon the European VAT landscape.

South Korea has an up-and-running e-invoicing system that combines mandatory e-invoicing with a continuous transaction controls (CTC) reporting obligation. This mature and well-established system, launched over a decade ago, is seeing its first significant changes in years.

Presidential Decree No. 31445 (Decree) has recently amended certain provisions of the Enforcement Decree of the Value-Added Tax Act. Among other changes, the scope of e-invoicing has been expanded and a new timeline and threshold limits introduced. This means that more taxpayers in South Korea must comply with e-invoicing rules in accordance with the timelines.

What is the new timeline and threshold limits for e-invoicing?

In South Korea, e-invoicing has been mandatory for all corporate businesses since 2011. From 2012, individual businesses (entrepreneurs) have also been required to comply with e-invoicing obligations if they meet the threshold limits which have been updated a couple of times over the years. Currently, an individual business whose aggregate supply value (including transactions that are tax exempt) for the immediately preceding tax year is KRW 300,000,000 or more, is required to comply with the country’s e-invoicing rules.

After the recent amendments, the current threshold is now lowered to KRW 200,000,000 and the new threshold limit will be applicable from 1 July 2022. The tax authority has already communicated further adjustments, announcing that from 1 July 2023, the threshold will be reduced further to the limit of KRW 100,000,000. The Korean tax authority aims to enhance the transparency of tax sources by requiring more businesses to comply with the e-invoicing rules.

What´s next for e-invoicing requirements in South Korea?

The expansion of the scope of e-invoicing obligations does not come as a surprise. Like in many other CTC jurisdictions, transactional data collected from a larger number of taxpayers provides greater insight to the tax authority about VAT, market trends and more.

Due to its success and maturity, e-invoicing in South Korea continues to inspire other countries in the Asia Pacific region. The Philippines tax authority is in the process of launching an e-invoicing pilot for the country’s 100 largest taxpayers from 1 July 2022. When designing their e-invoicing system, the Philippines tax authority had several meetings with its South Korean counterparts to benefit from Korean expertise and experience. Therefore, the Philippines is introducing a relatively similar CTC system to the Korean one.

Take Action

Need to ensure compliance with the latest e-invoicing requirements in South Korea? Get in touch with our tax experts. Follow us on LinkedIn and Twitter to keep up-to-date with regulatory news and updates.

The EU-UK Trade and Cooperation Agreement (TCA) provides for tariff-free trade between the United Kingdom (UK) and the European Union (EU) but does not work in the same way as when the UK was part of the EU.

Before Brexit, if the goods were in free circulation within the EU, they could be moved cross-border without incurring any additional customs duty. Therefore, the origin of the goods was not relevant for this intra-EU movement. If the goods originated from outside the EU, customs duty would have been paid as required when they first entered into free circulation but was not payable again.

This difference creates issues for UK businesses where they import finished goods into the UK first before being sold to the EU. As the goods are not being processed in the UK, they cannot be of UK origin and will be subject to double duty unless specific duty mitigations measures are taken.

The same tariff-free trade between the EU and the UK can be achieved under the TCA, but it depends on meeting the detailed rules within the agreement. The key is in the origin of the goods and whether they qualify under the terms of the TCA. This ensures that only eligible goods are tariff-free and removes the risk of goods entering from outside the Free Trade Area without paying customs duty.

The requirement for goods to be of relevant origin to benefit from zero tariffs on imports under the TCA has been in place since 1 January 2021.

Claiming and evidencing relief

If goods meet the appropriate rules of origin, preference can be claimed on the customs declaration when they are imported. Thus, the claim is made by the importer of the goods. However, it is not as simple as completing the appropriate box on the declaration; there is a requirement for the proper evidence to be held.

To claim tariff preference, the importer needs to have one of the following proofs of origin:

A statement on origin – this must be made out by the exporter to confirm the product originates in the UK or EU; or

Importer’s knowledge – this option allows the importer to claim tariff preference based on their knowledge of where the goods they’re importing originate.

If they are relying on a statement of origin, the exporter will have to prove that the goods are of appropriate origin to qualify.

End of easement

In 2021, there was a light touch approach towards holding evidence when the customs declaration was made. The TCA allowed for a declaration to be made and the evidence to be obtained later to reduce the burden on business. There is still a requirement to provide the appropriate evidence on request, so businesses must ensure that it will be available if necessary.

There may be checks that the goods are of appropriate origin to be free of duty under the TCA. With effect from 1 January 2022, there is a need to have the appropriate evidence that the goods meet the origin requirements when the declaration is lodged. Therefore, businesses will need to ensure that the appropriate documents are immediately available should they be requested.

Post import claims for relief

Businesses should note that it is not obligatory to claim preference at the time of entry of the goods as claims can be made up to three years later, as long as there is valid proof of origin. It is beneficial to claim preference at the earliest possible time to benefit cash flow and provide certainty of the cost of the goods.

Therefore, businesses will need to ensure that they determine origin of goods correctly and have the appropriate evidence to support the goods being tariff-free.

It’s important to remember that the rules for trade between Northern Ireland and the EU are different because of the Northern Ireland Protocol.

Take Action

Get in touch with Sovos to discuss your company’s obligations for cross-border trade.

We recently launched the 13th Edition of our annual Trends report, the industry’s most comprehensive study of global VAT mandates and compliance controls. Trends provides a comprehensive look at the world’s regulatory landscape highlighting how governments across the world are enacting complex new policies and controls to close tax gaps and collect the revenue owed. These policies and protocols impact all companies in the countries where they trade no matter where they are headquartered.

This year’s report looks at how large-scale investments in digitization technology in recent years have enabled tax authorities in much of the world to enforce real-time data analysis and always-on enforcement. Driven by new technology and capabilities, governments are now into every aspect of business operations and are ever-present in company data.

Businesses are increasingly having to send what amounts to all their live sales and supply chain data as well as all the content from their accounting systems to tax administrations. This access to finance ledgers creates unprecedented opportunities for tax administrations to triangulate a company’s transaction source data with their accounting treatment and the actual movement of goods and money flows.

The European VAT landscape

After years of Latin America leading with innovation in these legislative areas, Europe is starting to accelerate the digitization of tax reporting. Our Trends report highlights the key developments and regulations that will continue to make an impact in 2022, including:

VAT reporting processes become digital and more frequent – Existing VAT reporting is becoming more granular and more frequent in many EU Member States, with the majority quickly evolving towards real-time controls with or without electronic invoice mandates.

Italy has mandatory e-invoicing via a data exchange platform previously introduced for public procurement messaging.

Since 2017 in Spain, all companies must report inbound and outbound invoices within four days.

In Hungary, suppliers have had to report their sales invoices in real-time since 2018.

Public procurement standards will play a major role in the design of various continuous transaction control (CTC) models – Frameworks such as PEPPOL are increasingly adopted by public administrations as large buyers of goods and services – the standards and platforms used for these transactions will increasingly be repurposed for electronic invoicing as a key enabler of VAT digitization.

“Own the Transaction” CTC model becomes more popular – More tax administrations aim not only to receive reporting data from business transactions but use legislation to become the invoice exchange platform themselves.

This trend is gaining traction after Turkey and Italy introduced it as core concepts in their CTC legislation, while countries like France and Poland are introducing similar models.

SAF-T is here to stay – The OECD’s Standard Audit File for Tax (SAF-T) will remain an inspiration for European tax administrations not only to enforce VAT via real-time or near-real-time controls, but to obtain copies of taxpayers’ entire accounting books on their own systems for broader tax controls and audit support as well.

EU E-commerce VAT package and digital services – Changes introduced in July 2021 to the One Stop Shop (OSS) and the launch of an Import One Stop Shop (IOSS) concept have drastically changed requirements for all e-commerce vendors and marketplaces selling low-value goods or digital services to European consumers.

According to Christiaan van der Valk, lead author of Trends, governments already have all the evidence and capabilities they need to drive aggressive programs toward real-time oversight and enforcement. These programs exist in most of South and Central America and are rapidly spreading across countries in Europe such as France, Germany and Belgium as well as Asia and parts of Africa. Governments are moving quickly to enforce these standards and failure to comply can lead to business disruptions and even stoppages.

This new level of imposed transparency is forcing businesses to adapt how they track and implement e-invoicing and data mandate changes all over the world. To remain compliant, companies need a continuous and systematic approach to requirement monitoring.

Trends is the most comprehensive report of its kind. It provides an objective view of the VAT landscape with unbiased analysis from our team of tax and regulatory experts. The pace of change for tax and regulation continues to accelerate and this report will help you prepare.

Take Action

Contact us or download Trends to keep up with the changing regulatory landscape for VAT.

Towards the end of 2021, the tax authority in Turkey published a draft communique that expands the scope of e-documents in Turkey. After minor revisions, the draft communique was enacted and published in the Official Gazette on 22 January 2022.

Let’s take a closer look at the changes in the scope of Turkish e-documents.

Scope of e-fatura expanded

The gross sales revenue threshold will decreased reduce. The threshold limit has been lowered from TRY 5 million to TRY 4 million and above for the 2021 financial period. A lower threshold of TRY 3 million and above will apply for 2022 and subsequent fiscal periods.

The use of the e-fatura is now mandatory for taxpayers in the e-commerce sector when exceeding a certain threshold. The communique introduced a gross sales revenue threshold of TRY 1 million and above for 2020 and 2021 financial periods; and TRY 500.000 for 2022 and all subsequent fiscal periods.

Taxpayers who run a business in the real estate and/or motor vehicle sector by carrying out construction, manufacturing, purchase, sale, and rental transactions, as well as taxpayers who act as intermediaries in these transactions must use the e-fatura application if their gross sales revenue exceeds TRY 1 million and above for 2020 and 2021 financial periods; and TRY 500.000 for 2022 and all subsequent fiscal periods.

Taxpayers who provide accommodation services by obtaining investment and/or operation certificates from the Ministry of Culture and Tourism and Municipalities must use the e-fatura application.

Taxpayers meeting these thresholds and criteria must start using the e-fatura application from the start of the year’s seventh month following the relevant accounting period.

In terms of accommodation service providers, if they provide services as of the publication date of this communique, they must start using the e-fatura application from 1 July 2022.

For any business activities that start after the publication date of the communique e-fatura must be used from the beginning of the fourth month following the month in which their business activities began.

E-arsiv invoice scope expanded

Taxpayers not in scope of e-arşiv invoices have been obliged to issue e-arşiv invoices if the total amount of the invoices to be issued exceeds TRY 30.000 including taxes (in terms of invoices issued to non-registered taxpayers, the total amount including taxes exceeds TRY 5.000) from 1 January 2020.

With the amended communique, the Turkish Revenue Administration (TRA) lowered the total amount of the invoice threshold to TRY 5.000, and thus more taxpayers will be required to use the e-arsiv application. The new e-arsiv invoice threshold applies from 1 March 2022.

E-delivery note scope expanded

Another change introduced by the communique was the expansion of the scope of e-delivery notes. The gross sales turnover threshold for mandatory e-delivery notes has been revised to TRY 10 million, effective from the 2021 accounting period. In addition, taxpayers who manufacture, import or export iron and steel (GTIP 72) and iron or steel goods (GTIP 73) are required to use the e-delivery note application. E-fatura application registration is not applicable to those taxpayers.

The EU E-Commerce VAT Package came into effect on 1 July 2021. And with it, the need for operational change, business disruption and plenty of accounting complexity.

A key component of the package is the Import One Stop Shop (IOSS) – a new way for companies to meet their EU VAT obligations when trading cross-border.

In this e-book we explain IOSS’s key concepts and common use cases so you can better understand and take advantage of IOSS and how you apply it to your business.

IOSS is expansive, complicated and rewrites the rules for companies selling into and within Europe. This e-book aims to simplify that for you. We cover:

The basics

Intermediary requirements

Key considerations for your business

How to ensure IOSS compliance

How we can help

Get the e-book

We spend ample time on each of these topics so that you feel confident understanding whether IOSS is the right option for your business.

Our e-book starts with an easy-to-understand primer on IOSS. This includes how IOSS operates, its many rules and what has happened. The e-book also explains more on IOSS intermediaries as well as their purpose and when they can be used.

Find out more about the IOSS registration process, including its effects on:

Customer experience

VAT registration

VAT simplification

Record keeping

Data collection and invoicing

Contingency planning

Commercial matters

We answer some important questions you should consider about IOSS registration:

Will you need to appoint an intermediary?

How will you appoint one?

How will you get set up for IOSS registration – will you do this yourself or search for help?

How will you submit monthly returns and pay the VAT or use a partner?

How can you ensure record keeping data is in the right format and up to date?

How will you respond to tax authority audits?

Whatever your eventual IOSS decision is, our e-book will help you make an informed decision for the good of your business.

Whatever your VAT implications, Sovos has the expertise to help you navigate your global events and the complexities of cross-border VAT obligations.

Our VAT Managed Services ease your compliance workload while mitigating risk wherever you operate today. In addition, we ensure you’re ready to handle the VAT requirements in the markets you intend to lead tomorrow.

The Tax Bureaus of Shanghai, Guangdong Province and Inner Mongolia Autonomous Region have all issued announcements stating they intend to carry out a new pilot program for selected taxpayers based in some areas of the provinces. The pilot program will involve adopting a new e-invoice type, known as a fully digitized e-invoice.

Introduction of a new e-invoice type

Many regions in China are currently part of a pilot program that enables newly registered taxpayers operating in China to voluntarily issue VAT special electronic invoices to claim input VAT, mostly for B2B purposes.

The new fully digitized e-invoice is a simplified and upgraded version of current electronic invoices in China. The issuance and characteristics of the fully digitized invoice are different from other e-invoices previously used in the country.

Characteristics of the fully digitized e-invoice

The fully digitized invoice is supervised by the local Taxation Bureaus as part of the pilot program

The legal effect and basic purpose are the same as those of existing paper invoices

Fully digitized invoices can be delivered in the form of data messages, which eliminates specific format requirements such as PDF or OFD

The basic content includes dynamic QR code, invoice number, invoice date, buyer information, seller information, quantity, unit price, amount, tax rate, tax amount, total, total price, and tax

After the pilot program taxpayer has passed a “real-name verification” they can immediately use the electronic invoice service platform to issue invoices without the need to use special equipment for tax control (e.g., UKey device)

Pilot taxpayers can automatically deliver fully digitized invoices through the tax digital account of the electronic invoice service platform and can also deliver fully electronic invoices themselves via email or other means

Verification of fully digitized e-invoices

Relying on the national unified electronic invoice service platform, tax authorities will provide selected taxpayers for this pilot program with services such as issuance, delivery, and inspection of fully digitized e-invoices 24 hours a day. Taxpayers will be able to verify the information of all electronic invoices through the electronic invoice service platform or the national VAT invoice inspection platform.

What’s next for e-invoicing in China?

This new pilot program has been effective in Shanghai, Guangzhou, Foshan, Guangdong-Macao Intensive Cooperation Zone, and Hohhot since 1 December 2021. Despite the lack of an official timeline for implementation, it’s expected that the scope of this pilot program will be extended in 2022 to cover new taxpayers and regions in China, paving the way for nationwide adoption of the fully digitized e-invoice.

As a result of the 2020 Finance Law implementation, which transfers the management and collection of import VAT from customs to the Public Finances Directorate General (DGFIP), France has implemented mandatory reporting of import VAT in the VAT return instead of having the option to pay through customs as is typically the process. This change came into effect on 1 January 2022, with additional VAT reporting changes in France, including the Declaration of Exchange Goods (DEB) split where the Intrastat dispatch and EC sales list are now separate reports.

This new import procedure is mandatory for all taxpayers identified for VAT purposes in France. Registered taxpayers may no longer opt to pay import VAT to customs and must report all import VAT via the VAT return. This is a departure from the prior process, where taxpayers needed to receive prior authorisation to implement a reverse charge mechanism to pay import VAT through the VAT return. Now, this process is automatic and mandatory, and no authorisation is required.

Consequently, taxpayers with import transactions into France must now register for VAT purposes with the French tax authorities. Additionally, the French intra-community VAT number of the person liable for payment of import VAT must be listed on all customs declarations.

Changes to the VAT return

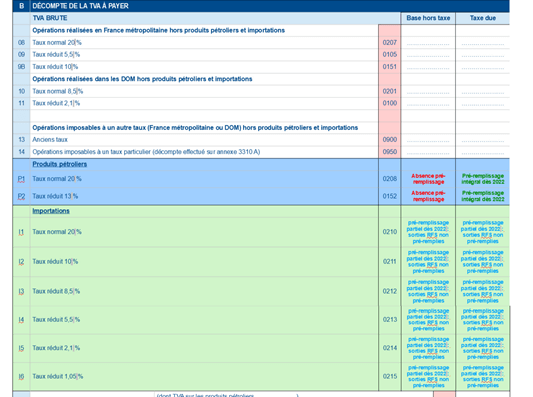

Changes to the French VAT return include (see Figure 1):

New fields to report import VAT and petroleum products

New numbering system for most of the return

Pre-filled information on imports – lists the amount of import VAT collected from customs items previously declared to the Directorate-General of Customs and Indirect Taxes (DGDDI). Taxpayers will have the ability to edit the pre-filled import amounts before submission

Pre-filled information will be populated from the 14th of the month following the due date

VAT returns containing import VAT will be due the 24th day of the month following the filing period

Figure 1: Draft extract of 2022 FR VAT Return

Impact on Taxpayers

From 31 December 2021, “foreign traders” who imported goods and then made local sales under the domestic reverse charge are now required to register as a result of the import portion of the transaction and will still apply the reverse charge to their sales. This will now require a new VAT declaration to be submitted.

Additionally, until 31 December 2021, a foreign company that imported goods into France and made local sales under the reverse charge had to recover the import VAT paid under the Refund Directive (EU companies) or the 13th Directive (non-EU companies). For Refund Directive claims, there would have been a cash advantage for France because either companies did not submit claims (small value) or because claims were rejected for non-compliance. For claims under the 13th Directive and the two previous considerations, there was also the issue of “reciprocity” which prevented claims from some counties such as the US, for example. Under the new regime, all import VAT is reclaimed, leading to a potential budget shortfall.

Take Action

To find out more about what we believe the future holds, download Trends and follow us on LinkedIn and Twitter to keep up-to-date with the latest regulatory news and updates.

With the most significant VAT gap in the EU (34.9% in 2019), Romania has been moving towards introducing a continuous transaction control (CTC) regime to improve and strengthen VAT collection while combating tax evasion.

The main features of this new e-invoicing system, e-Factura, have been described in an earlier blog post. Today, we’ll take a closer look at the roll-out for B2B transactions and the definition of high-fiscal risk products, as well as the new e-transport system that was introduced through the Government Emergency Ordinance (GEO) no. 130/2021, published in the Official Gazette on 18 December.

According to GEO no. 120/2021 (the legislative act introducing the legal framework of e-Factura), the supplier and the recipient must both be registered with the e-Factura system. The recently published GEO no. 130/2021 establishes an exception for high fiscal risk products and ensures that taxpayers will use the e-Factura system regardless of whether the recipients are registered.

In line with the GEO no. 130/2021, the National Agency for Fiscal Administration has issued an order to clarify which products are considered high fiscal risk products.

The five product categories are as follows:

Vegetables, fruits, roots and edible tubers, other edible plants

Alcoholic beverages

New constructions

Mineral products (natural mineral water, sand and gravel)

Clothing and footwear

High fiscal risk products are defined based on the nature of the products, marketing method, traceability of potential tax evasion and degree of taxation in those sectors. Detailed explanations, as well as product codes, can be found in the Annex of GEO no. 130/2021.

The enforcement timeline of this requirement means that businesses that supply these types of products must be ready to comply with the new Romanian e-Factura system as follows:

From 1 April to 30 June 2022: It will be voluntary to submit invoices in the Romanian e-Factura system

From 1 July: It will be mandatory to submit invoices in the Romanian e-Factura system

Looking ahead: introduction of an e-transport system in Romania

Another reform that shows the intention of the Romanian authorities to combat tax fraud and evasion is the introduction of an e-transport system.

Taxpayers will be required to declare the movement of goods from one location to another in advance. Once declared, the system will issue a unique number written on the transport documents. Authorities will then verify the declaration on the transport routes.

Moreover, it is stated in the justification letter that the e-transport system will interconnect with the Ministry of Finance’s current systems, Romanian e-invoice, and traffic control, much like similar initiatives in other countries, such as India, Turkey and Brazil.

The introduction of the e-transport system is still pending as the Ministry of Finance has not yet issued the order regarding the application procedure of the system. According to GEO 130/2021, the Ministry of Finance had 30 days to do so after GEO 130/2021 was published in the Official Gazette. However, the deadline expired on the 17 January, and no announcement has been made yet. Therefore, the details of the system are still unknown.

Take Action

Need to ensure compliance with the latest Romanian regulatory requirements? Speak to our team. Follow us on LinkedIn and Twitter to keep up-to-date with the latest regulatory news and updates.

The Northern Ireland Protocol regarding goods moving from Great Britain to Northern Ireland continues to cause problems, leading to calls to suspend it via Article 16. But at the same time, some NI politicians are looking to capitalise on the possibility of inward investment by companies that can benefit from being in both the UK and the Single Market at the same time. This will be an interesting circle to square.

For goods moving from Great Britain to the EU, it has been necessary to review supply chains and VAT compliance, especially where the GB supplier is required to import the goods. Here we have the issue of theory clashing with reality, requiring plans to be revised.

Many UK suppliers selling goods into the EU decided that a good approach would be to obtain a VAT number in the Netherlands and then import the goods under an Article 23 licence to defer the import VAT to the VAT return – a straight-forward scheme to set up and manage. However, under the Union Customs Code, anyone who imports goods into the EU is required either to be established in the EU or to appoint an “indirect customs agent” who is established in the EU.

Upon accepting such an appointment, the EU entity becomes jointly liable with the importer for the VAT and duty that is due. Not surprisingly, it is difficult to find businesses that will offer such a service. In 2020, the body representing freight forwarders in Germany suggested that no such appointments should be accepted because of the financial risk. For many UK businesses, the only solution has been to establish a company in the EU, often the Netherlands, to import in their name.

Brexit also caused issues for GB businesses that supply equipment required to be installed in factories or other premises – such as parts of manufacturing production lines.

Within the Single Market there is a simplification for such supplies. The vendor can move the goods to another Member State to install them with the customer accounting for the acquisition tax due on the goods. This is because there is no need for the supplier to have a local VAT number in the Member State where the goods are installed.

Following Brexit, suppliers shipping goods from Great Britain to the EU for installation are no longer able to use this simplification. Instead, the GB supplier must now import the goods into the EU and then make a sale. If the goods are imported and installed in a Member State where the extended reverse charge applies to the sale, there will be a cash flow issue regarding the paid import VAT. Claims need to be made under the 13th Directive and, if the Member State concerned applies the concept of “reciprocity”, then the claim may be denied.

“Reciprocity” allows a Member State to refuse VAT refunds to taxpayers from third countries which do not allow VAT refunds to taxpayers of the Member State. The Member State normally publishes a list of third countries that can submit claims where reciprocity is invoked.

Pre Brexit, there was no need for the UK to be on such a list, so this now represents a real risk. Some Member States, including Spain, added the UK to their list immediately following Brexit. If these subtle complexities are not considered before a transaction is agreed the cashflow consequences could be severe – so planning is essential.

Businesses also have to ensure that they are prepared for changes which came into effect on 1 January 2022.

Under the EU-UK Trade and Cooperation Agreement, goods exported from Great Britain to the EU with a UK origin are free of import duty. In some situations, exporters require information from their suppliers about the origin of the goods they are supplying.

Until 31 December 2021, an exporter of goods from Great Britain to the EU did not need to hold a supplier’s declaration when making a statement on origin to be used by the customer to claim the zero-duty rate on imports into the EU. It is enough that the exporter is confident that the origin rules are met and make every effort to get supplier declarations retrospectively.

Suppose a UK exporter finds that a supplier statement is not available retrospectively. In that case, they must inform the EU customer who will have to consider the impact on the imports they have made.

If an exporter cannot comply with an official request for verification of the origin of the goods being the UK, the EU customer will be liable to pay the full duty rate retrospectively.

From 1 January 2022, an exporter must hold a supplier’s declaration, when required, when making the statement on origin declaration to the customer or the full rate of Customs Duty is payable. This significant change to the rules will impact all businesses exporting to the EU, including e-commerce retailers selling goods above EUR150.

Take Action

Get in touch about the benefits a managed service provider can offer to ease your business’ VAT compliance burden.

In a blog post earlier this year, we wrote about how several Eastern European countries have started implementing continuous transaction controls (CTC) to combat tax fraud and reduce the VAT gap. However, it’s been an eventful year with many new developments in the region, so let’s take a closer look at some of the changes on the horizon.

Latvia

Latvia has recently revealed its new CTC regime plans. The Latvian government approved a report prepared by the Ministry of Finance to implement an electronic invoicing system in the country. The concept described in the report envisages the introduction of electronic invoicing as mandatory for B2B and B2G transactions from 2025 under the PEPPOL framework. The details about the system, including the legislation and technical documentation, are expected in due course.

Serbia

Serbia is another country moving rapidly towards a CTC framework, and apparently, various stakeholders find this movement rather quick. The Ministry of Finance recently announced that upon the request for a transition period to adapt to the new system of e-invoices, they have decided to postpone the date for entry into force of CTC clearance for B2G transactions until the end of April 2022. It must be noted that there has been no delay concerning B2B transactions.

According to the revised calendar:

From 1 May 2022: B2G e-invoicing through a CTC portal will become mandatory

From 1 July 2022: All taxpayers will be obliged to receive and store e-invoices

From 1 January 2023: All taxpayers will be obliged to issue B2B e-invoices through the CTC system.

Slovenia

Slovenia is also looking to introduce CTCs. In June 2021, the Ministry of Finance submitted a draft law to the Slovenian parliament, aimed at introducing mandatory B2B e-invoicing in the country. According to the draft regulation, all business entities would be obliged to exchange e-invoices exclusively in their mutual transactions (B2B). In the case of B2C transactions, consumers could opt to receive their invoices in electronic or paper form. However, the Ministry of Finance withdrew the draft law due to disagreement with various stakeholders but intends to review it by simplifying the process and reducing the administrative burden on businesses.

Discussions around the introduction of CTCs in the country continue among various stakeholders, e.g., the local Chamber of Commerce. However, seeing as national elections are expected in Slovenia in April 2022, the CTC reform is not expected to gain much traction until summer 2022 at the earliest.

Slovakia

Earlier this year, we reported that the Slovakian Ministry of Finance had prepared draft legislation to introduce a CTC scheme. The aim was to lower Slovakia’s VAT gap to the EU average and obtain real-time information about underlying business transactions. Public consultation for the draft law was completed in March 2021. However, no roll-out timeline was published at the time.

Over the past months, the Slovakian government has launched the CTC system and published new documentation. The CTC system is called Electronic Invoice Information Systems (IS EFA, Informačný systém elektronickej fakturácie) and is a unified process of electronic circulation of invoices and sending structured data from invoices to the financial administration. The timeline for the gradual roll-out of entry into force looks as follows:

Phase 1: From January 2022, CTC e-invoicing will be introduced for B2G, G2G, and G2B transactions; and

Phase 2: From January 2023, CTC e-invoicing will be introduced for B2B, B2C, and G2C transactions.

Poland

There have been serious developments regarding Poland’s CTC framework and system, the Krajowy System e-Faktur (KSeF). The CTC legislation was finally adopted and publishedin the Official Gazette on 18 November 2021. Starting from January 2022, KSeF goes live as a voluntary system, meaning there is no obligation to use this e-invoicing system in B2B transactions. It is expected that the system will be mandatory in 2023, but no date has been set yet for the mandate.

With the largest VAT gap in the EU (34.9% in 2019), Romania has also been moving towards introducing a CTC regime to streamline the collection of taxes to improve and strengthen VAT collection while combating tax evasion. In October 2021, Government Emergency Ordinance (GEO) no. 120/2021 introduced the legal framework for implementing e-Factura, regulating the structure of the Romanian e-invoice process and creating the framework for basic technical specifications of the CTC e-invoicing system. While the Romanian e-Factura went live as a voluntary system on 6 November 2021, no timeline has yet been published for a mandate. Suppliers in both B2B and B2G transactions may opt to use this new e-invoicing system and issue their e-invoices in the Romanian structured format through the new system.

The EU e-commerce VAT package was introduced in July 2021. The new schemes, One Stop Shop (OSS) and Import One Stop Shop (IOSS) bring significant changes to VAT treatment and reporting mechanisms for sales to private individuals in the EU.

In the last of our series of FAQ blogs, we answer some of the more common questions asked on the IOSS.

IOSS VAT is the VAT collected at the time when the supply takes place and subsequently remitted to the tax authority in the Member State of Identification (MSI).

Under the old rules, when goods imported from third countries were sold to private individuals, the normal steps would require the supplier to account for import VAT, then account for the VAT on the subsequent supply (the sale to the private individual) then deduct the import VAT.

Instead, with IOSS, the VAT on the import is exempt and only the VAT on the subsequent supply is to be collected and remitted to the tax authority.

Q: What is IOSS?

IOSS is short for Import One Stop Shop. This is a special scheme that simplifies the registration obligations for taxpayers who carry out distance sales of goods imported from third countries to private individuals in the EU.

Similar to the OSS, the IOSS scheme allows taxpayers to register in a single EU Member State where they account for VAT that was actually due in other Member States.

Here’s an example. A business registered for IOSS in the Netherlands, can account for its sales to German, French, Italian, Polish etc. customers in its Dutch IOSS return thus avoiding the requirement to register in multiple jurisdictions.

Other advantages of using the schemes are:

Making use of the exemption from import VAT.

No customs duties are due at importation.

The scheme, however, is restricted to consignments of up to €150. Additionally, signing up for the scheme requires careful analysis of the taxpayer’s profile, the way the supply chain is structured and other factors. All of these would affect the business’ eligibility for the scheme, and the requirements to appoint a special type of representative for the purposes of the scheme that is required in certain cases.

If such representative is required, they will be jointly and severally liable with the taxpayer’s IOSS obligations. It’s also important to note that such representative must be established in the EU.

Q: What is an IOSS number?

An IOSS number is the specific identification for the IOSS scheme that is designated by the MSI (the country where the taxpayer is eligible or decides to register for the scheme) to the taxpayers that have decided to make use of this mechanism.

Although IOSS identification is a type of VAT identification it’s not an actual resident VAT registration in the MSI.

Instead, it’s an IOSS number specifically for the purposes of the scheme. In this sense only the eligible type of supplies can be accounted for using the IOSS number and the IOSS registration. In case the taxpayer will carry out other type of supplies which require a regular VAT registration the latter should be obtained for the purposes of being compliant.

Q: How much does IOSS cost?

The cost of IOSS compliance can vary depending on multiple factors. This would be ultimately affected by:

The scope and the quality of the service offered by different providers. For example, a low-cost provider would have the best price, but it will not offer the full scope of compliance service in terms of detailed data checks, instant client communication, providing compliance or ad hoc advisory services. On the other hand, mid-market providers would be best suited to provide a balanced price that would have the added value of more coherent, consistent and higher quality service.

The requirement to appoint an IOSS representative that is established in the EU. For example, should a taxpayer need to appoint such representative, the cost would be higher as the latter would be jointly and severally liable regarding the taxpayer’s IOSS obligations.

Q: Who needs an IOSS number?

An IOSS number is required for any taxpayer that wants to make use of the IOSS special scheme. This mechanism isn’t mandatory hence there’s no obligation to apply for an IOSS number.

However, it is advisable that any taxpayer that carries out supplies eligible to be reported using IOSS should consider this option as it has some considerable advantages. Of course, the consideration should also include the numerous requirements and conditions that must be met if a person opts to use the IOSS scheme.

Q: What’s the difference between IOSS and OSS?

Both are special schemes used to simplify the registration obligations for taxpayers involved in B2C supplies. They provide an option to account for VAT, that is due in multiple EU VAT jurisdictions, using a single registration and only one IOSS or OSS return.

The difference between both schemes is the different types of supplies that can be accounted for. More precisely:

IOSS can only be used to account for B2C distance sale of goods imported from third countries, whereby the eligible supplies are restricted to a single consignment value of up to 150 EUR.

OSS can be used to account for B2C intra-Community distance sale of goods irrespective of the consignment value.

Considering the above, the main difference is that with IOSS the goods are located in a third country (outside the EU customs territory) at the time of the sale, whereas with OSS the goods are located within the EU’s territory.

Q: Do I need to register for IOSS?

No, IOSS is currently an optional scheme for taxpayers. If not used, the taxpayer’s supplies are subject to the normal rules and depending on the way the supply is structured normal VAT registration/s may be required instead.

Q: What is IOSS tax ID?

IOSS tax ID is the special IOSS VAT number assigned to a taxpayer that has chosen to opt in for the IOSS scheme. It‘s not a regular VAT number that is assigned in the course of a normal VAT registration but is instead used to identify a taxpayer specifically for the purposes of the scheme.

Also, in more practical terms, the IOSS number must be indicated in a specific way on each shipment/supply in order to identify it as eligible under the IOSS as this would allow for:

1Quicker customs procedures

Exemption of the import VAT

No customs duties will be charged

The VAT on the supply to be accounted for under the monthly IOSS VAT return of the taxpayer

The EU e-Commerce VAT Package is nearly six months old and businesses should have submitted their first Union One Stop Shop (OSS) return by the end of October 2021. Union OSS provides a welcome simplification to the requirement to be registered for VAT in multiple Member States when making intra-EU B2C supplies of goods and services.

Whilst a simplification, there are several conditions that need to be met on an ongoing basis to continues its use. The European Commission produced a number of guides on the application of Union OSS prior to its introduction which provided guidance on its operation. However, there are still several questions about how Union OSS interacts with other compliance obligations in place for e-commerce sellers around the EU.

Union OSS – interaction with Intrastat

Intrastat is the EU’s mechanism to provide details of intra-EU trade in the absence of customs borders. It’s made up of two components: dispatches declarations submitted in the Member State where the transport starts and arrivals declarations in the Member State of delivery.

E-commerce businesses selling intra-EU goods have long had to comply with Intrastat obligations when they exceeded the reporting thresholds. For lots of businesses an obligation arose in the Member State from where the goods are dispatched given that goods were delivered to multiple other EU countries, so thresholds were often exceeded.

In addition, larger e-commerce sellers also had obligations to submit arrivals declarations in the country of delivery of the goods even though they were not the purchaser of the goods. The very largest may also have had obligations to submit dispatches declarations in the Member State of their customer because of returned goods.

There is no mention of Intrastat in any of the European Commission’s guides about OSS so no guidance is provided on how it will apply when a business adopts Union OSS. Furthermore, many Member States do not currently seem to have a finalised position on the interaction with Union OSS.

The position in the Member State of dispatch of the goods seems clear but there are potentially complexities when goods are dispatched from more than one Member State especially if there is no VAT registration in that country. Whilst this is unlikely, there are circumstances where no VAT registration is required or even allowed.

The real complexity is with regards to Intrastat arrivals declarations. The principle of Union OSS is that no VAT registration is required in the Member State of the customer for intra-EU supplies. There may be other reasons for a VAT registration there but for many e-commerce sellers, they will not have to be registered in the Member State of delivery.

This raises the question of whether arrivals declarations are required in those territories. Some Intrastat authorities have provided guidance and those that have are taking different routes. Some are clear it is not required for arrivals when using Union OSS whilst others still require declarations to be made even though there is no local VAT registration in place.

We continue to monitor the situation and will update further as more information is available.

Unions OSS and other declarations

E-commerce sellers of goods can have other compliance and tax obligations in the countries to which they deliver goods. These include meeting local country rules with regards to environmental taxes. For example in Romania there is a requirement for e-commerce sellers to submit Environmental Fund returns even if the business has opted to use Union OSS. This creates complexity as the Romanian VAT number is normally used to file the returns. A separate registration seems to be possible to ensure compliance with the environmental regulations.

There is also potentially an issue in Hungary with the retail tax that is payable by businesses with a turnover in excess of HUF 500 million. There is still a liability to pay the tax even if there is no VAT registration because of Union OSS. Affected businesses will need to ensure that they remain compliant.

Teething problems can be expected with any new regime but there is an argument that some of these should have been predicted and clear guidance provided, especially for Intrastat. It is clear that some authorities have not considered the matter at all prior to Union OSS’s introduction. We will continue to monitor the situation and provide further updates when more information is available.

Take Action

Get in touch to discuss your Union OSS queries with our tax experts and follow us on LinkedIn and Twitter to keep up-to-date with regulatory news and updates.

As we inch closer to the implementation date of 1 January 2022 for Norway’s new digitized VAT return, let’s take a second look at the details.

Norway announced its intentions to introduce a new digital VAT return in late 2020, with an intended launch date of 1 January 2022. With this update comes the removal of box numbers, which will be replaced by a dynamic list of specifications. The report will also repurpose the Norwegian Standard Tax Codes from the SAF-T financial file to provide more detailed reporting and flexibility. It’s important to note that the obligation to submit a SAF-T file will not change with the introduction of this new VAT return.

This change is for the VAT return only – with the SAF-T codes being re-used and re-purposed to provide additional information. Businesses must still comply with the Norwegian SAF-T mandate where applicable and must also submit this new digital VAT return. With the new VAT return, the Norwegian Tax Administration (Skatteetaten) seeks to simplify reporting, better administration, and improved compliance.

Details on technical specifications

Skatteetaten has created many different web pages with detailed information for businesses to look through over the next few months, including the following:

Implementation guide – created to assist developers and businesses in assessing the technical requirements needed to implement upcoming changes

Validation rules – continually updated as Norway will add more validation rules as needed

XSD for VAT Return – contains the technical specifications (XSD) for the new VAT return as well as example files and descriptions of the fields contained in the return

API submission – contains information on submission and validation of the VAT return, including error messages

Questions and answers – FAQ page for businesses to understand answers to common questions that may come up, including registration, submission method and additional files

Submission method

Norway is encouraging direct ERP submission of the VAT return where possible. However, the tax authorities have announced that manual population via the portal will still be available.

Login and authentication of the end user or system is carried out via the ID porten system. Originally, Norway didn’t allow for XML upload; however, the tax authorities have recently updated their guidance to ensure that XML upload will be accepted. Changing numbers or notes in the uploaded XML file will not be possible, but it will be possible to upload attachments.

Additionally, Norway has provided a method for validation for the VAT return file, which should be tested before submission to increase the probability that the file is accepted by the tax authorities. The validator will validate the content of a tax return and should return a response with any errors, deviations, or warnings. This is done by checking the message format and the composition of the elements in the VAT return.

Please note that Norway is not allowing for any grace period for the submission of this newly designed return.

What’s next?

In addition to the new VAT return, Norway has also announced plans to implement a sales and purchase report by 2024. The proposal is currently in the mandatory public consultation phase, which ends on 26 November 2021.

Romania Issues Last-Minute Amendments to B2B E-invoicing Regulations

After the implementation of Romania’s new B2B e-invoicing regulations, effective January 2024, the country introduced Government Emergency Order No. 115/2023 with last-minute amendments.

We can summarise the key amendments from the new legislation in three categories:

1. Exemptions from the e-reporting and e-invoicing mandate are clarified

The e-reporting mandate explicitly excludes the following transactions:

Intra-community supplies and exports

Supplies of goods or services made to taxable entities not registered or established in Romania

Simplified invoices issued for supplies of goods or services

Provisions of services for which the invoice is not subject to invoicing rules applicable in Romania

2. New five-calendar-day deadline to report e-invoices from July 2024

From July 2024 onwards, the requirement to issue e-invoices for transactions between established entities persists. The amendment states that in the event of a taxpayer’s failure to generate an electronic invoice, they are obligated to submit it to the RO e-Factura platform within five calendar days.

3. Penalties for businesses in the scope of e-invoicing

From July 2024, established entities that fail to comply with the issuance and receipt of e-invoices will receive a fine equal to 15% of the total invoice amount.

Additionally, those who fail to report the invoice which was not issued and automatically transmitted to the RO e-Factura within the additional five calendar days will be fined:

RON 5,000 (€1k) to RON 10,000 (€2k) for legal entities classified as large taxpayers

RON 2,500 (€500) to RON 5,000 (€1k) for legal entities classified as medium taxpayers

RON 1,000 (€200) to RON 2,500 (€500) for other legal entities and individuals

Romania Publishes Draft Legislation For B2B E-invoicing Mandate

The Romanian Ministry of Finance has published draft legislation proposing new budgetary measures, among which is the implementation of the highly anticipated electronic invoicing mandate.

Even though the draft legislation maintains the January 2024 roll-out date previously approved by the EU Council, it proposes an invoice reporting system to operate in the first six months with the electronic invoicing system (RO e-factura) being fully implemented in July 2024.

Additionally, a three-month grace period – from January 2024 to March 2024 – is foreseen where penalties are not imposed.

January 2024 – Established taxable persons, as well as VAT-registered taxable persons, must submit their invoices in the RO e-factura system within five days of issuance for the purpose of reporting the invoice data

April 2024 – Fines will become applicable to non-compliant taxpayers

July 2024 – The system shifts to an invoice clearance system which also transmits the invoice to Romanian-registered trading parties

The first phase of implementation where taxpayers report invoices to the RO e-factura system – instead of issuing the invoices directly through that system – is an addition of the draft law.

This reporting obligation is a transitional measure to help businesses prepare and adapt their systems to the new e-invoicing requirements. Between January and June 2024, the draft legislation also foresees an obligation for the supplier to send the cleared invoice out-of-band to the buyer whenever the latter is not registered with the RO e-factura system.

The scope of the new B2B draft mandate applies to all B2B transactions carried out by established or VAT-registered suppliers deemed to take place in Romania.

Looking to better understand e-invoicing regulations ahead of Romania’s mandate? Our guide can help.

Update: 28 July 2023 by Enis Gencer

Romania Authorised to Implement Mandatory B2B E-Invoicing

The EU Council has approved the proposal from the EU Commission to authorise Romania to introduce mandatory e-invoicing starting from January 2024. The decision was adopted on 25 July and published in the Official Journal of the EU on 27 July.

Romania’s e-invoicing journey

Romania has been progressing towards implementing a continuous transaction controls (CTC) e-invoicing regime for some time now. The country introduced the e-invoicing requirement for B2B transactions of high-fiscal risk products in December 2021 and B2G transactions in May 2022, both implemented as of July 2022.

In addition to these requirements, Romania aims to make e-invoicing mandatory for all B2B transactions. To this end, the country applied to the European Commission on 14 January 2022, requesting authorisation for a special measure to derogate from articles 218 and 232 of Directive 2006/112/EC, which was granted on 25 July. This measure would allow for the introduction of mandatory electronic invoicing for all transactions carried out between taxable persons established in Romania.

Key takeaways from the derogation decision

The derogation will be effective from 1 January 2024. This means that Romania can enforce mandatory e-invoicing for all B2B transactions starting from January 2024, following the amendments in the local legislation.

The derogation will remain valid until 31 December 2026, or until the national transposition of the VAT in the Digital Age (ViDA) directive into Romanian law.

The introduction of mandatory e-invoicing will replace the current obligation to report information on domestic supplies.

What’s next?

The Romanian authorities will need to make the necessary amendments to local legislation to implement mandatory e-invoicing, following the derogation decision received by the EU Council.

The Romanian tax authority, ANAF, is expected to issue an order within 30 days from the date of the derogation which will define the scope and timeline for the implementation of the mandate. The order will provide more specific details about the upcoming mandate.

Considering the mandate could come into effect as early as January 2024, it’s crucial that taxpayers start preparing their systems for mandatory e-invoicing from now.

Looking for guidance to comply with Romania’s upcoming e-invoicing mandate? Our expert team can help.

Update: 28 July 2023 by Enis Gencer

Romania Authorised to Implement Mandatory B2B E-Invoicing

The EU Council has approved the proposal from the EU Commission to authorise Romania to introduce mandatory e-invoicing starting from January 2024. The decision was adopted on 25 July and published in the Official Journal of the EU on 27 July.

Romania’s e-invoicing journey

Romania has been progressing towards implementing a continuous transaction controls (CTC) e-invoicing regime for some time now. The country introduced the e-invoicing requirement for B2B transactions of high-fiscal risk products in December 2021 and B2G transactions in May 2022, both implemented as of July 2022.

In addition to these requirements, Romania aims to make e-invoicing mandatory for all B2B transactions. To this end, the country applied to the European Commission on 14 January 2022, requesting authorisation for a special measure to derogate from articles 218 and 232 of Directive 2006/112/EC, which was granted on 25 July. This measure would allow for the introduction of mandatory electronic invoicing for all transactions carried out between taxable persons established in Romania.

Key takeaways from the derogation decision

The derogation will be effective from 1 January 2024. This means that Romania can enforce mandatory e-invoicing for all B2B transactions starting from January 2024, following the amendments in the local legislation.

The derogation will remain valid until 31 December 2026, or until the national transposition of the VAT in the Digital Age (ViDA) directive into Romanian law.

The introduction of mandatory e-invoicing will replace the current obligation to report information on domestic supplies.

What’s next?

The Romanian authorities will need to make the necessary amendments to local legislation to implement mandatory e-invoicing, following the derogation decision received by the EU Council.

The Romanian tax authority, ANAF, is expected to issue an order within 30 days from the date of the derogation which will define the scope and timeline for the implementation of the mandate. The order will provide more specific details about the upcoming mandate.

Considering the mandate could come into effect as early as January 2024, it’s crucial that taxpayers start preparing their systems for mandatory e-invoicing from now.

Looking for guidance to comply with Romania’s upcoming e-invoicing mandate? Our expert team can help.

Update: 24 January 2022 by Enis Gencer

Romania’s B2B E-invoicing Mandate for High-risk Products and E-transport System

With the most significant VAT gap in the EU (34.9% in 2019), Romania has been moving towards a CTC regime to improve and strengthen VAT collection while combating tax evasion.

The main features of this new e-invoicing system, e-Factura, are described further down in this blog. Here, we’ll take a closer look at the roll-out for B2B transactions and the definition of high-fiscal risk products, as well as the new e-transport system that was introduced through the Government Emergency Ordinance (GEO) no. 130/2021, published in the Official Gazette on 18 December.

What are high fiscal risk products?

According to GEO no. 120/2021 (the legislative act introducing the legal framework of e-Factura), the supplier and the recipient must both be registered with the e-Factura system. The recently published GEO no. 130/2021 establishes an exception for high fiscal risk products and ensures that taxpayers will use the e-Factura system regardless of whether the recipients are registered.

In line with the GEO no. 130/2021, the National Agency for Fiscal Administration has issued an order to clarify which products are considered high fiscal risk products.

The five product categories are as follows:

Vegetables, fruits, roots and edible tubers, other edible plants

Alcoholic beverages

New constructions

Mineral products (natural mineral water, sand and gravel)

Clothing and footwear

High fiscal risk products are defined based on the nature of the products, marketing method, traceability of potential tax evasion and degree of taxation in those sectors. Detailed explanations, as well as product codes, can be found in the Annex of GEO no. 130/2021.

The enforcement timeline of this requirement means that businesses that supply these types of products must be ready to comply with the new Romanian e-Factura system as follows:

From 1 April to 30 June 2022: It will be voluntary to submit invoices in the Romanian e-Factura system

From 1 July 2022: It will be mandatory to submit invoices in the Romanian e-Factura system

Looking ahead: introduction of an e-transport system

Another reform that shows the intention of the Romanian authorities to combat tax fraud and evasion is the introduction of an e-transport system.

Taxpayers will be required to declare the movement of goods from one location to another in advance. Once declared, the system will issue a unique number written on the transport documents. Authorities will then verify the declaration on the transport routes.

Moreover, it is stated in the justification letter that the e-transport system will interconnect with the Ministry of Finance’s current systems, Romanian e-invoice, and traffic control, much like similar initiatives in other countries, such as India, Turkey and Brazil.

The introduction of the e-transport system is still pending as the Ministry of Finance has not yet issued the order regarding the application procedure of the system. According to GEO 130/2021, the Ministry of Finance had 30 days to do so after GEO 130/2021 was published in the Official Gazette. However, the deadline expired on the 17 January, and no announcement has been made yet. Therefore, the details of the system are still unknown.

Take Action

Follow us on LinkedIn and Twitter to keep up-to-date with the latest regulatory news and updates.

Update: 16 November 2021 by Joanna Hysi

E-Factura – Romania’s New E-invoicing System

In March 2020, Romania launched an e-invoicing pilot program, e-Factura, to streamline the collection of taxes to improve and strengthen the collection of VAT whilst combating tax evasion.

The decision to launch e-Factura was taken after closely monitoring the Italian e-invoicing model and analysing the economic impact and efficiencies that electronic invoicing has had for both B2G and B2B transactions in Italy.

E-Factura is to implement a new e-invoicing system for B2G transactions but also lays the foundation for the extension of the platform for further developments and provides the necessary know-how to develop an e-invoicing system in B2B.

In October, Government Emergency Ordinance (GEO) no. 120/2021 introduced the legal framework for implementing e-Factura, regulating the structure of the Romanian e-invoice process and creating the framework for achieving basic technical specifications of the e-invoice system.

Further documentation regulating the use and operation of e-Factura and technical documentation such as API specifications and draft e-invoice schemas have also been published.

According to published documentation, the B2B e-invoicing process is not expected to differ from the B2G e-invoicing process, whose framework and relevant requirements are defined to a clearer standard.