Update: 25 June 2024 by Dilara İnal

The German Ministry of Finance (MoF) released a draft guideline on 13 June 2024, detailing the upcoming B2B e-invoicing mandate which will roll out on 1 January 2025.

Although the current law only obliges taxpayers to issue and receive e-invoices for domestic B2B transactions, the MoF plans to introduce an e-reporting system for invoice details at a later stage, with no set date.

The highlights from the guidelines are:

The final version of the guideline is expected by Q4 2024.

Update: 26 March 2024 by Dilara İnal

The German parliament passed the Growth Opportunities Act (Wachstumschancengesetz – the Act) concerning various tax matters on 22 March 2024, including a nationwide B2B electronic invoicing mandate.

The Act was originally scheduled for a vote at the end of 2023, with enforcement planned for January 2024. However, the lack of consensus between the Bundestag and Bundesrat – lower and upper houses of the parliament, respectively – in various provisions of the Act delayed its finalisation.

The Mediation Committee of the Bundestag and Bundesrat concluded its negotiations about the Act on 21 February 2024, and the Bundestag approved the amended text on 23 February. The Bundesrat’s vote on 22 March completed the parliamentary process.

The implementation timeline for this mandate has been confirmed as follows:

Mandatory receipt of e-invoices for domestic B2B transactions will be required for all businesses. Additionally, businesses will have the option to issue e-invoices that are compliant with the approved syntaxes based on CEN 16931 voluntarily, without the Buyer’s consent.

Following this parliamentary approval, the Act will be signed by the President and subsequently published in the official gazette.

Acceptable invoice formats to issue in following years:

| Domestic B2B Invoices | 2024 | 2025 | 2026 | 2027 | 2028 |

| Paper Invoices |

Allowed |

Prohibited for large taxpayers |

Prohibited for all |

||

| E-invoices in EN 16931 format |

Allowed with Buyer’s consent |

Allowed |

Mandatory for large taxpayers |

Mandatory for all |

|

| EDI invoice not EN 16931 format |

Allowed with Buyer’s consent |

Allowed if are interoperable with the CEN, if the required information can be extracted into CEN | |||

| Other invoices in e-form (e.g. PDF, JPEG) |

Allowed with Buyer’s consent |

Allowed if are interoperable with the CEN, if the required information can be extracted into CEN** Please note that exchange on EDI is permitted if the e-invoice aligns with European standards. |

|||

Is your organization unprepared for the upcoming mandate? Our expert team can help.

Update: 6 November 2023 by Dilara İnal

In October 2023, The Federal Ministry of Finance (MoF) released additional information regarding electronic invoicing, one of the proposed tax measures included in the Growth Opportunities Act.

If the MoF’s proposal, with the details provided in the preceding updates, becomes law, the following will be applicable:

Besides MoF clarifications, the upper house of the German Federal Parliament, Bundesrat, addressed the Act during its session on 20 October. While the Bundesrat supports the introduction of mandatory e-invoicing, it has proposed a two-year delay so the mandatory receipt of electronic invoices commences on 1 January 2027.

In the next steps of the process, the lower house of the Parliament, Bundestag, is expected to vote on the Growth Opportunities Act in mid-November. The upper house’s vote should take place in mid-December.

Looking for more information on the global adoption of e-invoicing? Read our definitive E-invoicing guide.

Update: 20 September 2023 by Dilara İnal:

On 30 August, the German Federal Government approved the draft act known as the “Growth Opportunities Act,”. The act consists of several provisions on different tax matters, including the introduction of a nationwide B2B e-invoicing mandate.

Key dates for implementation of the mandate include:

The draft bill approved by the government does not change the previously communicated framework, however it extends the voluntary phase by one year. The voluntary phase will last until January 2027 for small companies with annual turnover of 800,000 EUR or less in 2025.

The Federal Parliament and the Federal Council are expected to give their approval to this reform by the end of 2023.

Looking for additional guidance on invoicing in Germany? Speak with our team of experts.

Update: 4 August 2023 by Dilara İnal

The German Federal Ministry of Finance (the Ministry) shared the draft “Growth Opportunities Act” with significant German business associations on 14 July 2023. This act introduces amendments to VAT law to implement mandatory e-invoicing, along with other national and international tax-related proposals.

Currently, issuing an electronic invoice requires the buyer’s consent. Proposed amendments will change this, with invoices for transactions between German resident taxpayers – known as domestic B2B transactions – required to be electronic.

The act also introduces a new definition for e-invoices. An electronic invoice is defined as an invoice issued, transmitted and received in a structured electronic format that enables electronic processing. An e-invoice must also comply with the eInvoicing standard of the European Committee for Standardization (CEN), EN 16931.

The Ministry previously shared its plan to roll out mandatory e-invoicing as of January 2025. This date remains the same in the amendment proposals, with transitional measures giving taxpayers some time and flexibility to comply with the new requirements:

Even though this act does not include any provisions for a transaction-based reporting system, it notes that such a reporting system for B2B sales will be introduced later.

The European Council authorised Germany to introduce special measures regarding mandatory electronic invoicing with its decision dated 25 July 2023.

Germany received the derogation from the VAT Directive from 1 January 2025 to 31 December 2027 or, if an EU directive is adopted earlier than planned, until the national transposition of the VAT in the Digital Age (ViDA) directive into German law.

Looking for additional guidance on invoicing in Germany? Speak with our team of experts.

Update: 21 April 2023 by Anna Norden

The German Federal Ministry of Finance sent a discussion proposal for the introduction of mandatory B2B e-invoicing in Germany on 17 April to significant German business associations.

The business associations are requested to provide their opinion on matters such as the following by 8 May:

The proposed e-invoicing mandate is a step toward implementing a real-time transaction-based reporting system for creating, verifying and forwarding e-invoices. This system is not part of the current proposal, but – as this is directly related to an e-invoice mandate – the ideas for such a system are laid out at a high level by the Ministry of Finance.

The final aims to provide a uniform electronic transaction-based reporting system for national and cross-border B2B transactions. The invoice exchange would be done via a central or private platform.

No verification of the full invoice content would be performed or interruption of forwarding of the invoice – however, the issuer’s platform would check (“Plausibilitätsprüfungen”) that all mandatory fields are present, whether structure and syntax are EN-compliant and so on.

The reporting of the invoice would be in real-time at the same time as the invoice is sent so that the supplier would not have to initiate two transactions.

The Ministry of Finance states the aim is for the new system to be aligned with ViDA but that Germany counts on having to use a derogation from the provisions of the VAT Directive to introduce the e-invoice mandate, should ViDA not be adopted in time.

While many have speculated around Germany going down the path of the Italian e-invoicing system, the message from the Ministry of Finance seems rather to be that the cues are taken from the French system, with the use of a centralised platform complemented with private service providers who serve to channel the invoices.

Need to discuss how Germany’s proposal to introduce continuous transaction controls could affect your business? Speak to our tax experts.

Update: 3 November 2021 by Joanna Hysi

There’s been increased discussion among different institutions about the introduction of continuous transaction controls (CTCs) in Germany to combat tax fraud and boost the competitiveness of the German market in Europe.

Proponents of the introduction of CTCs in Germany include, among others: the parliamentary group of the business-friendly Free Democratic Party (FDP), the German Association for Electronic Invoicing (VeR) and an independent judiciary body, the German Bundesrechnungshof (Federal Audit Office).

Recently, we’ve seen this topic included in tax policy negotiations of the coalition partners that emerged from the recent German government elections (the Social Democratic Party (SPD), FDP, and the Green Party).

While the discussions remain at a conceptual level, the new potential coalition parties display political will for reform in this area.

Specifically, the German Bundesrechnungshof proposed to the Ministry of Finance a real-time reporting system leveraging blockchain technology as an efficient system to combat VAT fraud. However, their proposal wasn’t accepted on the grounds that a cost-benefit analysis is required before such measures are proposed and implemented.

As part of a parliamentary process the FDP called for “an electronic reporting system comparable to the Italian SDI to be introduced nationwide as quickly as possible, for the creation and testing and forwarding of invoices”. The leading German industry association, the VeR, welcomed this proposal recognising its numerous advantages to companies and the German economy.

A VeR study on whether the Italian model can be used as a blueprint for Europe explains that although it doesn’t seem to have contributed significantly to reducing Italy’s VAT gap, the advantages of e-invoicing to companies and the Italian economy are convincing. It concludes that the Italian clearance system can serve as a model for the digitization of VAT in Germany, if not in Europe. In addition, the VeR experts offer their knowledge to develop such a CTC system in Germany.

It seems that the idea of introducing a CTC system in Germany – following in the footsteps of fellow Member States like Italy, France and Poland – is gaining traction and might not be far from becoming reality if the coalition partners indeed manage to reach a coalition agreement to succeed the currently ruling party.

To find out more about what we believe the future holds, download VAT Trends: Toward Continuous Transaction Controls. Follow us on LinkedIn and Twitter to keep up-to-date with regulatory news and updates.

Black Friday Countdown: Are You VAT Ready with OSS?

Time: 14:00 BST / 09:00 EDT

Date: October 14, 2021

On 26 November, Black Friday presents another opportunity for retailers to drive e-commerce sales and boost revenue. Retailers will be working hard to prepare the best deals to entice shoppers, but do you know where you stand with VAT compliance in the EU?

In our latest webinar, learn how the new EU e-commerce VAT rules will apply to retail businesses ahead of this year’s annual shopping event. In addition, we’ll explain how this year B2C retailers can – for the first time in respect of goods – account for VAT on Black Friday sales in the EU using the VAT One Stop Shop (OSS) schemes. These schemes can greatly simplify VAT compliance by removing the need to register for VAT in multiple Member States.

Join Consulting Services Director Andy Spencer and Strategy Programs Director Anna Higgins in this webinar to learn:

We will host a short Q&A session at the end of this webinar.

Need more information? Sovos’ VAT managed service provides a full OSS service for your business. Let us handle the initial registration, monthly filling and any potential intermediary requirements. Click here to find out more.

On 1 July 2021 the EU E-Commerce VAT Package was introduced. The package replaced existing distance-selling rules and extended the Mini One Stop Shop (MOSS) into a wider-ranging One Stop Shop (OSS).

The implementation of the EU E-Commerce VAT Package was designed to simplify the VAT reporting requirements for sellers and improve the tax take for Member States.

Two months in: we take a look at how it’s going.

There were unfortunately some initial delays and teething problems when the EU E-Commerce VAT Package was introduced, which is to be expected with the adoption of such a significant new system, but as with any new scheme these can be resolved over time.

Some examples include:

There are also issues associated with the import of the goods.

Some Member States disallow the import of certain categories of goods due to local restrictions e.g. foodstuffs, plants etc.

It’s sometimes unclear if freight forwarders have used IOSS or not and this could lead to repeated errors of underpayment or overpayment of VAT.

Some non-EU vendors are trying to avoid an IOSS registration by stating that the customer is the importer of record. Such practice happened before the introduction of IOSS but not always at the same level as it is now – and was not always spotted or queried.

However, since the introduction of the IOSS, some tax authorities, including Germany, are questioning such an approach on the grounds that the carrier who imports the goods is acting for the non-EU vendor and is not known by the buyer.

This means import VAT is due by the vendor who must then also charge German VAT. For cases that have already occurred there may be an issue with recovery of the import VAT, as the evidence required to support the deduction will have been issued in the wrong name (consumer).

It’s still early days for the EU VAT E-Commerce Package and initial teething problems are to be expected. One thing is certain, navigating these new VAT schemes is complex. Sovos is here to help and we’ll keep you updated on the latest regulatory changes.

Join our latest webinar on September 22, 2021 to learn how you can use the Import One-Stop Shop (IOSS) to simplify your EU VAT compliance and unlock the full potential of the EU e-commerce market.

Still have questions about OSS and IOSS? Download our e-book to understand the implications of the 2021 EU e-commerce VAT package and ensure your business is ready by 1 July 2021 for the significant changes ahead

Simplify EU VAT with IOSS – Unlock the EU E-Commerce Market

Time: 3:00pm BST / 10:00 EDT

Date: September 22, 2021

Join our latest webinar to learn how you can use the Import One-Stop Shop (IOSS) to simplify your EU VAT compliance and unlock the full potential of the EU e-commerce market.

Since July 2021, the low value consignment relief on small packages has been removed. From the same date, businesses selling imported goods valued at less than EUR 150 can now use IOSS to collect, declare and pay VAT to the local tax authorities in one single VAT return. IOSS simplifies your EU VAT compliance – making it essential to grow sales in the EU, avoid fines and penalties, and provide an excellent customer service.

Join Consulting Services Director Alex Smith and Senior Consultant Russell Hughes in this webinar to learn:

We will host a short Q&A session at the end of this webinar.

Need more information? Sovos’ VAT managed service provides a full IOSS service for your business. In addition to proving an intermediary service, we handle the IOSS registration and monthly filling. Click here to find out more.

Back in 2019, Portugal passed a mini e-invoicing reform consolidating the country’s framework around SAF-T reporting and certified billing software.

Since then, a lot has happened: non-resident companies were brought into the scope of e-invoicing requirements, deadlines have been postponed due to Covid, and new regulations were published. This blog summarises the latest and upcoming changes.

Introduced in 2019, the de facto implementation of the QR code requirement was delayed, and is now expected to be fully implemented by taxpayers in January 2022. A QR code should be included in all invoices. Technical specifications about the content and placement of the code in the invoice are available on the tax authority’s website.

The ATCUD is a unique ID number to be included in invoices and is part of the content of the QR code. The ATCUD is a number with the following format ‘ATCUD:Validation Code-Sequential number’.

To obtain the first part of the ATCUD – the so-called ‘validation code’ -, taxpayers must communicate the document series to the tax authority along with information such as type of document, first document number of the series, etc.

In return, the tax authority will deliver a validation code. The validation code will be valid for the whole document series for at least a fiscal year. The second part of the ATCUD – the ‘sequential number’ – is a sequential number within the document series.

This month, the Portuguese tax authority published technical specifications for obtaining the validation code, creating a new web service. To access this web service, a specific certificate obtained from the tax authority is required and can be assigned to taxpayers or software service providers.

In addition, the tax authority has created a standard list of document classes and types, enabling the communication of document types in a structured format.

An ATCUD will be required in all invoices from January 2022. To be ready for the deadline, taxpayers must get the series’ validation codes during the last half of 2021 to apply in invoices issued in the beginning of 2022.

In April this year, Portugal clarified that non-resident companies with a Portuguese VAT registration should comply with domestic VAT rules. This includes the use of certified billing software for invoice creation, among others. These companies must also ensure integrity and authenticity of e-invoices. In Portugal, integrity and authenticity of invoices are presumed with the use of a qualified electronic signature or seal, or use of EDI with contracted security measures.

Consequently, since 1 July 2021, non-established but VAT registered companies must adopt certified billing software to comply with the Portuguese law as required by Law-Decree 28/2019, Decision 404/2020-XXII, and Circular 30234/2021.

The Portuguese e-invoicing mandate for business-to-government transactions includes a format requirement attached to specific transmission methods. In other words, invoices to the public administration must be issued electronically in the CIUS-PT format and transmitted through one of the web services made available by the public administration.

Initially, a phased roll-out started in January 2021, obliging large companies to issue e-invoices to public buyers. In July, the subjective scope was enlarged to include small and medium-sized businesses. The last step is to include microenterprises by January 2022.

Due to the Covid pandemic, Portugal established a grace period that has been renewed several times, whereby PDF invoices would be accepted by the public administration. Currently, the grace period runs until 31 December 2021, meaning that, in practice, all suppliers of the public administration, regardless of their size, should comply with the e-invoicing rules in public procurement by 1 January 2022.

Need to ensure compliance with the latest e-invoicing regulations? Get in touch with our tax experts at Sovos.

In our last look at Romania SAF-T, we detailed the technical specifications released from Romania’s tax authority. Since then, additional guidance has been released including an official name for the SAF-T submission: D406.

To alleviate taxpayer concerns due to the complexity of the report and difficulties with extraction, the tax authorities are introducing a voluntary testing period which is due to begin in the coming weeks. During this period, taxpayers may submit what is known as D406T which will contain test data that the authorities will not use in the future for audit purposes.

The Romanian SAF-T, D406, is based on the OECD schema version 2.0 which contains five sections:

The submission deadlines are as follows:

Taxpayers must submit sections of D406 monthly or quarterly, following the applicable tax period for VAT return submission.

For the first report, tax authorities have announced a grace period for the first three months of submission. This is from the date when the deposit obligation becomes effective for that taxpayer, where non-filing or incorrect filing will not result in penalization if correct submissions are submitted once the grace period ends.

The D406 must be submitted electronically in PDF format, with an XML attachment and electronic signature. The size of the two files must not exceed 500 MB. If the file is larger than the maximum limit, the portal will not accept it and the file must be divided into segments according to details set out in the Romanian guidance.

The tax authorities have indicated that, should a taxpayer find errors in the original submission, a corrective statement may be submitted to rectify these errors. The taxpayer should submit a second full corrected file to replace the original file that contains errors. If a taxpayer submits a second D406 for the same period, it is automatically considered a corrective statement.

Need to ensure compliance with the latest Romania SAF-T requirements? Speak to our team. Follow us on LinkedIn and Twitter to keep up-to-date with the latest regulatory news and updates or see this overview on VAT Compliance in Romania.

Welcome to our Q&A two-part blog series on the French e-invoicing and e-reporting mandate, which comes into effect 2023-2025. That sounds far away but businesses must start preparing now if they are to comply.

The Sovos compliance team has returned to answer some of your most pressing questions asked during our webinar.

We have outlined the new mandate, e-invoicing specifically, and questions around this topic in our first blog post.

This blog will look at the other side of the mandate – e-reporting obligations. These will apply to B2C and cross-border B2B transactions in France, which must be periodically reported.

First let’s look at common questions around payments e-reporting.

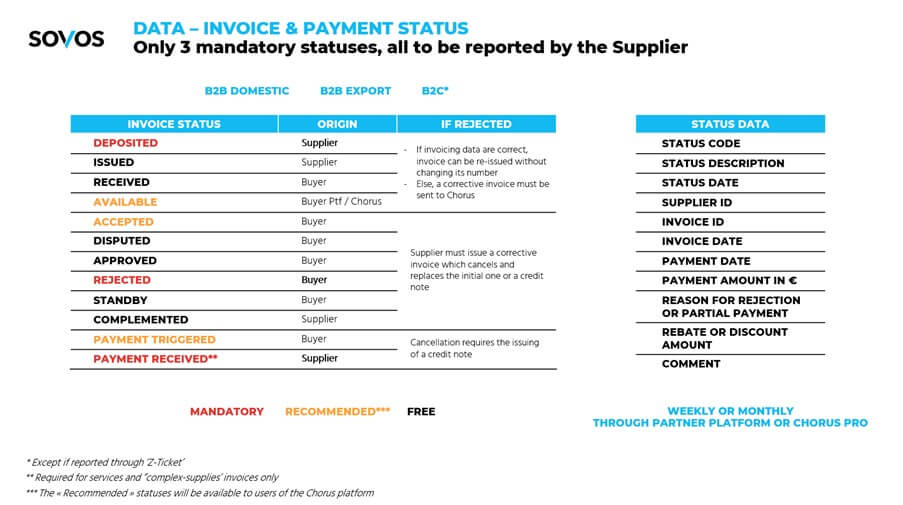

What are the invoice and payment statuses to be reported?

Here is a slide from our webinar showing invoice statuses, whether these are mandatory, recommended, or free, origins, action to take if rejected, status data, and when it needs to be reported:

Who is responsible for payment e-reporting? The buyer, the seller, or both?

It was initially rumoured to be both on the buyer and the seller side, but the latest information from DGFIP clearly states that it will be the responsibility of the seller to report the invoice status, and, if applicable, its payment status.

Some further clarification is needed though since the seller is dependent on the buyer’s response on some status (e.g. ‘invoice rejected’).

Your e-invoicing and e-reporting project cannot be done in isolation. This is a significant project with many dependencies that involve external third parties.

There will be one or, in most likelihood, several third parties in the middle of the transaction chain. This will include Chorus Pro, chosen by the French government as the official and obligatory platform for businesses to issue e-invoices to public administrations.

This section covers common questions on partner platform certification requirements.

Is there a list of official validated partner platforms?

The 13 July 2021 DGFIP workshop dedicated to this matter highlighted that there would be a registration process for third-party platforms, as well as taxpayers who would want to run their own platform.

The registration process will consist of two phases:

Phase 1. A prior selection by the tax authorities based on the general profile of the candidate (e.g. are they up to date in their own tax payment duties?) and the services they propose;

Phase 2. Within 12 months after registration, an independent audit would have to performed that demonstrates that the platform meets the DGFIP requirements, such as:

<liPerforming the control and mapping activities (extraction of invoicing data for both e-invoicing and e-reporting, certain invoice validation checks – mandatory fields, check sums, Customer ID verification – mapping to and from a minimum set of mandatory formats, compliance with GDPR, etc)

A few other key points to note are:

What is the current expectation on when exact required fields with be supplied by the government (invoice specs with all required fields and values)?

Excel files are available as a draft document at a very detailed level which Sovos can provide on request. The final specs should be known by the end of September 2021.

Still have questions about e-reporting? Access our webinar on-demand for more information and advice on how to comply.

In our recent webinar, Sovos covered the new French e-invoicing and e-reporting mandate, and what this means for businesses and their tax obligations.

We are witnessing a global move towards Continuous Transaction Controls (CTCs), where tax authorities are demanding transactional data in real-time or near real-time, affecting e-invoicing and e-reporting obligations.

As such, from 2023, France will implement a mandatory B2B e-invoicing clearance and e-reporting obligation in an effort to increase tax efficiency, cut costs, and fight fraud.

The pace towards this mandate has been accelerating lately with the adoption of the Finance law for 2021, followed by a number of workshops organised by the Ministry of Finance — namely the Direction Générale des Finances Publiques (DGFIP).

In the first of two blogs on the mandate, we answer some of your most pressing questions asked during our webinar.

In part one, we focus on setting the scene in terms of scope, and cover questions around e-invoicing specifically, invoicing file formats, processes and controls, and archiving.

The second blog covers questions around e-reporting obligations.

In this section, we answer questions on the scope of the regulation, such as which companies must comply with the mandate and how.

Are non-resident companies (foreign companies with only a French VAT-registration) obliged to fulfil this new regulation? Are foreign legal entities with a French VAT number in scope?

The Budget Laws for 2020 and 2021 introduced the CTC scheme from a legal perspective. Both include “persons subject to VAT” in the scope.

VAT registration is a strong indication that a company is subject to VAT, but classification as a VAT “taxable person” also depends on other factors.

Therefore, it is not as simple as just looking at whether a company has a local VAT registration, to decide whether it is subject to VAT and therefore targeted by the mentioned budget laws.

However, the scope cannot be unilaterally decided by France as the French CTC scheme is dependent on a derogation from the EU Council.

As a comparison, Italy initially included all taxable persons in the scope of its e-invoicing clearance mandate, including those with a mere VAT registration but no establishment. But in this case, the EU Council limited the scope (of its derogation) to persons established in Italy.

From an e-invoicing perspective, we can therefore expect that France will need to follow the Italian path (due to its reliance on a derogation from the EU Council), limiting the scope to established persons.

DGFIP has however suggested that companies that are non-established but VAT registered will be in scope of the reporting obligation.

Is import of goods in the scope of e-reporting? What about import of services?

Only imports (supplies from outside of the EU) of services are in the scope of the current proposal.

In this section, we discuss permitted e-invoice formats.

The fact that the new regime creates a specific process for domestic B2B e-invoicing does not change the need for businesses to demonstrate the integrity and authenticity of each invoice.

This can be done through one of the 3 legal methods defined by the existing regulations:

To ensure there’s no impact of the reform on integrity and authenticity demonstration methods, one can still apply any of them.

However, with the new regime, e-invoicing data sent to the DGFIP does need to be in a structured format.

Will digital signatures be required?

Digital signatures are not strictly required today and will not be strictly required in the new scheme. Integrity and authenticity will still need to be ensured though, irrespective of invoice format, as is the case today.

The options remain the same; use of digital signatures, use of EDI with security measures, or the BCAT option whereby the audit trail should prove the transaction and its authenticity and integrity.

Are PDF and XML invoice file formats still possible to receive from 2023-2025?

The legal invoice format can be anything, as long as the supplier and buyer agree on it and the integrity and authenticity are guaranteed. Also, a human readable version (normally a PDF) is required upon audit as part of the general EU requirements.

What e-invoicing formats are permitted?

This is not fully defined yet, but DGFIP has indicated the following syntax, based on the EN16931 standard:

Those formats would apply to:

In this section, we answer questions around the processes for sending and receiving e-invoices, what information they need to include, and the Chorus Pro platform.

Will the e-invoice need to be sent real-time?

Yes, it can be considered a “real-time clearance system”. As part of the e-invoicing obligation, the reporting of mandatory data to the tax authorities and the issuance of the original invoice to the buyer by the supplier’s partner platform should happen right after receiving the invoicing data from the supplier.

If the invoice doesn’t have all the mandatory information like the SIRET number of a customer, will the Chorus Pro platform clear it?

Will Chorus Pro also be validating the VAT rates used?

No, or at least not on the fly when submitting the invoicing data to Chorus Pro. Our understanding is that those verifications will be done by the tax authorities after the fact, using data analytics / AI algorithms.

Are there common data, connection and bridges with the current SAF-T?

The French version of SAF-T (FEC) must still be available on demand from the tax authorities.

In this section, we answer questions around compliant archiving of e-invoices.

Does the Chorus Pro/Tax Authority portal provide a compliant electronic archive for AP/AR invoices in France?

Yes. However, in our experience, even though a tax authority’s archiving solution would be available for taxable persons, few larger companies choose to solely rely on it for evidence purposes and instead continue to use their compliant internal or third-party archiving solutions.

This decision is ultimately based on the fact that the tax authority’s archiving solution poses a conflict of interest: it is maintained by the tax authority, which, from a legal perspective, is not an independent party but rather the counterparty in a fiscal claim.

In fact, from discussions with many experts and customers over that past year, we see that the market request for third-party archiving services is even stronger after the introduction of clearance, especially as customers see a need to store not only the invoice but also response messages from the CTC portal to further maintain evidence of compliance.

Still have questions about the e-invoicing mandate? Access our webinar on-demand for more information and advice on how to comply.

Intrastat is a reporting regime relating to the intra-community trade of goods within the EU.

Under Regulation (EC) No. 638/2004, VAT taxpayers who are making intra-community sales and purchases of goods are required to complete Intrastat declarations when the reporting threshold is breached.

Intrastat declarations must be completed in both the country of dispatch (by the seller) and the country of arrival (by the purchaser). The format and data elements of Intrastat declarations vary from country to country, though some data elements are required in all Member States. Reporting thresholds also vary by Member State.

In an effort to improve data collection and ease the administrative burden on businesses an ‘Intrastat Modernisation’ project was launched in 2017. As a result of this project Regulation (EU) 2019/2152 (the Regulation on European business statistics) was adopted.

The practical effects of these changes are two-fold:

Currently Member States are required to collect the following information as part of Intrastat:

To ease compliance burdens on small businesses, EU Member States are allowed to set thresholds, under which businesses are relieved of their obligations to complete Intrastat. Thresholds are set annually by Member States, and threshold amounts for arrivals and dispatches are set separately.

Under the current regulations, Member States cannot set thresholds at a level that results in less than 97% of dispatches from the Member State being reported and cannot set thresholds at a level that results in less than 93% of intra-community arrivals to the Member State being reported.

Under current regulations Member States are allowed to let certain small businesses report simplified information, so long as the value of trade subject to simplified reporting does not exceed 6% of total trade.

Under the upcoming new regulation, Member States need only ensure that 95% of dispatches are reported and the exchange of data on intra-community arrivals between Member States is optional.

Need to ensure compliance with the latest Intrastat requirements? Get in touch with our tax experts.

Progress has been made in the roll-out of the Polish CTC (continuous transaction control) system, Krajowy System of e-Faktur. Earlier this year, the Ministry of Finance published a draft act, which is still awaiting adoption by parliament to become law. Draft e-invoice specifications have been released and there has been a public consultation on the CTC system.

In June, the Ministry of Finance announced it had reviewed all comments submitted by the public and Polish ministers on the CTC system and decided to take the following actions:

In the announcement, the Minister outlined the benefits of adopting the CTC system for taxpayers. These include: quicker VAT refunds; security of the stored invoice in the tax authority’s database until the end of the mandatory storage period; certainty about the invoice delivery to the recipient through the CTC platform and therefore quicker invoice payments; automation of the invoice processing and exchange due to the adoption of a standardized e-invoice format.

In addition, as a result of the new e-invoicing rules upcoming changes in the SLIM VAT 2 package will trigger further relief measures, e.g. around the handling of duplicates and corrective invoices.

The Polish authorities are making good progress in the implementation of the Krajowy System e-Faktur. It is positive to see that the public consultation has proven useful in defining next steps and the authorities’ intent for transparency and timely documentation will hopefully continue throughout the entire CTC roll-out.

To find out more about what we believe the future holds, download Trends: Towards Continuous Transaction Controls.

For more information see this overview about e-invoicing in Poland, Poland SAF-T or VAT Compliance in Poland.

More than 170 countries throughout the world have implemented a VAT system, and some of the most recent adopters are the Gulf countries. In a bid to diversify economic resources, the Gulf countries have spent the past decade investigating other ways to finance its public services.

As a result, in 2016 the GCC (Gulf Cooperation Council), consisting of Saudi Arabia, UAE, Bahrain, Kuwait, Qatar and Oman, signed the Common VAT Agreement to introduce a VAT system at a rate of 5%.

Following the VAT agreement, Saudi Arabia and UAE implemented VAT in 2018. Bahrain followed with a VAT regime in 2019. Most recently Oman enforced a 5% VAT from April 2021, and looking ahead both Qatar and Kuwait are expected to enact VAT laws within the next year.

After the implementation of VAT and the increase of VAT rate from 5% to 15%, Saudi Arabia has taken the next step to digitize the control mechanisms for VAT compliance.

The E-invoicing Regulation enacted in December 2020 sets out an obligation for all resident taxable persons to generate and store invoices electronically. This requirement will be enforced from 4 December 2021.

Saudi Arabia has made considerable progress since it first introduced VAT in 2018. The Saudi E-invoicing Regulation is expected to not only encourage digitization and automation for businesses, but also to achieve efficiency in VAT controls and better macro-economic data for its tax authority, a development which will likely be replicated by other GCC countries soon.

Considering the efforts involved in the digitization of government processes and the VAT implementation timeline, the next candidate for similar e-invoicing adoption would likely be the UAE. While there are currently no plans for a mandatory framework, the UAE has announced bold plans for general digitization. According to the UAE government website, “In 2021, Dubai Smart government will go completely paper-free, eliminating more than 1 billion pieces of paper used for government transactions every year, saving time, resources and the environment.”

The spread of VAT digitization is typically the second reform following VAT adoption. As Bahrain and Oman also have VAT systems in place, introduction of mandatory e-invoicing in the next a few years in these countries would not come as a surprise. The adoption of e-invoicing in Qatar and Kuwait would depend on the success of VAT implementation, therefore it is not easy to estimate when their VAT digitization journey will begin but there is no doubt that it will happen at some stage.

After the adoption of e-invoicing, the Gulf countries may continue to digitize other VAT processes, including VAT returns. Pre-population of VAT returns using the data collected through e-invoicing systems is another trend that the countries are moving towards.

Regardless of the shape and form of digitization, there will be many moving parts in terms of VAT and its execution. Businesses operating in the region should be prepared to invest in their VAT compliance processes to avoid unnecessary fines and reputational risk for non-compliance.

To find out more about what we believe the future holds, download VAT Trends: Toward Continuous Transaction Controls. Follow us on LinkedIn and Twitter to keep up-to-date with regulatory news and updates.

A current mega-trend in VAT is continuous transaction controls (CTCs), whereby tax administrations increasingly request business transaction data in real-time, often pre-authorising data before a business can progress to the next step in the sales or purchase workflow.

When a tax authority introduces CTCs, companies tend to view this as an additional set of requirements to be implemented inside ERP or transaction automation software by IT experts. This kneejerk reaction is understandable as implementation timelines tend to be short and potential sanctions for non-compliance significant.

But businesses would do better to approach these changes as part of an ongoing journey to avoid inefficiencies and other risks. From a tax authority perspective, CTCs are not a standalone exercise but part of a wider digital transformation strategy where all data that can be legally accessed for audit purposes is transmitted to them electronically.

In many tax authorities’ vision of digitization, each category of data is received at ‘organic’ intervals that follow the natural cadence of data processing by the businesses and data needs of governments.

Tax administrations use digitization to access data more conveniently, on a more granular level, and more frequently.

A business that doesn’t consider this continuum from the old world of reporting and audit to the new world of automated data exchange risks over-focusing on the ‘how’ – the orchestration of messages to and from a CTC platform – rather than keeping a close eye on the ‘why’ – transparency of business operations.

Data received quicker and in a structured, machine-exploitable format is infinitely more valuable for tax administrations as it gives them an opportunity to perform deeper analysis of both varying taxpayer and third-party sources of data.

If your business data is incomplete or faulty, you are likely exposing yourself to increased audits, as your bad data is under scrutiny and more transparent to the taxman.

Put differently, in a digitized world of tax, garbage-in will translate to garbage-out.

Many companies already have the magic formula to fix these data issues at their fingertips. Start by preparing for this wave of VAT digitization with a project to analyse internal data issues and work with upstream internal and external stakeholders – including suppliers – to fix them.

Tools designed to introduce automated controls for VAT filing processes can help achieve better insight into the upstream data issues that need ironing out. These same tools can also help you through the CTC journey by re-using data extraction and integration methods set up for VAT reporting for CTC transmission, thereby creating better data governance and keeping a connection between these two naturally linked processes.

A lot of bad data stems from residual paper-based processes such as paper or PDF supplier invoices or customer purchase orders. Taking measures now to switch to automated processes based on structured, fully machine-readable alternatives will make a big difference.

Improving invoice data is not the only challenge. With the inevitable broadening of document types to be submitted under CTC rules (from invoice to buy-side approval messages, to transport documents and payment status data) tax administrations will cross-check more and more of your data, as well as trading partners’ and third parties’ data — think financial institutions, customs, and other available data points.

Tax administrations are unlikely to stop their digitization efforts at indirect tax. Mandates to introduce The Standard Audit File for Tax (SAF-T ) and similar e-accounting requirements show how quickly countries are moving away from the old world of tax and onsite audits.

All this data, from multiple sources with strong authentication, will paint an increasingly detailed and undeniable picture of your business operations. It is just a matter of time before corporate income tax returns will be pre-filled by tax administrations who expect little to no legitimate changes from your side.

‘Substance over form’ is a popular aphorism in the world of tax. As more business applications and data streams become readily accessible by tax administrations, you need to start considering data quality and consistency as a first step towards thriving in the world of digitized tax enforcement.

In the end, tax administrations want to understand your business. They don’t just want data, they want meaningful information on what you do, why you do it, how you trade, with whom and when. This is also exactly what your owners and management want.

So the ultimate goals are the same between businesses and tax administrations – it’s just that businesses will often prioritise operational efficiency and financial objectives whereas tax administrations focus on getting the best, most objective information possible.

Tax administrations introducing CTCs as an objective may be a blessing in disguise, and there are benefits of introducing better analytics to your business to comply with tax administration requirements.

The real value lies in real-time insight into business operations and financial indicators such as cash management or supply chain weaknesses. This level of instant insight into your own business also enables you to always be one step ahead, leaving you in control of the picture your data is providing to governments.

CTCs are the natural next step on a journey to a brave new world of business transparency.

Download VAT Trends: Toward Continuous Transaction Controls for other perspectives on the future of tax. Follow us on LinkedIn and Twitter to keep up-to-date with regulatory news and developments.

Update: 23 March 2023 by Dilara İnal

Japan is moving closer to the roll-out of its Qualified Invoice System (QIS), which will happen in October 2023.

Under QIS rules, taxpayers will only be eligible for input tax credit after being issued a qualified invoice. However, exceptions exist where taxpayers do not require a qualified invoice to take input credit.

The new system does not entail mandatory e-invoice issuance, though QIS introduces the following requirements for invoices:

While only taxpayers can register and obtain a QIIN, a supplier exempt from Japanese Consumption Tax (JCT) can register under the QIS – provided that it voluntarily applied to become a taxpayer.

In line with the implementation of the new invoicing system, the Japanese government’s 2023 Tax Reform introduces new measures for the QIS transition. It is implementing efforts to reduce the tax liability amount for three years.

The measures will also lessen the administrative burden on businesses below a specific size for six years. The government will allow companies to take an input tax deduction for book purposes, but only for small-amount transactions.

Need assistance preparing for Japan’s QIS? Our expert team is ready and waiting to speak with you.

Update: 13 July 2021 by Coskun Antal

Japan is in the middle of a multi-year process of updating its consumption tax system. This started with the introduction of its multiple tax rate system on 1 October 2019 and the next step is expected to be the implementation of the so-called Qualified Invoice System as a tax control measure on 1 October 2023.

Through this significant change, the Japanese government is attempting to solve a tax leakage problem that has existed for many years.

The Japanese indirect tax is referred to as Japanese Consumption Tax (JCT) and is levied on the supply of goods and services in Japan. The consumption tax rate increased from 8% to 10% on 1 October 2019. At the same time, Japan introduced multiple rates, with a reduced tax rate of 8% applied to certain transactions.

Currently, Japan doesn’t follow the common practice of including the applicable tax rate in the invoice to calculate consumption tax. Instead, the current system (called the ledger system) is based on transaction evidence and the company’s accounting books. The government believes this system causes systemic problems related to tax leakage.

A new system – the Qualified Invoice System – will be introduced from 1 October 2023 to counter this. The key difference when compared to an invoice issued today is that a qualified invoice must include a breakdown of applicable tax rates for that given transaction.

Under the new system, only registered JCT payers can issue qualified tax invoices, and on the buyer side of the transaction, taxpayers will only be eligible for input tax credit where a qualified invoice has been issued. In other words, the Qualified Invoice System will require both parties to adapt their invoicing templates and processes to specify new information as well as the need to register with the relevant tax authorities.

A transitional period for the implementation of the new e-invoicing system applies from 1 October 1 2019 until 1 October 2023.

In order to issue qualified invoices, JCT taxpayers must register with Japan’s National Tax Agency (“NTA”). It will be possible to apply for registration from 1 October 1 2021 at the earliest, and this application must be filed no later than 31 March 2023, which is six months in advance of the implementation date of the e-invoicing system. Non-registered taxpayers will not be able to issue qualified invoices.

The registered JCT payers may issue electronic invoices instead of paper-based invoices provided that certain conditions are met.

The introduction of the Qualified Invoice System will affect both Japanese and foreign companies that engage in JCT taxable transactions in Japan. To ensure proper tax calculations and input tax credit, taxpayers must make sure they understand the requirements, and update or adjust their accounting and bookkeeping systems to comply with the new requirements in advance of the implementation of the Qualified Invoice System in 2023.

Get in touch with our experts who can help you prepare for the Japanese Qualified Invoice System.

Turkey’s e-transformation journey, which started in 2010, became more systematic in 2012. This process first launched with the introduction of e-ledgers on 1 Jan 2012 and has since reached a much wider scope for e-documents.

The Turkish Revenue Administration (TRA), the leader of the e-transformation process, has played an important role in encouraging companies to embrace the digitalization of tax and created a successful model for following tax-related procedures.

You can read more about Turkey’s e-transformation in our e-book Navigating Turkey’s Evolving Tax Landscape.

The process was further accelerated with new requirements for e-documents.

The TRA continues to widen the scope of e-documents and the types of e-documents in use are:

Many taxpayers have voluntarily adopted the new system since the TRA launched this whole process and TRA’s latest updates for e-documents are critically important to monitor for tax-related procedures.

As e-documents become more popular, any income loss arising from tax procedures will reduce. E-documents offer additional advantages for public institutions and private businesses, such as saving time, minimising costs and improving productivity. It’s certain that the scope of e-documents in Turkey will keep expanding in the future, which will affect taxpayers and tax procedures.

Get in touch to find out how Sovos tax compliance software can help you meet your e-transformation and e-document requirements in Turkey.

In this blog, we provide an insight into continuous transaction controls (CTCs) and the terminology often associated with them.

With growing VAT gaps the world over, more tax authorities are introducing increasingly stringent controls. Their aim is to increase efficiency, prevent fraud and increase revenue.

One of the ways governments can gain greater insight into a company’s transactions is by introducing CTCs. These mandates require companies to send their invoice data to the tax authority in real-time or near-real-time. One popular CTC method requires an invoice to be cleared before it can be issued or paid. In this way, the tax authority has not only visibility but actually asserts a degree of operational control over business transactions.

The basic principle of VAT (value-added tax) is that the government gets a percentage of the value added at each step of an economic chain. The chain ends with the consumption of the goods or services by an individual. VAT is paid by all parties in the chain including the end customer. However only businesses can deduct their input tax.

Many governments use invoices as primary evidence in determining “indirect” taxes owed to them by companies. VAT is by far the most significant indirect tax for nearly all the world’s trading nations. Many countries with VAT see the tax contribute more than 30% of all public revenue.

The VAT gap is the overall difference between expected VAT revenues and the amount actually collected.

In Europe, the VAT gap amounts to approximately €140 billion every year according to the latest report from the European Commission. This amount represents a loss of 11% of the expected VAT revenue in the block. Globally we estimate VAT due but not collected by governments because of errors and fraud could be as high as half a trillion EUR. This is similar to the GDP of countries like Norway, Austria or Nigeria. The VAT gap represents some 15-30% of VAT due worldwide.

Continuous transaction controls is an approach to tax enforcement. It’s based on the electronic submission of transactional data from a taxpayer’s systems to a platform designated by the tax administration, that takes place just before/during or just after the actual exchange of such data between the parties to the underlying transaction.

A popular CTC is often referred to as the ‘clearance model’ because the invoice data is effectively cleared by the tax administration and in near or real-time. In addition, CTCs can be a strong tool for obtaining unprecedented amounts of economic data that can be used to inform fiscal and monetary policy.

The first steps toward this radically different means of enforcement began in Latin American within years of the early 2000s. Other emerging economies such as Turkey followed suit a decade later. Many countries in LatAm now have stable CTC systems. These require a huge amount of data for VAT enforcement from invoices. Other key data – such as payment status or transport documents – may also be harvested and pre-approved directly at the time of the transaction.

Electronic or e-invoicing is the sending, receipt and storage of invoices in electronic format without the use of paper invoices for tax compliance or evidence purposes. Scanning incoming invoices or exchanging e-invoice messages in parallel to paper-based invoices is not electronic invoicing from a legal perspective. E-invoicing is often required as part of a CTC mandate, but this doesn’t have to be the case; in India, for example, the invoice must be cleared by the tax administration, but it’s not mandatory to subsequently exchange the invoice in a digital format.

The objective of CTCs and e-invoicing mandates is often to use business data that is controlled at the source, during the actual transactions, to prefill or replace VAT returns. This means that businesses must maintain a holistic understanding of the evolution of CTCs and their use by tax administrations for their technology and organisational planning.

As more governments realise the revenue and economic statistics benefits that introducing these tighter controls bring, we’re seeing more mandates on the horizon. We expect the rise of indirect tax regimes based on CTCs to accelerate sharply in the coming five to 10 years. Our expectation is that most countries that currently have VAT, GST or similar indirect taxes will have adopted such controls fully, or partially, by 2030.

Looking ahead, as of today we know that in Europe within the next few years that France, Bulgaria and also Poland will all introduce CTCs. Saudi Arabia has also recently published rules for e-invoicing and many others will follow suit.

Upcoming mandates present an opportunity for a company’s digital transformation rather than a challenge. If viewed with the right mindset. But, as with all change, preparation is key. Global companies should allow enough time and resources to strategically plan for upcoming CTC and other VAT digitization requirements. A global VAT compliance solution will suit their needs both today and into the future as the wave of mandates gains momentum across the globe.

With coverage across more than 60 countries, contact us to discuss your VAT e-invoicing VAT requirements.

Since 1993, supplies performed between Italy and San Marino have been accompanied by a set of customs obligations. These include the submission of paperwork to both countries’ tax authorities.

After the introduction of the Italian e-invoicing mandate in 2019, Italy and San Marino started negotiations to expand the use of e-invoices in cross-border transactions between the two countries. Those negotiations have finally bore fruit, and details are now available.

Italy and the enclaved country of San Marino will abandon paper-based customs flows.

The Italian and Sammarinese tax authorities have decided to implement a “four-corner” model, whereby the Italian clearance platform SDI will become the access point for Italian taxpayers, while a newly created HUB-SM will be the SDI counterpart for Sammarinese taxpayers.

Cross-border e-invoices between the countries will be exchanged between SDI and HUB-SM. The international exchange system will be enforced on 1 July 2022, and a transition period will be in place between 1 October 2021 and 30 June 2022.

HUB-SM’s technical specifications are now available for imports from Italy to San Marino, and exports from San Marino to Italy. The countries have also decided to choose FatturaPA as the e-invoice format, although content requirements for export invoices from San Marino will slightly differ from domestic Italian FatturaPA e-invoices.

The SDI and HUB-SM systems will process e-invoices to and from taxpayers connected to them, or under each country’s jurisdictions.

In other words, Italian taxpayers will send and receive cross-border invoices to or from San Marino via the SDI platform, while Sammarinese taxpayers will perform the same activities via HUB-SM.

Both platforms will deliver invoices to the corresponding taxpayers through the Destination Codes assigned by the respective tax authorities. This means HUB-SM will also assign Destination Codes for Sammarinese companies.

Inspired by the Italian methodology for fiscal controls in cross-border transactions, San Marino will require Sammarinese buyers to fill out an additional integration document (similar to a “self-billing” invoice created for tax evidence reasons) upon receipt of the FatturaPA. This document will be filled out in a new XML-RSM format created by the enclave and sent to HUB-SM.

After the larger rollout of the SDI for B2B transactions in 2019, the platform has proven capable of adapting to new workflows and functionalities.

Since last year, e-purchase orders from the Italian National Health System have been exchanged through the NSO, an add-on to the SDI platform. In January 2022, the FatturaPA replaces the Esterometro as a cross-border reporting mechanism.

SDI has already debuted in the international arena through the acceptance of the e-invoices following the European Norm, which are mapped into a FatturaPA before being delivered to Italian buyers. This integration between SDI and HUB-SM might also reveal the early steps of interoperability between both tax authorities’ platforms for cross-border trade.

Get in touch with our experts who can help you understand how SDI and HUB-SM will work together.

Download VAT Trends: Toward Continuous Transaction Controls to find out more about the future of tax systems around the world.

Starting in 2023, French VAT rules will require businesses to issue invoices electronically for domestic transactions with taxable persons and to obtain ‘clearance’ on most invoices before their issue. Other transactions, such as cross-border and B2C, will be reported to the tax authority in the “normal” way.

This will be a major undertaking for affected companies and although the changes are more than a year away, planning should start now. But what does planning mean in the context of a continuous transaction control (CTC) rollout? What have businesses on the cusp of such a transformation learnt when faced with the same challenge in countries such as Italy, India, Mexico and Spain? And how can businesses leverage those best practices for future CTC rollouts?

We share the points businesses should consider when planning for any CTC rollout, which can be used as a checklist for the France 2023 mandate to help you prepare.

Once you’ve answered the questions above, you’ll be in a good position to both plan the roadmap to ensure compliant processes in time for the entry into force, as well as to estimate the cost and secure the needed funding for the project.

Register for our webinar How to Comply with France’s E-Invoicing Mandate or Get in touch with our experts who can help you prepare.

Norway announced its intentions to introduce a new digital VAT return in late 2020, with an intended launch date of 1 January 2022. Since then, businesses have wondered what this change would mean for them and how IT teams would need to prepare systems to meet this new requirement. Norway has since provided ample guidance so businesses can begin preparations sooner rather than later.

With this new VAT return, the Norwegian Tax Administration (Skatteetaten) seeks to provide simplification in reporting, better administration, and improved compliance.

This new VAT return provides for an additional 11 boxes, increasing the count from 19 to 30 boxes which are based on existing SAF-T codes to allow for more detailed reporting and flexibility. It’s important to note that the obligation to submit a SAF-T file will not change with the introduction of this new VAT return.

This change is for the VAT return only – with the SAF-T codes being re-used and re-purposed to provide additional information. Businesses must still comply with the Norwegian SAF-T mandate where applicable and must also submit this new digital VAT return.

Skatteetaten has created many web pages with detailed information for businesses to look through over the next few months including the following:

Norway is encouraging direct ERP submission of the VAT return where possible. However, the tax authorities have announced that manual upload via the Altinn portal will still be available. Login and authentication of the end user or system is carried out via ID-porten.

Additionally, Norway has provided a method for validation for the VAT return file, which should be tested before submission to increase the probability that the file is accepted by the tax authorities. The validator will validate the content of a tax return and should return a response with any errors, deviations, or warnings. This is done by checking the message format and the composition of the elements in the VAT return.

Businesses should begin preparations for the implementation of this new VAT return, as there will likely be challenges along the way.

In addition to the new VAT return, Norway has also announced plans to implement a sales and purchase report, which is currently in an early proposal stage in review with the Ministry of Finance. The next phase is mandatory public consultation which is when a desired launch date will be set. Skatteetaten notes that implementation time will be considered when determining an introduction date for the report.

Get in touch to find out how we can help your business prepare for Norway’s 2022 Digital VAT Return requirements. Follow us on LinkedIn and Twitter to keep up-to-date with the latest regulatory news and updates.