Several EU Member States have been introducing continuous transaction controls (CTCs), aiming to close their VAT gaps, increase revenue and have more control over the data of their economy. However, the CTC regimes adopted by those countries are far from uniform. So far, Italy is the only country that obtained a derogation from the VAT Directive to introduce mandatory e-invoicing in domestic flows. Other countries, such as Hungary and Spain, instead adopted an e-reporting approach, which avoids the need for a derogation from the European Council as it does not mandate e-invoicing.

These national movements towards CTCs have not passed unnoticed by the European Commission which commissioned a study to assess the current CTC landscape and analyse different scenarios involving new technologies and digitization of business processes. This project is broadly called “VAT in the Digital Age”. It includes the analysis of CTC regimes, the VAT treatment of the platform economy, and the creation of a single EU identification number.

Although the final study is yet to be published, preliminary findings have been discussed in some forums. The study has found that CTCs exist in Europe, with southern and central-eastern Europe at the forefront of local implementations. That also means that the Member States have implemented local flavours of CTCs in a non-uniform and non-standardised way, often creating a burden to multinational companies and cross-border commerce.

One of the study’s goals is to assess the cost-benefit for tax authorities and businesses trading under CTC rules. The study investigates a few approaches, including real-time reporting, mandatory e-invoicing, and periodical reporting (including SAF-T schemes). It is expected that the research will consider EU-wide standards/platforms for CTC models and analyse the possibility of leaving things as they are (but removing the need for the Member States to ask for a derogation before the implementation of mandatory e-invoicing schemes).

The “VAT in the Digital Age” initiative is not the sole CTC project on the EU’s agenda. Italy has also asked the European Council to extend the country’s derogation for its e-invoicing mandate. The ongoing discussion, which includes Italian data estimating an increase in public revenue of more than EUR 2 billion might considerably influence the conclusions of the “VAT in the Digital Age” initiative.

After the study’s publication, the European Commission is expected to open a public consultation to debate the future of CTCs in Europe, a single EU VAT registration, perhaps expanding the One-Stop-Shop (OSS) scheme for transactions and subjects currently out of scope and the VAT treatment of the platform economy. The public consultation is expected to open before the end of this quarter.

Get in touch or download VAT Trends: Toward Continuous Transaction Controls for an essential guide VAT compliance.

As we inch closer to the implementation date of 1 January 2022 for Norway’s new digitized VAT return, let’s take a second look at the details.

Norway announced its intentions to introduce a new digital VAT return in late 2020, with an intended launch date of 1 January 2022. With this update comes the removal of box numbers, which will be replaced by a dynamic list of specifications. The report will also repurpose the Norwegian Standard Tax Codes from the SAF-T financial file to provide more detailed reporting and flexibility. It’s important to note that the obligation to submit a SAF-T file will not change with the introduction of this new VAT return.

This change is for the VAT return only – with the SAF-T codes being re-used and re-purposed to provide additional information. Businesses must still comply with the Norwegian SAF-T mandate where applicable and must also submit this new digital VAT return. With the new VAT return, the Norwegian Tax Administration (Skatteetaten) seeks to simplify reporting, better administration, and improved compliance.

Skatteetaten has created many different web pages with detailed information for businesses to look through over the next few months, including the following:

Norway is encouraging direct ERP submission of the VAT return where possible. However, the tax authorities have announced that manual population via the portal will still be available.

Login and authentication of the end user or system is carried out via the ID porten system. Originally, Norway didn’t allow for XML upload; however, the tax authorities have recently updated their guidance to ensure that XML upload will be accepted. Changing numbers or notes in the uploaded XML file will not be possible, but it will be possible to upload attachments.

Additionally, Norway has provided a method for validation for the VAT return file, which should be tested before submission to increase the probability that the file is accepted by the tax authorities. The validator will validate the content of a tax return and should return a response with any errors, deviations, or warnings. This is done by checking the message format and the composition of the elements in the VAT return.

Please note that Norway is not allowing for any grace period for the submission of this newly designed return.

In addition to the new VAT return, Norway has also announced plans to implement a sales and purchase report by 2024. The proposal is currently in the mandatory public consultation phase, which ends on 26 November 2021.

To find out more about what we believe the future holds, download Trends: Toward Continuous Transaction Controls and follow us on LinkedIn and Twitter to keep up-to-date with the latest regulatory news and updates.

>

Update: 3 January 2024 by Inês Carvalho

After the implementation of Romania’s new B2B e-invoicing regulations, effective January 2024, the country introduced Government Emergency Order No. 115/2023 with last-minute amendments.

We can summarise the key amendments from the new legislation in three categories:

The e-reporting mandate explicitly excludes the following transactions:

From July 2024 onwards, the requirement to issue e-invoices for transactions between established entities persists. The amendment states that in the event of a taxpayer’s failure to generate an electronic invoice, they are obligated to submit it to the RO e-Factura platform within five calendar days.

From July 2024, established entities that fail to comply with the issuance and receipt of e-invoices will receive a fine equal to 15% of the total invoice amount.

Additionally, those who fail to report the invoice which was not issued and automatically transmitted to the RO e-Factura within the additional five calendar days will be fined:

Read our dedicated Romania e-invoicing page for more information on the mandate or VAT Compliance in Romania.

Update: 20 September 2023 by Inês Carvalho

The Romanian Ministry of Finance has published draft legislation proposing new budgetary measures, among which is the implementation of the highly anticipated electronic invoicing mandate.

Even though the draft legislation maintains the January 2024 roll-out date previously approved by the EU Council, it proposes an invoice reporting system to operate in the first six months with the electronic invoicing system (RO e-factura) being fully implemented in July 2024.

Additionally, a three-month grace period – from January 2024 to March 2024 – is foreseen where penalties are not imposed.

For more information see this overview about e-invoicing in Romania.

The first phase of implementation where taxpayers report invoices to the RO e-factura system – instead of issuing the invoices directly through that system – is an addition of the draft law.

This reporting obligation is a transitional measure to help businesses prepare and adapt their systems to the new e-invoicing requirements. Between January and June 2024, the draft legislation also foresees an obligation for the supplier to send the cleared invoice out-of-band to the buyer whenever the latter is not registered with the RO e-factura system.

The scope of the new B2B draft mandate applies to all B2B transactions carried out by established or VAT-registered suppliers deemed to take place in Romania.

Looking to better understand e-invoicing regulations ahead of Romania’s mandate? Our guide can help.

Update: 28 July 2023 by Enis Gencer

The EU Council has approved the proposal from the EU Commission to authorise Romania to introduce mandatory e-invoicing starting from January 2024. The decision was adopted on 25 July and published in the Official Journal of the EU on 27 July.

Romania has been progressing towards implementing a continuous transaction controls (CTC) e-invoicing regime for some time now. The country introduced the e-invoicing requirement for B2B transactions of high-fiscal risk products in December 2021 and B2G transactions in May 2022, both implemented as of July 2022.

In addition to these requirements, Romania aims to make e-invoicing mandatory for all B2B transactions. To this end, the country applied to the European Commission on 14 January 2022, requesting authorisation for a special measure to derogate from articles 218 and 232 of Directive 2006/112/EC, which was granted on 25 July. This measure would allow for the introduction of mandatory electronic invoicing for all transactions carried out between taxable persons established in Romania.

The Romanian authorities will need to make the necessary amendments to local legislation to implement mandatory e-invoicing, following the derogation decision received by the EU Council.

The Romanian tax authority, ANAF, is expected to issue an order within 30 days from the date of the derogation which will define the scope and timeline for the implementation of the mandate. The order will provide more specific details about the upcoming mandate.

Considering the mandate could come into effect as early as January 2024, it’s crucial that taxpayers start preparing their systems for mandatory e-invoicing from now.

Looking for guidance to comply with Romania’s upcoming e-invoicing mandate? Our expert team can help.

Update: 28 July 2023 by Enis Gencer

The EU Council has approved the proposal from the EU Commission to authorise Romania to introduce mandatory e-invoicing starting from January 2024. The decision was adopted on 25 July and published in the Official Journal of the EU on 27 July.

Romania has been progressing towards implementing a continuous transaction controls (CTC) e-invoicing regime for some time now. The country introduced the e-invoicing requirement for B2B transactions of high-fiscal risk products in December 2021 and B2G transactions in May 2022, both implemented as of July 2022.

In addition to these requirements, Romania aims to make e-invoicing mandatory for all B2B transactions. To this end, the country applied to the European Commission on 14 January 2022, requesting authorisation for a special measure to derogate from articles 218 and 232 of Directive 2006/112/EC, which was granted on 25 July. This measure would allow for the introduction of mandatory electronic invoicing for all transactions carried out between taxable persons established in Romania.

The Romanian authorities will need to make the necessary amendments to local legislation to implement mandatory e-invoicing, following the derogation decision received by the EU Council.

The Romanian tax authority, ANAF, is expected to issue an order within 30 days from the date of the derogation which will define the scope and timeline for the implementation of the mandate. The order will provide more specific details about the upcoming mandate.

Considering the mandate could come into effect as early as January 2024, it’s crucial that taxpayers start preparing their systems for mandatory e-invoicing from now.

Looking for guidance to comply with Romania’s upcoming e-invoicing mandate? Our expert team can help.

Update: 24 January 2022 by Enis Gencer

With the most significant VAT gap in the EU (34.9% in 2019), Romania has been moving towards a CTC regime to improve and strengthen VAT collection while combating tax evasion.

The main features of this new e-invoicing system, e-Factura, are described further down in this blog. Here, we’ll take a closer look at the roll-out for B2B transactions and the definition of high-fiscal risk products, as well as the new e-transport system that was introduced through the Government Emergency Ordinance (GEO) no. 130/2021, published in the Official Gazette on 18 December.

According to GEO no. 120/2021 (the legislative act introducing the legal framework of e-Factura), the supplier and the recipient must both be registered with the e-Factura system. The recently published GEO no. 130/2021 establishes an exception for high fiscal risk products and ensures that taxpayers will use the e-Factura system regardless of whether the recipients are registered.

In line with the GEO no. 130/2021, the National Agency for Fiscal Administration has issued an order to clarify which products are considered high fiscal risk products.

The five product categories are as follows:

High fiscal risk products are defined based on the nature of the products, marketing method, traceability of potential tax evasion and degree of taxation in those sectors. Detailed explanations, as well as product codes, can be found in the Annex of GEO no. 130/2021.

The enforcement timeline of this requirement means that businesses that supply these types of products must be ready to comply with the new Romanian e-Factura system as follows:

Another reform that shows the intention of the Romanian authorities to combat tax fraud and evasion is the introduction of an e-transport system.

Taxpayers will be required to declare the movement of goods from one location to another in advance. Once declared, the system will issue a unique number written on the transport documents. Authorities will then verify the declaration on the transport routes.

Moreover, it is stated in the justification letter that the e-transport system will interconnect with the Ministry of Finance’s current systems, Romanian e-invoice, and traffic control, much like similar initiatives in other countries, such as India, Turkey and Brazil.

The introduction of the e-transport system is still pending as the Ministry of Finance has not yet issued the order regarding the application procedure of the system. According to GEO 130/2021, the Ministry of Finance had 30 days to do so after GEO 130/2021 was published in the Official Gazette. However, the deadline expired on the 17 January, and no announcement has been made yet. Therefore, the details of the system are still unknown.

Follow us on LinkedIn and Twitter to keep up-to-date with the latest regulatory news and updates.

Update: 16 November 2021 by Joanna Hysi

In March 2020, Romania launched an e-invoicing pilot program, e-Factura, to streamline the collection of taxes to improve and strengthen the collection of VAT whilst combating tax evasion.

The decision to launch e-Factura was taken after closely monitoring the Italian e-invoicing model and analysing the economic impact and efficiencies that electronic invoicing has had for both B2G and B2B transactions in Italy.

E-Factura is to implement a new e-invoicing system for B2G transactions but also lays the foundation for the extension of the platform for further developments and provides the necessary know-how to develop an e-invoicing system in B2B.

In October, Government Emergency Ordinance (GEO) no. 120/2021 introduced the legal framework for implementing e-Factura, regulating the structure of the Romanian e-invoice process and creating the framework for achieving basic technical specifications of the e-invoice system.

Further documentation regulating the use and operation of e-Factura and technical documentation such as API specifications and draft e-invoice schemas have also been published.

According to published documentation, the B2B e-invoicing process is not expected to differ from the B2G e-invoicing process, whose framework and relevant requirements are defined to a clearer standard.

Taxpayers can expect the same requirements to apply to B2G and B2B e-invoicing. However, certain aspects for B2B e-invoicing must still be clarified, such as the authentication process and requirements for accessing and using the e-invoicing system through the API for taxpayers and their service providers.

The Romanian e-Factura went live as a voluntary system on 6 November 2021, just six months from the announcement of the Ministry of Finance of the roll-out of a new e-invoicing system and only one month after publication of enacting legislation. Suppliers in both B2B and B2G transactions may opt to use this new e-invoicing system and issue their e-invoices in the Romanian structured format through the new system.

The Romanian e-Factura is a clearance system where e-invoices are sent, cleared, and received through the central platform. The structured invoice is issued in XML format and sent to the central platform for validation. The validation checks relate to the compliance of the structured invoice with the schema requirements, the authenticity of the origin regarding the identity of the issuer who is authenticated in the system and the integrity of the invoice content after transmission. An XML invoice that passes validation and is signed by the Ministry of Finance is considered the legal invoice.

The initial implementation timeline must be – by international comparison – considered short for the roll-out of an extensive new CTC system. This could be explained by the fact that the roll-out of the voluntary system is not as disruptive as that of a mandatory system.

If, or when, a mandate is announced or relevant e-invoicing incentives are introduced, a longer implementation timeline is likely to follow to facilitate for taxpayers to comply with the new requirements in time.

Need to ensure compliance with the latest Romania e-Factura requirements? Speak to our team.

Electronic invoicing is rapidly becoming a standard business process. Governments are pushing for the adoption of B2G invoicing to optimize the public procurement process and also to provide a boost to the adoption of e-invoicing between businesses.

Apart from countries that have introduced general e-invoicing mandates to improve fiscal controls – most of which have so far been in Latin America – countries in Europe and some in Asia are looking towards the PEPPOL framework to generate both business process and fiscal benefits through standardization.

PEPPOL was established to simplify interoperability, initially for public procurement transactions, but it is being built upon to encompass fiscal reporting or invoicing ‘clearance’ concepts as well.

As part of harmonizing and digitizing public procurement processes within the EU, governments and other public bodies under Directive 2014/55/EU are required to be able to send and receive electronic invoices in accordance with the European Standard EN-16931.

All EU Member States’ public administrations had to be able to receive e-invoices at least for public procurement transactions either by November 2018 or by April 2019, with the possibility for Member States to extend the deadline by one extra year for sub-central authorities.

Several countries have taken the opportunity to generally mandate B2G electronic invoicing when implementing the Directive 2014/55/EU, so that both the public sector and private sector supplier will be obliged to send invoices electronically in B2G transactions.

Examples of countries that have introduced B2G mandatory e-invoicing are Sweden, Croatia, Estonia, Lithuania and Slovenia, and there is an upcoming mandate in Portugal that will come into force for all companies by January 2022. Finland is aiming for the same effect through a buyer-initiated mandate for the supplier to send e-invoices.

The PEPPOL project was initiated in 2008. One of its main objectives was standardization of the public procurement process in European governments. PEPPOL is a set of artifacts and specifications created to enable cross-border e-procurement, supported by a multi-lateral agreement structure which is owned and maintained by the OpenPEPPOL association.

PEPPOL aims to remove complexity around interoperability, as all parties that use PEPPOL will adhere to the same regulations and technical standards to exchange e-documents. Through the PEPPOL network, companies can exchange electronic procurement documents including e-Orders, e-Advance Shipping Notes, e-Invoices and e-Catalogues via access points based on what is known as a four-corner model – meaning that suppliers and buyers are represented by service providers that process data on their behalf.

While PEPPOL is known to have its initial focus in Europe, it is expanding beyond the EU to Asia and recently has also received more attention in the Americas. Singapore was the first country in Asia and the first outside Europe to establish a PEPPOL Authority, facilitating the framework on a national level, but was soon followed by other countries.

Currently, there are OpenPeppol members in 31 countries. In addition to countries in Europe, these include Australia, Canada, China, Japan, Mexico, New Zealand, Singapore and USA, with Japan being the newest addition.

As explained above, several EU Member States took the opportunity when transposing the Directive 2014/55/EU to make B2G e-invoicing mandatory.

More countries are now following that path:

Developments in B2G e-invoicing can no longer be considered separate from B2B e-invoicing. After all, many companies supply goods or services to public authorities, and investments in complying with government customer requirements under schemes like PEPPOL will drive the use of these same standards and rules in the business-to-business sector.

This also means that initiatives towards business-to-business electronic invoicing as a way for tax administrations to receive VAT-relevant data in real-time or near-real-time are increasingly influenced by concepts from the public procurement world.

This spillover goes well beyond conceptual inspiration. In Italy, for example, support for mandatory e-invoicing for VAT control purposes in 2019 was built on a massive data processing platform that was initially designed to facilitate public procurement. France and Poland are far down the path of similar architectures for their continuous transaction controls plans.

As PEPPOL becomes more popular as a standard to make country-specific public procurement methodologies more easily accessible for suppliers abroad, its concepts will increasingly penetrate the broader worlds of electronic invoicing, electronic trade and fiscal compliance.

Need to ensure compliance with the latest e-invoicing regulations? Get in touch with our tax experts.

Update: 25 June 2024 by Dilara İnal

The German Ministry of Finance (MoF) released a draft guideline on 13 June 2024, detailing the upcoming B2B e-invoicing mandate which will roll out on 1 January 2025.

Although the current law only obliges taxpayers to issue and receive e-invoices for domestic B2B transactions, the MoF plans to introduce an e-reporting system for invoice details at a later stage, with no set date.

The highlights from the guidelines are:

The final version of the guideline is expected by Q4 2024.

Update: 26 March 2024 by Dilara İnal

The German parliament passed the Growth Opportunities Act (Wachstumschancengesetz – the Act) concerning various tax matters on 22 March 2024, including a nationwide B2B electronic invoicing mandate.

The Act was originally scheduled for a vote at the end of 2023, with enforcement planned for January 2024. However, the lack of consensus between the Bundestag and Bundesrat – lower and upper houses of the parliament, respectively – in various provisions of the Act delayed its finalisation.

The Mediation Committee of the Bundestag and Bundesrat concluded its negotiations about the Act on 21 February 2024, and the Bundestag approved the amended text on 23 February. The Bundesrat’s vote on 22 March completed the parliamentary process.

The implementation timeline for this mandate has been confirmed as follows:

Mandatory receipt of e-invoices for domestic B2B transactions will be required for all businesses. Additionally, businesses will have the option to issue e-invoices that are compliant with the approved syntaxes based on CEN 16931 voluntarily, without the Buyer’s consent.

Following this parliamentary approval, the Act will be signed by the President and subsequently published in the official gazette.

Acceptable invoice formats to issue in following years:

| Domestic B2B Invoices | 2024 | 2025 | 2026 | 2027 | 2028 |

| Paper Invoices |

Allowed |

Prohibited for large taxpayers |

Prohibited for all |

||

| E-invoices in EN 16931 format |

Allowed with Buyer’s consent |

Allowed |

Mandatory for large taxpayers |

Mandatory for all |

|

| EDI invoice not EN 16931 format |

Allowed with Buyer’s consent |

Allowed if are interoperable with the CEN, if the required information can be extracted into CEN | |||

| Other invoices in e-form (e.g. PDF, JPEG) |

Allowed with Buyer’s consent |

Allowed if are interoperable with the CEN, if the required information can be extracted into CEN** Please note that exchange on EDI is permitted if the e-invoice aligns with European standards. |

|||

Is your organization unprepared for the upcoming mandate? Our expert team can help.

Update: 6 November 2023 by Dilara İnal

In October 2023, The Federal Ministry of Finance (MoF) released additional information regarding electronic invoicing, one of the proposed tax measures included in the Growth Opportunities Act.

If the MoF’s proposal, with the details provided in the preceding updates, becomes law, the following will be applicable:

Besides MoF clarifications, the upper house of the German Federal Parliament, Bundesrat, addressed the Act during its session on 20 October. While the Bundesrat supports the introduction of mandatory e-invoicing, it has proposed a two-year delay so the mandatory receipt of electronic invoices commences on 1 January 2027.

In the next steps of the process, the lower house of the Parliament, Bundestag, is expected to vote on the Growth Opportunities Act in mid-November. The upper house’s vote should take place in mid-December.

Looking for more information on the global adoption of e-invoicing? Read our definitive E-invoicing guide.

Update: 20 September 2023 by Dilara İnal:

On 30 August, the German Federal Government approved the draft act known as the “Growth Opportunities Act,”. The act consists of several provisions on different tax matters, including the introduction of a nationwide B2B e-invoicing mandate.

Key dates for implementation of the mandate include:

The draft bill approved by the government does not change the previously communicated framework, however it extends the voluntary phase by one year. The voluntary phase will last until January 2027 for small companies with annual turnover of 800,000 EUR or less in 2025.

The Federal Parliament and the Federal Council are expected to give their approval to this reform by the end of 2023.

Looking for additional guidance on invoicing in Germany? Speak with our team of experts.

Update: 4 August 2023 by Dilara İnal

The German Federal Ministry of Finance (the Ministry) shared the draft “Growth Opportunities Act” with significant German business associations on 14 July 2023. This act introduces amendments to VAT law to implement mandatory e-invoicing, along with other national and international tax-related proposals.

Currently, issuing an electronic invoice requires the buyer’s consent. Proposed amendments will change this, with invoices for transactions between German resident taxpayers – known as domestic B2B transactions – required to be electronic.

The act also introduces a new definition for e-invoices. An electronic invoice is defined as an invoice issued, transmitted and received in a structured electronic format that enables electronic processing. An e-invoice must also comply with the eInvoicing standard of the European Committee for Standardization (CEN), EN 16931.

The Ministry previously shared its plan to roll out mandatory e-invoicing as of January 2025. This date remains the same in the amendment proposals, with transitional measures giving taxpayers some time and flexibility to comply with the new requirements:

Even though this act does not include any provisions for a transaction-based reporting system, it notes that such a reporting system for B2B sales will be introduced later.

The European Council authorised Germany to introduce special measures regarding mandatory electronic invoicing with its decision dated 25 July 2023.

Germany received the derogation from the VAT Directive from 1 January 2025 to 31 December 2027 or, if an EU directive is adopted earlier than planned, until the national transposition of the VAT in the Digital Age (ViDA) directive into German law.

Looking for additional guidance on invoicing in Germany? Speak with our team of experts.

Update: 21 April 2023 by Anna Norden

The German Federal Ministry of Finance sent a discussion proposal for the introduction of mandatory B2B e-invoicing in Germany on 17 April to significant German business associations.

The business associations are requested to provide their opinion on matters such as the following by 8 May:

The proposed e-invoicing mandate is a step toward implementing a real-time transaction-based reporting system for creating, verifying and forwarding e-invoices. This system is not part of the current proposal, but – as this is directly related to an e-invoice mandate – the ideas for such a system are laid out at a high level by the Ministry of Finance.

The final aims to provide a uniform electronic transaction-based reporting system for national and cross-border B2B transactions. The invoice exchange would be done via a central or private platform.

No verification of the full invoice content would be performed or interruption of forwarding of the invoice – however, the issuer’s platform would check (“Plausibilitätsprüfungen”) that all mandatory fields are present, whether structure and syntax are EN-compliant and so on.

The reporting of the invoice would be in real-time at the same time as the invoice is sent so that the supplier would not have to initiate two transactions.

The Ministry of Finance states the aim is for the new system to be aligned with ViDA but that Germany counts on having to use a derogation from the provisions of the VAT Directive to introduce the e-invoice mandate, should ViDA not be adopted in time.

While many have speculated around Germany going down the path of the Italian e-invoicing system, the message from the Ministry of Finance seems rather to be that the cues are taken from the French system, with the use of a centralised platform complemented with private service providers who serve to channel the invoices.

Need to discuss how Germany’s proposal to introduce continuous transaction controls could affect your business? Speak to our tax experts.

Update: 3 November 2021 by Joanna Hysi

There’s been increased discussion among different institutions about the introduction of continuous transaction controls (CTCs) in Germany to combat tax fraud and boost the competitiveness of the German market in Europe.

Proponents of the introduction of CTCs in Germany include, among others: the parliamentary group of the business-friendly Free Democratic Party (FDP), the German Association for Electronic Invoicing (VeR) and an independent judiciary body, the German Bundesrechnungshof (Federal Audit Office).

Recently, we’ve seen this topic included in tax policy negotiations of the coalition partners that emerged from the recent German government elections (the Social Democratic Party (SPD), FDP, and the Green Party).

While the discussions remain at a conceptual level, the new potential coalition parties display political will for reform in this area.

Specifically, the German Bundesrechnungshof proposed to the Ministry of Finance a real-time reporting system leveraging blockchain technology as an efficient system to combat VAT fraud. However, their proposal wasn’t accepted on the grounds that a cost-benefit analysis is required before such measures are proposed and implemented.

As part of a parliamentary process the FDP called for “an electronic reporting system comparable to the Italian SDI to be introduced nationwide as quickly as possible, for the creation and testing and forwarding of invoices”. The leading German industry association, the VeR, welcomed this proposal recognising its numerous advantages to companies and the German economy.

A VeR study on whether the Italian model can be used as a blueprint for Europe explains that although it doesn’t seem to have contributed significantly to reducing Italy’s VAT gap, the advantages of e-invoicing to companies and the Italian economy are convincing. It concludes that the Italian clearance system can serve as a model for the digitization of VAT in Germany, if not in Europe. In addition, the VeR experts offer their knowledge to develop such a CTC system in Germany.

It seems that the idea of introducing a CTC system in Germany – following in the footsteps of fellow Member States like Italy, France and Poland – is gaining traction and might not be far from becoming reality if the coalition partners indeed manage to reach a coalition agreement to succeed the currently ruling party.

To find out more about what we believe the future holds, download VAT Trends: Toward Continuous Transaction Controls. Follow us on LinkedIn and Twitter to keep up-to-date with regulatory news and updates.

On 1 July 2021 the EU E-Commerce VAT Package was introduced. The package replaced existing distance-selling rules and extended the Mini One Stop Shop (MOSS) into a wider-ranging One Stop Shop (OSS).

The implementation of the EU E-Commerce VAT Package was designed to simplify the VAT reporting requirements for sellers and improve the tax take for Member States.

Two months in: we take a look at how it’s going.

There were unfortunately some initial delays and teething problems when the EU E-Commerce VAT Package was introduced, which is to be expected with the adoption of such a significant new system, but as with any new scheme these can be resolved over time.

Some examples include:

There are also issues associated with the import of the goods.

Some Member States disallow the import of certain categories of goods due to local restrictions e.g. foodstuffs, plants etc.

It’s sometimes unclear if freight forwarders have used IOSS or not and this could lead to repeated errors of underpayment or overpayment of VAT.

Some non-EU vendors are trying to avoid an IOSS registration by stating that the customer is the importer of record. Such practice happened before the introduction of IOSS but not always at the same level as it is now – and was not always spotted or queried.

However, since the introduction of the IOSS, some tax authorities, including Germany, are questioning such an approach on the grounds that the carrier who imports the goods is acting for the non-EU vendor and is not known by the buyer.

This means import VAT is due by the vendor who must then also charge German VAT. For cases that have already occurred there may be an issue with recovery of the import VAT, as the evidence required to support the deduction will have been issued in the wrong name (consumer).

It’s still early days for the EU VAT E-Commerce Package and initial teething problems are to be expected. One thing is certain, navigating these new VAT schemes is complex. Sovos is here to help and we’ll keep you updated on the latest regulatory changes.

Join our latest webinar on September 22, 2021 to learn how you can use the Import One-Stop Shop (IOSS) to simplify your EU VAT compliance and unlock the full potential of the EU e-commerce market.

Still have questions about OSS and IOSS? Download our e-book to understand the implications of the 2021 EU e-commerce VAT package and ensure your business is ready by 1 July 2021 for the significant changes ahead

Back in 2019, Portugal passed a mini e-invoicing reform consolidating the country’s framework around SAF-T reporting and certified billing software.

Since then, a lot has happened: non-resident companies were brought into the scope of e-invoicing requirements, deadlines have been postponed due to Covid, and new regulations were published. This blog summarises the latest and upcoming changes.

Introduced in 2019, the de facto implementation of the QR code requirement was delayed, and is now expected to be fully implemented by taxpayers in January 2022. A QR code should be included in all invoices. Technical specifications about the content and placement of the code in the invoice are available on the tax authority’s website.

The ATCUD is a unique ID number to be included in invoices and is part of the content of the QR code. The ATCUD is a number with the following format ‘ATCUD:Validation Code-Sequential number’.

To obtain the first part of the ATCUD – the so-called ‘validation code’ -, taxpayers must communicate the document series to the tax authority along with information such as type of document, first document number of the series, etc.

In return, the tax authority will deliver a validation code. The validation code will be valid for the whole document series for at least a fiscal year. The second part of the ATCUD – the ‘sequential number’ – is a sequential number within the document series.

This month, the Portuguese tax authority published technical specifications for obtaining the validation code, creating a new web service. To access this web service, a specific certificate obtained from the tax authority is required and can be assigned to taxpayers or software service providers.

In addition, the tax authority has created a standard list of document classes and types, enabling the communication of document types in a structured format.

An ATCUD will be required in all invoices from January 2022. To be ready for the deadline, taxpayers must get the series’ validation codes during the last half of 2021 to apply in invoices issued in the beginning of 2022.

In April this year, Portugal clarified that non-resident companies with a Portuguese VAT registration should comply with domestic VAT rules. This includes the use of certified billing software for invoice creation, among others. These companies must also ensure integrity and authenticity of e-invoices. In Portugal, integrity and authenticity of invoices are presumed with the use of a qualified electronic signature or seal, or use of EDI with contracted security measures.

Consequently, since 1 July 2021, non-established but VAT registered companies must adopt certified billing software to comply with the Portuguese law as required by Law-Decree 28/2019, Decision 404/2020-XXII, and Circular 30234/2021.

The Portuguese e-invoicing mandate for business-to-government transactions includes a format requirement attached to specific transmission methods. In other words, invoices to the public administration must be issued electronically in the CIUS-PT format and transmitted through one of the web services made available by the public administration.

Initially, a phased roll-out started in January 2021, obliging large companies to issue e-invoices to public buyers. In July, the subjective scope was enlarged to include small and medium-sized businesses. The last step is to include microenterprises by January 2022.

Due to the Covid pandemic, Portugal established a grace period that has been renewed several times, whereby PDF invoices would be accepted by the public administration. Currently, the grace period runs until 31 December 2021, meaning that, in practice, all suppliers of the public administration, regardless of their size, should comply with the e-invoicing rules in public procurement by 1 January 2022.

Need to ensure compliance with the latest e-invoicing regulations? Get in touch with our tax experts at Sovos.

In our last look at Romania SAF-T, we detailed the technical specifications released from Romania’s tax authority. Since then, additional guidance has been released including an official name for the SAF-T submission: D406.

To alleviate taxpayer concerns due to the complexity of the report and difficulties with extraction, the tax authorities are introducing a voluntary testing period which is due to begin in the coming weeks. During this period, taxpayers may submit what is known as D406T which will contain test data that the authorities will not use in the future for audit purposes.

The Romanian SAF-T, D406, is based on the OECD schema version 2.0 which contains five sections:

The submission deadlines are as follows:

Taxpayers must submit sections of D406 monthly or quarterly, following the applicable tax period for VAT return submission.

For the first report, tax authorities have announced a grace period for the first three months of submission. This is from the date when the deposit obligation becomes effective for that taxpayer, where non-filing or incorrect filing will not result in penalization if correct submissions are submitted once the grace period ends.

The D406 must be submitted electronically in PDF format, with an XML attachment and electronic signature. The size of the two files must not exceed 500 MB. If the file is larger than the maximum limit, the portal will not accept it and the file must be divided into segments according to details set out in the Romanian guidance.

The tax authorities have indicated that, should a taxpayer find errors in the original submission, a corrective statement may be submitted to rectify these errors. The taxpayer should submit a second full corrected file to replace the original file that contains errors. If a taxpayer submits a second D406 for the same period, it is automatically considered a corrective statement.

Need to ensure compliance with the latest Romania SAF-T requirements? Speak to our team. Follow us on LinkedIn and Twitter to keep up-to-date with the latest regulatory news and updates or see this overview on VAT Compliance in Romania.

Welcome to our Q&A two-part blog series on the French e-invoicing and e-reporting mandate, which comes into effect 2023-2025. That sounds far away but businesses must start preparing now if they are to comply.

The Sovos compliance team has returned to answer some of your most pressing questions asked during our webinar.

We have outlined the new mandate, e-invoicing specifically, and questions around this topic in our first blog post.

This blog will look at the other side of the mandate – e-reporting obligations. These will apply to B2C and cross-border B2B transactions in France, which must be periodically reported.

First let’s look at common questions around payments e-reporting.

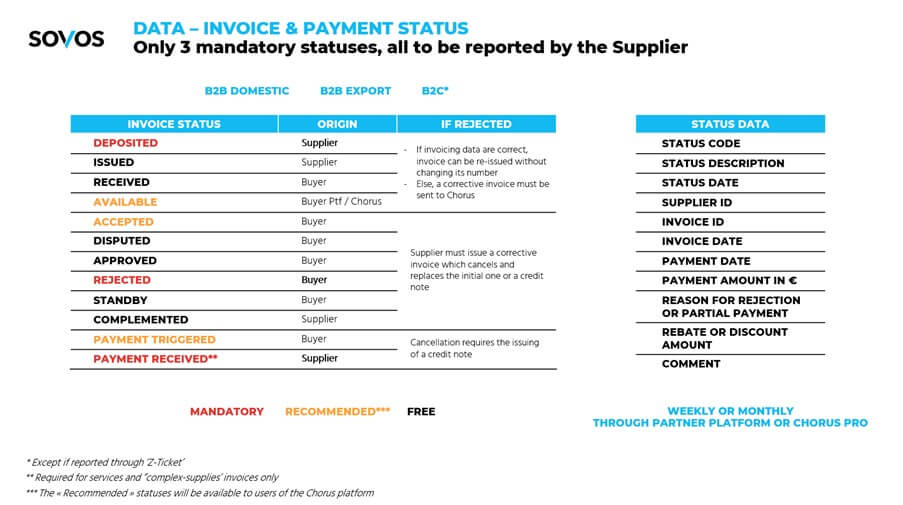

What are the invoice and payment statuses to be reported?

Here is a slide from our webinar showing invoice statuses, whether these are mandatory, recommended, or free, origins, action to take if rejected, status data, and when it needs to be reported:

Who is responsible for payment e-reporting? The buyer, the seller, or both?

It was initially rumoured to be both on the buyer and the seller side, but the latest information from DGFIP clearly states that it will be the responsibility of the seller to report the invoice status, and, if applicable, its payment status.

Some further clarification is needed though since the seller is dependent on the buyer’s response on some status (e.g. ‘invoice rejected’).

Your e-invoicing and e-reporting project cannot be done in isolation. This is a significant project with many dependencies that involve external third parties.

There will be one or, in most likelihood, several third parties in the middle of the transaction chain. This will include Chorus Pro, chosen by the French government as the official and obligatory platform for businesses to issue e-invoices to public administrations.

This section covers common questions on partner platform certification requirements.

Is there a list of official validated partner platforms?

The 13 July 2021 DGFIP workshop dedicated to this matter highlighted that there would be a registration process for third-party platforms, as well as taxpayers who would want to run their own platform.

The registration process will consist of two phases:

Phase 1. A prior selection by the tax authorities based on the general profile of the candidate (e.g. are they up to date in their own tax payment duties?) and the services they propose;

Phase 2. Within 12 months after registration, an independent audit would have to performed that demonstrates that the platform meets the DGFIP requirements, such as:

<liPerforming the control and mapping activities (extraction of invoicing data for both e-invoicing and e-reporting, certain invoice validation checks – mandatory fields, check sums, Customer ID verification – mapping to and from a minimum set of mandatory formats, compliance with GDPR, etc)

A few other key points to note are:

What is the current expectation on when exact required fields with be supplied by the government (invoice specs with all required fields and values)?

Excel files are available as a draft document at a very detailed level which Sovos can provide on request. The final specs should be known by the end of September 2021.

Still have questions about e-reporting? Access our webinar on-demand for more information and advice on how to comply.

In our recent webinar, Sovos covered the new French e-invoicing and e-reporting mandate, and what this means for businesses and their tax obligations.

We are witnessing a global move towards Continuous Transaction Controls (CTCs), where tax authorities are demanding transactional data in real-time or near real-time, affecting e-invoicing and e-reporting obligations.

As such, from 2023, France will implement a mandatory B2B e-invoicing clearance and e-reporting obligation in an effort to increase tax efficiency, cut costs, and fight fraud.

The pace towards this mandate has been accelerating lately with the adoption of the Finance law for 2021, followed by a number of workshops organised by the Ministry of Finance — namely the Direction Générale des Finances Publiques (DGFIP).

In the first of two blogs on the mandate, we answer some of your most pressing questions asked during our webinar.

In part one, we focus on setting the scene in terms of scope, and cover questions around e-invoicing specifically, invoicing file formats, processes and controls, and archiving.

The second blog covers questions around e-reporting obligations.

In this section, we answer questions on the scope of the regulation, such as which companies must comply with the mandate and how.

Are non-resident companies (foreign companies with only a French VAT-registration) obliged to fulfil this new regulation? Are foreign legal entities with a French VAT number in scope?

The Budget Laws for 2020 and 2021 introduced the CTC scheme from a legal perspective. Both include “persons subject to VAT” in the scope.

VAT registration is a strong indication that a company is subject to VAT, but classification as a VAT “taxable person” also depends on other factors.

Therefore, it is not as simple as just looking at whether a company has a local VAT registration, to decide whether it is subject to VAT and therefore targeted by the mentioned budget laws.

However, the scope cannot be unilaterally decided by France as the French CTC scheme is dependent on a derogation from the EU Council.

As a comparison, Italy initially included all taxable persons in the scope of its e-invoicing clearance mandate, including those with a mere VAT registration but no establishment. But in this case, the EU Council limited the scope (of its derogation) to persons established in Italy.

From an e-invoicing perspective, we can therefore expect that France will need to follow the Italian path (due to its reliance on a derogation from the EU Council), limiting the scope to established persons.

DGFIP has however suggested that companies that are non-established but VAT registered will be in scope of the reporting obligation.

Is import of goods in the scope of e-reporting? What about import of services?

Only imports (supplies from outside of the EU) of services are in the scope of the current proposal.

In this section, we discuss permitted e-invoice formats.

The fact that the new regime creates a specific process for domestic B2B e-invoicing does not change the need for businesses to demonstrate the integrity and authenticity of each invoice.

This can be done through one of the 3 legal methods defined by the existing regulations:

To ensure there’s no impact of the reform on integrity and authenticity demonstration methods, one can still apply any of them.

However, with the new regime, e-invoicing data sent to the DGFIP does need to be in a structured format.

Will digital signatures be required?

Digital signatures are not strictly required today and will not be strictly required in the new scheme. Integrity and authenticity will still need to be ensured though, irrespective of invoice format, as is the case today.

The options remain the same; use of digital signatures, use of EDI with security measures, or the BCAT option whereby the audit trail should prove the transaction and its authenticity and integrity.

Are PDF and XML invoice file formats still possible to receive from 2023-2025?

The legal invoice format can be anything, as long as the supplier and buyer agree on it and the integrity and authenticity are guaranteed. Also, a human readable version (normally a PDF) is required upon audit as part of the general EU requirements.

What e-invoicing formats are permitted?

This is not fully defined yet, but DGFIP has indicated the following syntax, based on the EN16931 standard:

Those formats would apply to:

In this section, we answer questions around the processes for sending and receiving e-invoices, what information they need to include, and the Chorus Pro platform.

Will the e-invoice need to be sent real-time?

Yes, it can be considered a “real-time clearance system”. As part of the e-invoicing obligation, the reporting of mandatory data to the tax authorities and the issuance of the original invoice to the buyer by the supplier’s partner platform should happen right after receiving the invoicing data from the supplier.

If the invoice doesn’t have all the mandatory information like the SIRET number of a customer, will the Chorus Pro platform clear it?

Will Chorus Pro also be validating the VAT rates used?

No, or at least not on the fly when submitting the invoicing data to Chorus Pro. Our understanding is that those verifications will be done by the tax authorities after the fact, using data analytics / AI algorithms.

Are there common data, connection and bridges with the current SAF-T?

The French version of SAF-T (FEC) must still be available on demand from the tax authorities.

In this section, we answer questions around compliant archiving of e-invoices.

Does the Chorus Pro/Tax Authority portal provide a compliant electronic archive for AP/AR invoices in France?

Yes. However, in our experience, even though a tax authority’s archiving solution would be available for taxable persons, few larger companies choose to solely rely on it for evidence purposes and instead continue to use their compliant internal or third-party archiving solutions.

This decision is ultimately based on the fact that the tax authority’s archiving solution poses a conflict of interest: it is maintained by the tax authority, which, from a legal perspective, is not an independent party but rather the counterparty in a fiscal claim.

In fact, from discussions with many experts and customers over that past year, we see that the market request for third-party archiving services is even stronger after the introduction of clearance, especially as customers see a need to store not only the invoice but also response messages from the CTC portal to further maintain evidence of compliance.

Still have questions about the e-invoicing mandate? Access our webinar on-demand for more information and advice on how to comply.

In the “Statement on a Two-Pillar Solution to Address the Tax Challenges Arising From the Digitalization of the Economy” issued on 1 July 2021, members of the G20 Inclusive Framework on Base Erosion and Profit Shifting (“BEPS”) have agreed upon a framework to move forward with a global tax reform deal.

This will address the tax challenges of an increasingly digital worldwide economy. As of 9 July 2021, 132 of the 139 OECD/G20 member jurisdictions have agreed to the Inclusive Framework on BEPS.

Pillar 1

Pillar 1 gives a new taxing right, Amount A, to market countries to ensure companies pay tax on a portion of residual profits earned from activities in those jurisdictions, regardless of physical presence. Pillar 1 will apply to multinational enterprises (“MNEs”) with global turnover above 20 billion euros and profitability above 10%.

There will be a new nexus rule permitting allocation of Amount A to a market jurisdiction when the in-scope multinational enterprise derives at least 1 million euros in revenue from that jurisdiction. For jurisdictions with a GDP less than 40 billion euros, the nexus will instead be set at 250,000 euros.

The “special purpose nexus rule” determines if a jurisdiction qualifies for the Amount A allocation. Furthermore, countries have agreed on an allocation of 20-30% of in-scope MNE residual profits to market jurisdictions, with nexus using a revenue-based allocation key.

Revenue will be sourced to the end market jurisdictions where goods or services are consumed, with detailed source rules still to come.

More details on segmentation are still in the works, as is the final design of a marketing and distribution profits safe harbour that will cap the residual profits allowed to the market jurisdiction through Amount A.

Lastly, countries have agreed to streamline and simplify Amount B with a particular focus on the needs of low-capacity countries. The finalised details are expected to be completed by the end of 2022.

Pillar 2

Pillar 2 consists of Global anti-Base Erosion (“GloBE”) Rules that will ensure MNEs that meet the 750 million euros threshold pay a minimum tax rate of at least 15%. The GloBE Rules consist of an Income Inclusion Rule and an Undertaxed Payment Rule, the latter of which still needs to be finalised.

Pillar 2 also includes a Subject to tax rule, which is a treaty-based rule, allowing source jurisdictions to impose limited source taxation on certain related party payments subject to tax below a minimum rate. The rate will range from 7.5 to 9 percent.

There is currently a commitment to continue discussion, in order to finalise the design elements of the plan within the agreed framework by October 2021. Inclusive Framework members will agree and release an implementation plan.

The current timeline is that the multilateral instrument through which Amount A is implemented will be developed and opened for signature in 2022, with Amount A coming into effect in 2021. Similarly, Pillar Two should be brought into law in 2022, to be effective in 2023.

Although the key components of the Two-Pillar Solution have been agreed upon, a detailed implementation plan that includes resolving remaining issues is still to come.

As many countries could be implementing these changes in the near future, it is important for businesses active in the digital economy to carefully track and understand the developments surrounding the OECD/G20 Base Erosion and Profit Shifting Project.

Need to ensure compliance with the latest e-document regulations? Get in touch with our tax experts.

Intrastat is a reporting regime relating to the intra-community trade of goods within the EU.

Under Regulation (EC) No. 638/2004, VAT taxpayers who are making intra-community sales and purchases of goods are required to complete Intrastat declarations when the reporting threshold is breached.

Intrastat declarations must be completed in both the country of dispatch (by the seller) and the country of arrival (by the purchaser). The format and data elements of Intrastat declarations vary from country to country, though some data elements are required in all Member States. Reporting thresholds also vary by Member State.

In an effort to improve data collection and ease the administrative burden on businesses an ‘Intrastat Modernisation’ project was launched in 2017. As a result of this project Regulation (EU) 2019/2152 (the Regulation on European business statistics) was adopted.

The practical effects of these changes are two-fold:

Currently Member States are required to collect the following information as part of Intrastat:

To ease compliance burdens on small businesses, EU Member States are allowed to set thresholds, under which businesses are relieved of their obligations to complete Intrastat. Thresholds are set annually by Member States, and threshold amounts for arrivals and dispatches are set separately.

Under the current regulations, Member States cannot set thresholds at a level that results in less than 97% of dispatches from the Member State being reported and cannot set thresholds at a level that results in less than 93% of intra-community arrivals to the Member State being reported.

Under current regulations Member States are allowed to let certain small businesses report simplified information, so long as the value of trade subject to simplified reporting does not exceed 6% of total trade.

Under the upcoming new regulation, Member States need only ensure that 95% of dispatches are reported and the exchange of data on intra-community arrivals between Member States is optional.

Need to ensure compliance with the latest Intrastat requirements? Get in touch with our tax experts.

Progress has been made in the roll-out of the Polish CTC (continuous transaction control) system, Krajowy System of e-Faktur. Earlier this year, the Ministry of Finance published a draft act, which is still awaiting adoption by parliament to become law. Draft e-invoice specifications have been released and there has been a public consultation on the CTC system.

In June, the Ministry of Finance announced it had reviewed all comments submitted by the public and Polish ministers on the CTC system and decided to take the following actions:

In the announcement, the Minister outlined the benefits of adopting the CTC system for taxpayers. These include: quicker VAT refunds; security of the stored invoice in the tax authority’s database until the end of the mandatory storage period; certainty about the invoice delivery to the recipient through the CTC platform and therefore quicker invoice payments; automation of the invoice processing and exchange due to the adoption of a standardized e-invoice format.

In addition, as a result of the new e-invoicing rules upcoming changes in the SLIM VAT 2 package will trigger further relief measures, e.g. around the handling of duplicates and corrective invoices.

The Polish authorities are making good progress in the implementation of the Krajowy System e-Faktur. It is positive to see that the public consultation has proven useful in defining next steps and the authorities’ intent for transparency and timely documentation will hopefully continue throughout the entire CTC roll-out.

To find out more about what we believe the future holds, download Trends: Towards Continuous Transaction Controls.

For more information see this overview about e-invoicing in Poland, Poland SAF-T or VAT Compliance in Poland.

Moving goods from one place to another is a quintessential part of business. Manufacturers, wholesalers, transporters, retailers and consumers all need to carefully orchestrate the shipping and handling of raw materials, parts, equipment, finished goods and other products to keep business flowing. This supply chain harmony is what makes production and trade possible in society.

In Canada, the United States and most European countries, tax administrations don’t intervene much in these trade processes. Until recently, the same could be said about most countries of Latin America. But, with the rise and expansion of electronic invoicing mandates in the region, this is rapidly changing.

Most governments with mature e-invoicing mandates are now recognizing that these mechanisms and government platforms can be used as vehicles to understand where, what, how and when goods are being moved. The traditional electronic invoice, is no longer enough – and tax authorities are requiring businesses to report goods movements in real-time.

The implications are serious too. Goods moved on public roads without those documents are very likely to be seized by the authorities, and the owners and transporters will be subject to fines and other sanctions.

The country with the most sophisticated system in place is arguably Brazil. The MDF-e (or Manifesto Eletrônico de Documentos Fiscais) is a mandatory document required by the tax administration in order to audit the movement of goods in Brazil.

This purely digital document combines the information of an electronic invoice (NF-e) and the electronic documents that hauling companies issue to their clients (CT-e). This system became mandatory in 2014 and has since been expanded and modernized with a vast grid of electronic sensors and transponders placed in the public highways of Brazil, intended to ensure that every truck moving goods already has the corresponding MDF-e, NF-e and CT-e. In most cases, the authorities don’t need to stop the trucks to verify the existence of the document.

Mexico recently issued a new resolution requiring taxpayers delivering goods, or simply redistributing them, to have the corresponding authorization from the tax administration (SAT). Products delivered by road, rail, air or waterways need to have what is known as the CFDI with the Supplement of Carta Porte.

CFDI is the acronym for an electronic invoice in Mexico. That supplement of Carta Porte is a new attachment to the electronic invoice of transfer (Traslado) issued by the owners delivering products or to the CFDI of Income (Ingresos) issued by the hauling companies. Carta Porte will provide all the details about the goods being transported, the truck or other means being used, the time of delivery, route, destination, purchaser, transporter and other information. This new mandate will become effective on 30 September 2021. As is in Brazil, noncompliance with this mandate will result in hefty penalties.

Chile also has a mandate requiring the delivery of goods to be pre-authorized by the tax administration. These tax authorized documents are locally known as Guias de Despacho (or dispatch guides) and since January 2020 they can only be issued in an electronic format.

There are some exceptions where the dispatch guide can be issued temporarily on a paper format by certain taxpayers. Also, in cases of contingency, taxpayers may be authorized to issue paper versions of the guide; however, that will not exempt the issuer of regularizing the process once the contingency is complete.

The content of the dispatch guide will vary depending on who issues it and the purpose of the delivery (sales, consignment, returns, exports, internal transfers etc.) but in general, delivery of goods in Chile without the authorized dispatch guide will be subject to penalties from the tax administration (SII).

Argentina has a federal level VAT and a provincial level gross revenue tax. To control tax evasion, both levels of governments exercise certain levels of control in the process of dispatching goods within their jurisdictions.

The tax authority’s system for controlling the flow of goods in public ways is not as encompassing as in Brazil, Chile and Mexico, but it is getting closer. Only the provinces of Buenos Aires, Santa Fe and Mendoza, plus the City of Buenos Aires, require authorization from the fiscal authority to move goods that originated in, or are destined to, their jurisdictions. For that, they require the COT (or Transport Operations Code) where all the data related to the products, means of transport and other information is included once the authorization is provided. The provinces of Salta, Rio Negro and Entre Rios are working on similar regulations.

At federal level, the AFIP (Federal tax administration) only requires pre-authorization for the delivery of certain products such as meat and cereals. But at this level too, the regulatory environment is changing.

The AFIP, along with the Ministry of Agriculture and the Ministry of Transportation have issued a joint resolution 5017/2021 that mandates the use of a digital bill of lading (Carta Porte Electronica) whenever there is a transfer of agricultural products on public roads in Argentina. This change will become effective on 1 November 2021. In 2022, this federal requirement may expand to other products.

The requirement of authorization for moving goods in LatAm is not limited to the largest economies of the region. Smaller countries with electronic invoicing systems have expanded, or are in the process of expanding their mandates to require taxpayers to inform the tax authority, before goods are moved as result of a sale or any other internal distribution.

For instance, Peru requires the Guias de Remision from taxpayers before they start the delivery of their products. This electronic document should be informed to and authorized by the tax administration (SUNAT) using the digital format established for that purpose and will include all the information about the product delivered, issuer, recipient, means of transport, dates and more.

Uruguay has the ‘e-Remitos’ which is an electronic document authorized by the tax administration (DGI). It is required for any physical movement of goods in Uruguay. As in other countries, this document will provide all the information about the goods being transported, the means used, the issuer, the recipient and additional data. It is electronically delivered and authorized by the tax administration using the XML schemas established for that purpose.

Lastly, in Ecuador the tax administration (SRI) requires the ‘Guias de Remision’ (Delivery Guide) for any goods to be transported legally inside the country. As the infrastructure to support the electronic invoice is not fully developed in Ecuador, in some cases the tax administration allows the taxpayer to comply with this part of the mandate by having the electronic invoice issued by the retailer delivering the goods to his clients. Even though Colombia and Costa Rica do not require a separate electronic document to authorize the transport of goods, it is expected that in the future, this requirement will come into effect, mirroring what has happened in many other countries of the region.

The common element of all these mandates in Latin America, is that all of them are closely knitted to the electronic invoicing system imposed in each country. They are basically seen as another module of the electronic invoice system where information regarding goods being transported by public roads, waterways, by rail or air should be submitted to the tax administration, via the XML schemas established for that purpose.

Tax administrations in the region are actively enhancing their systems to ensure that movements of goods are properly controlled in real time. In some cases, tax administrations have provided online solutions aimed at taxpayers with small numbers of deliveries. But for all other taxpayers, a self-deployed solution is required.

Enforcement of the mandate is made not only by the tax administration, but also by the police and the public roads authorities, both of which routinely seize goods for non- compliance. Since these mandates have proven to be successful to control tax avoidance and smuggling, it’s safe to say that the Remitos, Dispatch Guides, Carta Porte or COTs are here to stay for good and taxpayers doing business in Latin America have no option but to comply with this new regulatory requirement.

To find out more about what we believe the future holds, download VAT Trends: Toward Continuous Transaction Controls. Follow us on LinkedIn and Twitter to keep up-to-date with regulatory news and updates.

More than 170 countries throughout the world have implemented a VAT system, and some of the most recent adopters are the Gulf countries. In a bid to diversify economic resources, the Gulf countries have spent the past decade investigating other ways to finance its public services.

As a result, in 2016 the GCC (Gulf Cooperation Council), consisting of Saudi Arabia, UAE, Bahrain, Kuwait, Qatar and Oman, signed the Common VAT Agreement to introduce a VAT system at a rate of 5%.

Following the VAT agreement, Saudi Arabia and UAE implemented VAT in 2018. Bahrain followed with a VAT regime in 2019. Most recently Oman enforced a 5% VAT from April 2021, and looking ahead both Qatar and Kuwait are expected to enact VAT laws within the next year.

After the implementation of VAT and the increase of VAT rate from 5% to 15%, Saudi Arabia has taken the next step to digitize the control mechanisms for VAT compliance.

The E-invoicing Regulation enacted in December 2020 sets out an obligation for all resident taxable persons to generate and store invoices electronically. This requirement will be enforced from 4 December 2021.

Saudi Arabia has made considerable progress since it first introduced VAT in 2018. The Saudi E-invoicing Regulation is expected to not only encourage digitization and automation for businesses, but also to achieve efficiency in VAT controls and better macro-economic data for its tax authority, a development which will likely be replicated by other GCC countries soon.

Considering the efforts involved in the digitization of government processes and the VAT implementation timeline, the next candidate for similar e-invoicing adoption would likely be the UAE. While there are currently no plans for a mandatory framework, the UAE has announced bold plans for general digitization. According to the UAE government website, “In 2021, Dubai Smart government will go completely paper-free, eliminating more than 1 billion pieces of paper used for government transactions every year, saving time, resources and the environment.”

The spread of VAT digitization is typically the second reform following VAT adoption. As Bahrain and Oman also have VAT systems in place, introduction of mandatory e-invoicing in the next a few years in these countries would not come as a surprise. The adoption of e-invoicing in Qatar and Kuwait would depend on the success of VAT implementation, therefore it is not easy to estimate when their VAT digitization journey will begin but there is no doubt that it will happen at some stage.

After the adoption of e-invoicing, the Gulf countries may continue to digitize other VAT processes, including VAT returns. Pre-population of VAT returns using the data collected through e-invoicing systems is another trend that the countries are moving towards.

Regardless of the shape and form of digitization, there will be many moving parts in terms of VAT and its execution. Businesses operating in the region should be prepared to invest in their VAT compliance processes to avoid unnecessary fines and reputational risk for non-compliance.

To find out more about what we believe the future holds, download VAT Trends: Toward Continuous Transaction Controls. Follow us on LinkedIn and Twitter to keep up-to-date with regulatory news and updates.

A current mega-trend in VAT is continuous transaction controls (CTCs), whereby tax administrations increasingly request business transaction data in real-time, often pre-authorising data before a business can progress to the next step in the sales or purchase workflow.

When a tax authority introduces CTCs, companies tend to view this as an additional set of requirements to be implemented inside ERP or transaction automation software by IT experts. This kneejerk reaction is understandable as implementation timelines tend to be short and potential sanctions for non-compliance significant.

But businesses would do better to approach these changes as part of an ongoing journey to avoid inefficiencies and other risks. From a tax authority perspective, CTCs are not a standalone exercise but part of a wider digital transformation strategy where all data that can be legally accessed for audit purposes is transmitted to them electronically.

In many tax authorities’ vision of digitization, each category of data is received at ‘organic’ intervals that follow the natural cadence of data processing by the businesses and data needs of governments.

Tax administrations use digitization to access data more conveniently, on a more granular level, and more frequently.

A business that doesn’t consider this continuum from the old world of reporting and audit to the new world of automated data exchange risks over-focusing on the ‘how’ – the orchestration of messages to and from a CTC platform – rather than keeping a close eye on the ‘why’ – transparency of business operations.

Data received quicker and in a structured, machine-exploitable format is infinitely more valuable for tax administrations as it gives them an opportunity to perform deeper analysis of both varying taxpayer and third-party sources of data.

If your business data is incomplete or faulty, you are likely exposing yourself to increased audits, as your bad data is under scrutiny and more transparent to the taxman.

Put differently, in a digitized world of tax, garbage-in will translate to garbage-out.

Many companies already have the magic formula to fix these data issues at their fingertips. Start by preparing for this wave of VAT digitization with a project to analyse internal data issues and work with upstream internal and external stakeholders – including suppliers – to fix them.

Tools designed to introduce automated controls for VAT filing processes can help achieve better insight into the upstream data issues that need ironing out. These same tools can also help you through the CTC journey by re-using data extraction and integration methods set up for VAT reporting for CTC transmission, thereby creating better data governance and keeping a connection between these two naturally linked processes.

A lot of bad data stems from residual paper-based processes such as paper or PDF supplier invoices or customer purchase orders. Taking measures now to switch to automated processes based on structured, fully machine-readable alternatives will make a big difference.

Improving invoice data is not the only challenge. With the inevitable broadening of document types to be submitted under CTC rules (from invoice to buy-side approval messages, to transport documents and payment status data) tax administrations will cross-check more and more of your data, as well as trading partners’ and third parties’ data — think financial institutions, customs, and other available data points.

Tax administrations are unlikely to stop their digitization efforts at indirect tax. Mandates to introduce The Standard Audit File for Tax (SAF-T ) and similar e-accounting requirements show how quickly countries are moving away from the old world of tax and onsite audits.

All this data, from multiple sources with strong authentication, will paint an increasingly detailed and undeniable picture of your business operations. It is just a matter of time before corporate income tax returns will be pre-filled by tax administrations who expect little to no legitimate changes from your side.

‘Substance over form’ is a popular aphorism in the world of tax. As more business applications and data streams become readily accessible by tax administrations, you need to start considering data quality and consistency as a first step towards thriving in the world of digitized tax enforcement.

In the end, tax administrations want to understand your business. They don’t just want data, they want meaningful information on what you do, why you do it, how you trade, with whom and when. This is also exactly what your owners and management want.

So the ultimate goals are the same between businesses and tax administrations – it’s just that businesses will often prioritise operational efficiency and financial objectives whereas tax administrations focus on getting the best, most objective information possible.

Tax administrations introducing CTCs as an objective may be a blessing in disguise, and there are benefits of introducing better analytics to your business to comply with tax administration requirements.

The real value lies in real-time insight into business operations and financial indicators such as cash management or supply chain weaknesses. This level of instant insight into your own business also enables you to always be one step ahead, leaving you in control of the picture your data is providing to governments.

CTCs are the natural next step on a journey to a brave new world of business transparency.

Download VAT Trends: Toward Continuous Transaction Controls for other perspectives on the future of tax. Follow us on LinkedIn and Twitter to keep up-to-date with regulatory news and developments.

Update: 23 March 2023 by Dilara İnal

Japan is moving closer to the roll-out of its Qualified Invoice System (QIS), which will happen in October 2023.