Electronic invoicing is rapidly becoming a standard business process. Governments are pushing for the adoption of B2G invoicing to optimize the public procurement process and also to provide a boost to the adoption of e-invoicing between businesses.

Apart from countries that have introduced general e-invoicing mandates to improve fiscal controls – most of which have so far been in Latin America – countries in Europe and some in Asia are looking towards the PEPPOL framework to generate both business process and fiscal benefits through standardization.

PEPPOL was established to simplify interoperability, initially for public procurement transactions, but it is being built upon to encompass fiscal reporting or invoicing ‘clearance’ concepts as well.

B2G e-invoicing in Europe with PEPPOL

As part of harmonizing and digitizing public procurement processes within the EU, governments and other public bodies under Directive 2014/55/EU are required to be able to send and receive electronic invoices in accordance with the European Standard EN-16931.

All EU Member States’ public administrations had to be able to receive e-invoices at least for public procurement transactions either by November 2018 or by April 2019, with the possibility for Member States to extend the deadline by one extra year for sub-central authorities.

Several countries have taken the opportunity to generally mandate B2G electronic invoicing when implementing the Directive 2014/55/EU, so that both the public sector and private sector supplier will be obliged to send invoices electronically in B2G transactions.

Examples of countries that have introduced B2G mandatory e-invoicing are Sweden, Croatia, Estonia, Lithuania and Slovenia, and there is an upcoming mandate in Portugal that will come into force for all companies by January 2022. Finland is aiming for the same effect through a buyer-initiated mandate for the supplier to send e-invoices.

What is PEPPOL?

The PEPPOL project was initiated in 2008. One of its main objectives was standardization of the public procurement process in European governments. PEPPOL is a set of artifacts and specifications created to enable cross-border e-procurement, supported by a multi-lateral agreement structure which is owned and maintained by the OpenPEPPOL association.

PEPPOL aims to remove complexity around interoperability, as all parties that use PEPPOL will adhere to the same regulations and technical standards to exchange e-documents. Through the PEPPOL network, companies can exchange electronic procurement documents including e-Orders, e-Advance Shipping Notes, e-Invoices and e-Catalogues via access points based on what is known as a four-corner model – meaning that suppliers and buyers are represented by service providers that process data on their behalf.

While PEPPOL is known to have its initial focus in Europe, it is expanding beyond the EU to Asia and recently has also received more attention in the Americas. Singapore was the first country in Asia and the first outside Europe to establish a PEPPOL Authority, facilitating the framework on a national level, but was soon followed by other countries.

Currently, there are OpenPeppol members in 31 countries. In addition to countries in Europe, these include Australia, Canada, China, Japan, Mexico, New Zealand, Singapore and USA, with Japan being the newest addition.

Recent developments in B2G e-invoicing

As explained above, several EU Member States took the opportunity when transposing the Directive 2014/55/EU to make B2G e-invoicing mandatory.

More countries are now following that path:

Cyprus recently launched a Public Consultation on the bill which will make electronic invoicing mandatory for Public Procurement transactions as from 1 January 2022.

Latvia has plans to make electronic invoicing mandatory for B2G transactions from 2025 in accordance with the PEPPOL framework.

In Australia, all Commonwealth Government agencies are mandated to adopt e-invoicing by 1 July 2022 with the PEPPOL framework. The New South Wales government agencies are obliged to adopt e-invoicing for goods and services up to the value of AUD 1 million already from 1 January 2022, leading efforts to see e-invoicing adopted across Australia by making this change six months ahead of the mandate. There is no requirement in the pipeline to mandate businesses to send e-invoices to the government entities.

What is next?

Developments in B2G e-invoicing can no longer be considered separate from B2B e-invoicing. After all, many companies supply goods or services to public authorities, and investments in complying with government customer requirements under schemes like PEPPOL will drive the use of these same standards and rules in the business-to-business sector.

This also means that initiatives towards business-to-business electronic invoicing as a way for tax administrations to receive VAT-relevant data in real-time or near-real-time are increasingly influenced by concepts from the public procurement world.

This spillover goes well beyond conceptual inspiration. In Italy, for example, support for mandatory e-invoicing for VAT control purposes in 2019 was built on a massive data processing platform that was initially designed to facilitate public procurement. France and Poland are far down the path of similar architectures for their continuous transaction controls plans.

As PEPPOL becomes more popular as a standard to make country-specific public procurement methodologies more easily accessible for suppliers abroad, its concepts will increasingly penetrate the broader worlds of electronic invoicing, electronic trade and fiscal compliance.

Ministry Publishes Draft Guideline on B2B E-Invoicing

The German Ministry of Finance (MoF) released a draft guideline on 13 June 2024, detailing the upcoming B2B e-invoicing mandate which will roll out on 1 January 2025.

Although the current law only obliges taxpayers to issue and receive e-invoices for domestic B2B transactions, the MoF plans to introduce an e-reporting system for invoice details at a later stage, with no set date.

The highlights from the guidelines are:

E-invoicing exemptions include tax-free services, invoices under EUR 250, and travel tickets.

E-invoices must comply with EN 16931 syntaxes or a mutually agreed format that meets the requirements. XRechnung, ZUGFeRD (from version 2.0.1), Italy’s FatturaPA and France’s Factur-X are mentioned as compliant formats.

E-invoices can be structured or hybrid with a human-readable part. If discrepancies occur, the electronic data takes precedence.

E-invoices can be sent via email, electronic interfaces or portals, but not on USB sticks.

Corrections must be in electronic form.

Issuers can rely on recipient-provided domestic entrepreneur status unless there’s contrary information.

Recipients who cannot accept e-invoices cannot demand alternatives, and issuers fulfil their VAT obligations if they make documented efforts to send e-invoices. Recipients must ensure e-invoicing compliance. Non-compliant invoices, such as PDFs or paper, are not valid for tax deductions.

The final version of the guideline is expected by Q4 2024.

Update: 26 March 2024 by Dilara İnal

German Parliament Passes the B2B e-Invoicing Mandate

The German parliamentpassedthe Growth Opportunities Act (Wachstumschancengesetz – the Act) concerning various tax matters on 22 March 2024, including a nationwide B2B electronic invoicing mandate.

The Act was originally scheduled for a vote at the end of 2023, with enforcement planned for January 2024. However, the lack of consensus between the Bundestag and Bundesrat – lower and upper houses of the parliament, respectively – in various provisions of the Act delayed its finalisation.

The Mediation Committee of the Bundestag and Bundesrat concluded its negotiations about the Act on 21 February 2024, and the Bundestag approved the amended text on 23 February. The Bundesrat’s vote on 22 March completed the parliamentary process.

The implementation timeline for this mandate has been confirmed as follows:

1 Jan 2025: Mandatory receipt and voluntary issuance of e-invoices

Mandatory receipt of e-invoices for domestic B2B transactions will be required for all businesses. Additionally, businesses will have the option to issue e-invoices that are compliant with the approved syntaxes based on CEN 16931 voluntarily, without the Buyer’s consent.

1 Jan 2027: Mandatory issuance of e-invoices will be implemented for businesses (large taxpayers) with an annual turnover of at least EUR 800,000.

1 Jan 2028: Mandatory issuance of e-invoices will be extended to include all remaining businesses (small taxpayers)

Following this parliamentary approval, the Act will be signed by the President and subsequently published in the official gazette.

Acceptable invoice formats to issue in following years:

Domestic B2B Invoices

2024

2025

2026

2027

2028

Paper Invoices

Allowed

Prohibited

for large taxpayers

Prohibited

for all

E-invoices in EN 16931 format

Allowed with Buyer’s consent

Allowed

Mandatory

for large taxpayers

Mandatory

for all

EDI invoice not EN 16931 format

Allowed with Buyer’s consent

Allowed if are interoperable with the CEN, if the required information can be extracted into CEN

Other invoices in e-form (e.g. PDF, JPEG)

Allowed with Buyer’s consent

Allowed if are interoperable with the CEN, if the required information can be extracted into CEN** Please note that exchange on EDI is permitted if the e-invoice aligns with European standards.

Additional Information Released for Germany’s B2B E-Invoicing Plans

In October 2023, The Federal Ministry of Finance (MoF) released additional information regarding electronic invoicing, one of the proposed tax measures included in the Growth Opportunities Act.

If the MoF’s proposal, with the details provided in the preceding updates, becomes law, the following will be applicable:

Invoices following the well-established XRechnung and ZUGFeRD formats from version 2.0.1 onwards must comply with the EN-based format requirements.

Efforts are underway to ensure the continued use of EDI (Electronic Data Interchange) procedures within the forthcoming legal framework, albeit with some necessary technical adjustments.

It is important to highlight that the government draft outlines a phased transition, though all taxpayers will be obliged to be able to receive electronic invoices as of 1 January 2025.

Besides MoF clarifications, the upper house of the German Federal Parliament, Bundesrat, addressed the Act during its session on 20 October. While the Bundesrat supports the introduction of mandatory e-invoicing, it has proposed a two-year delay so the mandatory receipt of electronic invoices commences on 1 January 2027.

In the next steps of the process, the lower house of the Parliament, Bundestag, is expected to vote on the Growth Opportunities Act in mid-November. The upper house’s vote should take place in mid-December.

Federal Government Approves Mandatory B2B E-Invoicing and Extends Voluntary Phase

On 30 August, the German Federal Government approved the draft act known as the “Growth Opportunities Act,”. The act consists of several provisions on different tax matters, including the introduction of a nationwide B2B e-invoicing mandate.

Key dates for implementation of the mandate include:

From 1 January 2025: Issuing e-invoices will be allowed without the buyer’s consent if the e-invoice is fully compliant with the e-invoicing standard set forth by the European Committee for Standardization (CEN), EN 16931. Paper invoices will still be permitted throughout 2025.

From 1 January 2026: Scheduled commencement of mandatory implementation of B2B e-invoicing.

The draft bill approved by the government does not change the previously communicated framework, however it extends the voluntary phase by one year. The voluntary phase will last until January 2027 for small companies with annual turnover of 800,000 EUR or less in 2025.

Next steps for the e-invoicing mandate

The Federal Parliament and the Federal Council are expected to give their approval to this reform by the end of 2023.

German Regulatory Changes For Mandatory E-invoicing

The German Federal Ministry of Finance (the Ministry) shared the draft “Growth Opportunities Act” with significant German business associations on 14 July 2023. This act introduces amendments to VAT law to implement mandatory e-invoicing, along with other national and international tax-related proposals.

Currently, issuing an electronic invoice requires the buyer’s consent. Proposed amendments will change this, with invoices for transactions between German resident taxpayers – known as domestic B2B transactions – required to be electronic.

The act also introduces a new definition for e-invoices. An electronic invoice is defined as an invoice issued, transmitted and received in a structured electronic format that enables electronic processing. An e-invoice must also comply with the eInvoicing standard of the European Committee for Standardization (CEN), EN 16931.

The Ministry previously shared its plan to roll out mandatory e-invoicing as of January 2025. This date remains the same in the amendment proposals, with transitional measures giving taxpayers some time and flexibility to comply with the new requirements:

Paper invoices will be accepted until the end of 2025. Also, electronic invoices that do not comply with the CEN standard can be issued if the buyer’s consent is obtained. However, electronic invoices based on the CEN standard can be issued without the buyer’s consent.

E-invoices do not have to meet the CEN standard until the end of 2027, if transaction parties agree and exchange invoices via electronic data interchange (EDI).

Even though this act does not include any provisions for a transaction-based reporting system, it notes that such a reporting system for B2B sales will be introduced later.

European Council issues derogation decision

The European Council authorised Germany to introduce special measures regarding mandatory electronic invoicing with its decision dated 25 July 2023.

Germany received the derogation from the VAT Directive from 1 January 2025 to 31 December 2027 or, if an EU directive is adopted earlier than planned, until the national transposition of the VAT in the Digital Age (ViDA) directive into German law.

Germany Takes Another Step Towards CTC by Proposing an E-Invoicing Mandate

The German Federal Ministry of Finance sent a discussion proposal for the introduction of mandatory B2B e-invoicing in Germany on 17 April to significant German business associations.

The business associations are requested to provide their opinion on matters such as the following by 8 May:

The timeline: The Ministry suggests a phased introduction of mandatory e-invoices for domestic B2B supplies starting from 1 January 2025. The associations are asked to consider this timeline as well as organisation size, exemptions and more

A new e-invoice definition: Based on VAT in the Digital Age (ViDA) using structured data and the European Norm

A definition of “other invoices”: For those that do not fall under the new e-invoice definition, which includes paper or PDF invoices

The proposed e-invoicing mandate is a step toward implementing a real-time transaction-based reporting system for creating, verifying and forwarding e-invoices. This system is not part of the current proposal, but – as this is directly related to an e-invoice mandate – the ideas for such a system are laid out at a high level by the Ministry of Finance.

The final aims to provide a uniform electronic transaction-based reporting system for national and cross-border B2B transactions. The invoice exchange would be done via a central or private platform.

No verification of the full invoice content would be performed or interruption of forwarding of the invoice – however, the issuer’s platform would check (“Plausibilitätsprüfungen”) that all mandatory fields are present, whether structure and syntax are EN-compliant and so on.

The reporting of the invoice would be in real-time at the same time as the invoice is sent so that the supplier would not have to initiate two transactions.

The Ministry of Finance states the aim is for the new system to be aligned with ViDA but that Germany counts on having to use a derogation from the provisions of the VAT Directive to introduce the e-invoice mandate, should ViDA not be adopted in time.

While many have speculated around Germany going down the path of the Italian e-invoicing system, the message from the Ministry of Finance seems rather to be that the cues are taken from the French system, with the use of a centralised platform complemented with private service providers who serve to channel the invoices.

Need to discuss how Germany’s proposal to introduce continuous transaction controls could affect your business? Speak to our tax experts.

Update: 3 November 2021 by Joanna Hysi

Germany Steps Closer to Introducing Continuous Transaction Controls

There’s been increased discussion among different institutions about the introduction of continuous transaction controls (CTCs) in Germany to combat tax fraud and boost the competitiveness of the German market in Europe.

Supporters of a CTC reform

Proponents of the introduction of CTCs in Germany include, among others: the parliamentary group of the business-friendly Free Democratic Party (FDP), the German Association for Electronic Invoicing (VeR) and an independent judiciary body, the German Bundesrechnungshof (Federal Audit Office).

Recently, we’ve seen this topic included in tax policy negotiations of the coalition partners that emerged from the recent German government elections (the Social Democratic Party (SPD), FDP, and the Green Party).

While the discussions remain at a conceptual level, the new potential coalition parties display political will for reform in this area.

Proposals on CTC reform

Specifically, the German Bundesrechnungshofproposed to the Ministry of Finance a real-time reporting system leveraging blockchain technology as an efficient system to combat VAT fraud. However, their proposal wasn’t accepted on the grounds that a cost-benefit analysis is required before such measures are proposed and implemented.

As part of a parliamentary process the FDPcalled for “an electronic reporting system comparable to the Italian SDI to be introduced nationwide as quickly as possible, for the creation and testing and forwarding of invoices”. The leading German industry association, the VeR, welcomed this proposal recognising its numerous advantages to companies and the German economy.

A VeR study on whether the Italian model can be used as a blueprint for Europe explains that although it doesn’t seem to have contributed significantly to reducing Italy’s VAT gap, the advantages of e-invoicing to companies and the Italian economy are convincing. It concludes that the Italian clearance system can serve as a model for the digitization of VAT in Germany, if not in Europe. In addition, the VeR experts offer their knowledge to develop such a CTC system in Germany.

Conclusion: Will Germany be the next EU country to introduce CTCs?

It seems that the idea of introducing a CTC system in Germany – following in the footsteps of fellow Member States like Italy, France and Poland – is gaining traction and might not be far from becoming reality if the coalition partners indeed manage to reach a coalition agreement to succeed the currently ruling party.

From food distribution to automotive manufacturing and logistics, companies are distributing their supply chain activities around the world to reduce costs, expand into lucrative markets and launch new products faster.

165 countries worldwide levy a form of VAT. Each has its own set of rules for both compliance and reporting. From differences in local VAT legislation to evolving international VAT reporting trends, if you trade cross-border you’ll be subject to change. This may create new requirements for invoicing, VAT registrations and VAT reporting obligations.

Companies that ignore the importance of VAT compliance could easily erase the benefits of a global supply chain, disrupting operations and cash flow, and negatively impacting the bottom line in the process.

This is why VAT compliance needs to be a critical factor in supply chain planning.

Cross-Border Supply Chain Review and Transaction Mapping

A holistic view of your full business activity, mapped against the changing legislative, political and economic landscape, to deliver clarity to all functions within your business so you can trade with confidence.

Download our infographic for full details of our cross-border supply chain review and transaction mapping service.

Global events are popular once again and conferences and exhibitions often create VAT registration obligations in different European Union Member States that your business operates in.

Navigating these complex place of supply rules can be challenging. Legislation varies country-to-country and the type of event you’re organising affects this. Download our helpful guide to understand what your VAT obligations are.

Place of Supply Rules

When determining where tax applies to an event, it’s important to consider the place of supply rules.

These can be confusing and hard to interpret. When organising events and conferences, there are two basic rules to think about:

Does the service being supplied fall under the general place of supply rules, in which case, if the supply is B2B, VAT is due where the customer is based. In this scenario if the customer is established outside the UK, then the customer has to account for VAT on behalf of the supplier in the country they are established in under the reverse charge rules in the EU or potentially equivalent if non-EU.

Does the supply fall under any of the exceptions to the main rule? The most common example being admission to conferences and events whereby VAT is due where the event is held.

Get the guide

As you can see, VAT and events is a complex affair.

Admission to events, exhibitions and conferences in the EU is subject to VAT in the country where the event takes place. In addition to admission, other considerations include stand rental, local suppliers, sponsorship packages and catering services.

Our guide covers these topics:

VAT registration – where should I register and what VAT rules should I consider?

Event organisers – what VAT liabilities apply and how does it affect clients?

Online events – how do the rules differ for online events, both for B2B and B2C?

Hybrid events – are these taxed differently?

VAT reclaims – what claims are possible and what VAT can I recover?

Tour operators margin scheme (TOMS)

In addition to these common concerns, the Sovos Understanding VAT Obligations: European Events guide also explores TOMS – the tour operators margin scheme.

If a business buys in and sells services such as hotel accommodation, passenger transport or excursions to its clients/delegates in its own name, TOMS may well apply. The supply of services that fall under the scheme receive a different tax treatment to most supplies of services. They can require the undertaking of a complex calculation.

Also covered is a summary of non-EU events and how to apply VAT when hosting an event outside of the European Union.

For example, some non-EU countries will apply similar rules to the EU and a registration may be

Needed. However the issues will often be complex and require a business to carefully consider the organisation of the event at the outset. VAT recovery in non-EU countries will also vary and not all countries will allow refunds to overseas businesses.

Compliance peace of mind with a complete, global VAT Managed Service from Sovos

Whatever your VAT implications, Sovos has the expertise to help you navigate your global events and the complexities of cross-border VAT obligations. Our VAT Managed Services ease your compliance workload while mitigating risk wherever you operate today. In addition, we ensure you’re ready to handle the VAT requirements in the markets you intend to lead tomorrow.

Tax in Romania: All you need to know about Romania’s VAT regime

Romania introduces measures to digitally transform its tax administration and close the VAT gap

Seeking to close its VAT gap, the Romanian tax authorities have been discussing the idea of implementing measures to combat the country’s ever-increasing VAT gap. After years of discussion, the country announced its Standard Audit File for Tax (SAF-T) initiative which began in January 2022.

Have questions? Get in touch with a Sovos expert on tax in Romania

Tax in Romania: Romania’s SAF-T reforms

The Organisation for Economic Co-operation and Development (OECD) introduced SAF-T in 2005, and Romania joins a long line of European Member States adopting this form of tax legislation.

From 1 January 2022, companies in the General Directorate for the Administration of Large Taxpayers list must report their VAT electronically to the Romanian tax authorities. Transaction and accounting data must be reported through Declaratiei Informative D406 (SAF-T Romania).

This move is not uncommon and follows the trend being seen across the EU with tax administrations requiring increasingly granular data in real-time in Italy, Spain and Hungary paving the way for pre-populated VAT returns.

D406 must be submitted electronically in PDF format with an XML attachment and electronic signature. The combined file size must not exceed 500MB for it to be accepted at the portal.

Submission deadlines can be periodically, annually or on demand.

There is currently a six-month grace period from 1 January 2022.

Asset information is expected to be required annually, though no date has officially been announced.

Continuous transactions control (CTC) reforms

The ANAF, Romania’s tax authority, has introduced the RO e-Invoice system. It is optional in the first phase, aiming as a first step at the relationship between companies and the state (B2G) and as a second step, the B2B transactions with high-risk products.

The ultimate goal, as is often the case when a tax administration wants visibility of more data so they can take steps to close their national VAT gap, looks set to be a system that ‘clears’ each supplier invoice prior to it being sent to a buyer.

In this respect, as of 1 July 2022, suppliers will be obliged to use the RO e‑Invoice system in B2B transactions, including high fiscal risk products. Moreover, Romania wants to expand the implementation of e‑invoicing to a broader economy as a next step.

Finally, the Ministry of Finance has announced the introduction of a mandatory e-transport system for monitoring certain goods on the national territory from 1 July 2022. The transportation of high-fiscal risk products must be declared in the e-transport system a maximum of three calendar days before the start of the transport, in advance of the movement of goods from one location to another.

The system will generate a unique code (ITU code) following the declaration. This code must accompany the goods being transported in physical or electronic format with the transport document. Competent authorities will verify the declaration and the goods on the transport routes.

Use of the RO e-Factura system will be mandatory for high-fiscal risk products in B2B transactions from 1 July 2022. High-risk fiscal products include:

Vegetables, fruits, roots and edible tubers, other edible plants

Alcoholic beverages

New constructions

Mineral products (natural mineral water, sand and gravel)

Clothing and footwear

Suppliers of high fiscal risk products must use the RO e-Factura system even if their buyers are not registered with the system.

The transportation of high-fiscal risk products must be declared in the e-transport system.

Mandate rollout dates for SAF-T and CTCs

Romania SAF-T

September 2021: Voluntary test period began with D406T allowing taxpayers to become familiar with the data extraction and mapping requirements.

January 2022: Large taxpayers included in the Romanian tax authority’s list in early-2021 must comply with new SAF-T regulations.

1 July 2022: Large taxpayers added to the list in November 2021 must comply with the new SAF-T regulations.

1 January 2023: Medium taxpayers must begin submitting SAF-T data.

1 January 2025: Small taxpayers must begin submitting SAF-T data.

Romania CTC

March 2020: Pilot program launched.

November 2021: Voluntary participation of B2G scheme.

1 April 2022: Voluntary participation of suppliers in B2B transactions including high-fiscal risk products scheme.

1 July 2022: Mandatory e-invoicing for B2B suppliers of high-fiscal risk products and mandatory issuance of e-transport document for the transport of high fiscal risk products.

2023: Mandate expansion to other B2B flows expected.

INFOGRAPHIC

Romania’s SAF-T Requirements

Understand more about Romania SAF-T including when to comply, penalties, requirements and how Sovos can help

Faced with a VAT gap of nearly €13 billion, France is introducing mandatory e-invoicing for business-to-business (B2B) transactions from 2024, as well as e-reporting of additional data types. Applying to all companies established or, for e-reporting, VAT-registered in France, this new mandate is complex. It will also require significant planning.

According to the ICC, businesses will need at least 12-18 months to prepare for such continuous transaction control (CTC) mandates so it’s clearly important to start planning now to prepare for the change.

This infographic provides answers to your pressing points surrounding the mandate including:

What your company needs to do to comply with the new mandate

When your business needs to comply by

Other key information surrounding the mandate requirements

The aim of the new mandate is to increase efficiency, cut costs and fight fraud via access to more transaction data. All B2B invoices will need to be transmitted through a central platform. This will be either directly or via registered service providers connected to the platform.

The new mandate will provide the French tax authority with access to all VAT relevant data related to B2C and B2B transactions, so it’s crucial to adjust your business systems and processes to avoid penalties and fines.

France is the latest country to adopt CTCs, as tax authorities across the world look to gain greater insight and close the VAT gap. The proposed requirements come into effect during the years 2024-2026.

France e-invoice and e-reporting rollout dates

July 2024: All companies, irrespective of size, must accept to receive e-invoices under the new rules. The largest 300 companies will be subject to the B2B e-invoice issuance mandate and wider e-reporting mandate. The e-invoicing mandate does not apply to B2C and cross-border invoices. However, there is an obligation to report those transactions so the tax administration has full visibility.

January 2025: Obligations will apply to a further 8,000 medium-sized companies.

January 2026: All remaining medium and small companies will be in scope of the mandate.

Sovos serves as a true one-stop-shop for managing all e-invoicing compliance obligations in France and across the globe. Sovos uniquely combines local excellence with a seamless, global customer experience.

Our scalable, end-to-end solution ensures e-invoicing and e-reporting compliance in not only France but also 60+ other countries.

Sovos is purpose built for modern tax – an evolving, complex landscape in which global tax authorities are requiring increased visibility and control into business processes, in many cases at the transaction level.

Tax authorities around the globe have embraced digitization to speed up revenue collection and reduce fraud while closing tax gaps. This is the catalyst for companies to move complete, connected and continuous tax compliance software into their digital financial core.

As country general manager, Elçim is responsible for all Sovos operations within Turkey and plays a key role in driving the strategy for the region. She thrives on success and fast growth having worked for companies including Oracle and Tech Mahindra.

Highly motivated, she strives for continued improvements not only for customers but also within Sovos, and for her team through collaboration and best practices. Elçim firmly believes that by removing the pain of tax compliance, companies can focus on their goals which in turn helps shareholders, local communities and the economy.

A natural leader, Elçim fosters key strategic relationships and has a strong teamwork ethos. She views challenges as algorithms and is always analysing and evaluating scenarios to achieve greater success.

In her first year with Gartner, Elçim was awarded the prestigious and rare Winner’s Circle and Eagle Award for outstanding sales achievements.

To relax, Elçim enjoys spending time with her husband, cooking with her daughters and collecting antique books. Curious by nature and with a passion for being outdoors, she loves to travel and explore different places and cultures. She is fluent in both English and French.

On 26 November, Black Friday presents another opportunity for retailers to drive e-commerce sales and boost revenue. Retailers will be working hard to prepare the best deals to entice shoppers, but do you know where you stand with VAT compliance in the EU?

In our latest webinar, learn how the new EU e-commerce VAT rules will apply to retail businesses ahead of this year’s annual shopping event. In addition, we’ll explain how this year B2C retailers can – for the first time in respect of goods – account for VAT on Black Friday sales in the EU using the VAT One Stop Shop (OSS) schemes. These schemes can greatly simplify VAT compliance by removing the need to register for VAT in multiple Member States.

Join Consulting Services Director Andy Spencer and Strategy Programs Director Anna Higgins in this webinar to learn:

What OSS schemes are available

How to register for OSS, IOSS or Non-Union OSS

Case studies selling into the EU

Changes required to comply ahead of Black Friday

We will host a short Q&A session at the end of this webinar.

Need more information? Sovos’ VAT managed service provides a full OSS service for your business. Let us handle the initial registration, monthly filling and any potential intermediary requirements. Click here to find out more.

The VAT Import One Stop Shop (IOSS)

Simplify EU VAT with IOSS in one single return

The Import One Stop Shop (IOSS) is here. Simplify your EU VAT compliance into a single VAT return – grow your sales in the EU, avoid fines and penalties and enhance the customer experience by removing unexpected fees for buyers.

Since its launch, we’ve been helping e-commerce businesses of all sizes make the switch to the new scheme. Our IOSS service provides you full access to our VAT compliance software solutions and a team of indirect tax specialists. Let us handle the initial registration, monthly filing and intermediary requirements so you can continue to focus on what you do best.

Speak to a VAT expert

What is IOSS?

Since July 2021, all goods imported into the EU, regardless of value, are subject to VAT. As of the same date, businesses selling imported goods valued at less than EUR 150 can now use IOSS to collect, declare and pay VAT to the local tax authorities in a single VAT return. IOSS simplifies your EU VAT compliance – unlock the full potential of the EU e-commerce market, maximise your cash flow, and provide an excellent customer service.

In order to obtain a registration, non- EU businesses need to appoint an intermediary. They can then obtain an IOSS VAT registration number in the Member State where the intermediary is established.

Full IOSS service

Let us handle the registration process, obtain a VAT number for your business and file the monthly IOSS returns. All included, no hidden fees.

Goods move through customs faster – IOSS calculates and accounts for VAT ahead of time instead of applying upon import

With an IOSS VAT registration number, the VAT is accounted for at the point of sale

Reduced charges for customs clearance – without an IOSS VAT registration, import VAT will be due when the goods are cleared in the EU and there are likely to be higher customs clearance costs

Quick Facts

The IOSS simplification is available to use now for any qualifying transactions

The scheme requires additional record-keeping: businesses must retain more detailed records of transactions than previously

IOSS VAT declarations are monthly

Businesses can correct previous IOSS VAT returns in the next one

Non-EU businesses may need to appoint an intermediary and obtain an IOSS VAT registration in the intermediary’s country of establishment in the EU

Depending on the nature of business activity/supply chains, non-EU retailers may need to report under the Union One Stop Shop (OSS) and non-Union OSS schemes.

Businesses need at least one ‘standard’ VAT registration and possibly more due to warehouses or similar if they are to use Union OSS. No other VAT registrations is needed for IOSS or non-Union OSS.

Penalties and Fines

Local tax authorities can issue penalties and fines to businesses if returns and payments are not submitted on time. In addition, repeated noncompliance can lead to a two-year exclusion from the scheme. Businesses would then need to register for VAT in all Member States where they import goods or have alternative arrangements in place to deal with the import VAT.

Businesses that want to use IOSS may require an intermediary. If an intermediary is required you can’t do it alone. Our comprehensive service handles all your registration, filing and intermediary requirements.

It’s time to get EU VAT compliance right with IOSS and Sovos

Our IOSS service gives you full access to our team of indirect tax specialists and VAT compliance software. Let us handle the initial registration, monthly filing and intermediary requirements so you can focus on what you do best.

Contact us to speak to a VAT expert and learn how to get started.

How Tax Compliance Impacts Supply Chain Globalisation: The VAT Effect in Europe and Beyond

VAT compliance throughout a global supply chain is paramount. It has never been more important to get right.

165 countries worldwide levy a form of VAT. Each has its own set of rules for both compliance and reporting.

Some governments are also now placing increased emphasis on indirect tax and changes to their tax regulations, with technology-enabled enforcement efforts.

Download this e-book for an in-depth look at the vital elements needed for today’s VAT compliance. There’s guidance to help with your tax strategy so you can maximise the benefits from an efficient global supply chain.

Get the e-book

Your VAT compliance strategy

Tax shouldn’t impede growth, and it doesn’t have to if you have a proactive tax compliance strategy. So to minimise risk, VAT needs to be a critical factor in supply chain planning.

In this e-book, we take a detailed look into crucial elements of VAT compliance, with clear explanations to inform your tax strategy and to also help you reap the full benefits of an efficient global supply chain. In detail, we look at:

What factors should you consider in VAT compliance planning? These include import VAT, local supply of goods, intra EU deliveries, chain transactions and triangulation, VAT reverse charge, in addition to zero-rated vs exempt goods.

What are the impacts of these types of tax and transactions? How these types of tax and transactions affect your business, when they apply, and what you need to do to avoid noncompliance.

What are the new and changed regulations and what do they mean for businesses? Many governments have dramatically changed their tax regulations, introducing continuous transaction controls (CTCs) and the Standard Audit File for Tax (SAF-T) so tax authorities can better detect errors in tax reporting, and also look for discrepancies.

The cost of getting it wrong

Failure to comply creates both risk and consequences for businesses such as:

Disrupting operations. Noncompliance can disrupt operations, putting supplier relationships and supply chain stability on the line. Consequently, goods may be delayed at customs borders goods may be delayed at customs borders if formalities are not complied with.

Delays in VAT refunds. Businesses could have their VAT refunds delayed, tying up significant sums of money that could instead be put toward paying suppliers or investing in innovations.

Fines and penalties. Errors can result in penalties or fines of up to 200% of VAT owed. This directly impacts the bottom line and also transforms VAT from a neutral to a hard cost.

The right technology for the job

VAT is becoming more complex and governments are digitizing indirect taxes. Therefore, businesses need to be armed with the right technology to simplify and streamline global tax obligations.

In the ever-changing legislative environment, businesses must also be able to maintain both control and visibility of their global tax obligations effectively. They need to use insights to predict what will change next.

With standardisation, automation and new levels of data, Sovos combines unparalleled regulatory expertise with technology that supports compliance by enabling:

Complete, continuous management of VAT determination and reporting, as well as business-to-government reporting in every country in which your business operates.

Comprehensive functional and geographic coverage of VAT reporting, CTCs, compliance archiving, and determination around the globe.

Integration with complex ERP, billing systems, POS, P2P and EDI systems as CTC and other VAT requirements create a much broader footprint on transactional and record-keeping systems.

Contact us now and let Sovos help you reap the full benefits of an efficient global supply chain.

Since then, a lot has happened: non-resident companies were brought into the scope of e-invoicing requirements, deadlines were postponed due to Covid, and new regulations have been published.

Get the information you need

Quick facts

Use of certified billing software is mandatory for the creation of all types of invoices (paper or electronic); this is understood to be the taxpayer’s ERP system. Since 2021, non-resident companies with a Portuguese VAT registration have also been obligated to issue invoices and other fiscally relevant documents via certified billing software.

A QR code should be included in all invoices issued through certified billing software. Technical specifications about the content and placement of the code in the invoice are available on the tax authority’s website.

A unique ID number (ATCUD) must be included in all invoices and fiscally relevant documents. The ATCUD is a number with the following format ‘ATCUD:Validation Code-Sequential number’.

Public entities must receive e-invoices whilst companies must send e-invoices since 1 July 2021. E-invoices must be issued electronically in the CIUS-PT format and transmitted to the public administration through one of the available web services.

A qualified electronic signature or seal, or the use of EDI with contracted security measures is mandatory for all electronic invoices from 1 January 2026.

Billing SAF-T has monthly submission requirements and must be completed with the normal VAT return by the 5th (until the 8th during the year of 2023 due to a grace period) day of the month following the reporting period. The Billing SAF-T may be submitted via the e-fatura portal or through web services.

Accounting SAF-T: annual submission is mandatory from 2027 via the tax authority´s portal which will enable automatic pre-filling of the VAT IES´ Annexes.

Important dates

1 July 2021: Non-resident taxpayers required to use a certified billing software to issue invoices and other fiscally relevant documents.

Issuance of B2G e-invoices:

1 January 2021: Phased rollout of mandatory issuance of e-invoices in the CIUS-PT format for large suppliers of the public administration.

1 January 2022: QR code requirement implemented for invoices and other fiscally relevant documents issued through a certified billing software.

1 January 2023: Unique ID number (ATCUD) is mandatory on all paper and electronic invoices.

1 January 2023: Non-resident taxpayers required to submit Billing SAF-T monthly.

2026 fiscal year: Mandatory annual submission of accounting SAF-T for residents and non-residents (first submission occurs in 2027 regarding the fiscal year of 2026)

1 January 2026: Mandatory B2G E-invoicing extended to include small and medium-sized businesses.

1 January 2026: Qualified electronic signature/seal or EDI mandatory for electronic invoices.

Need help to ensure your business is VAT compliant in Portugal?

Sovos provides a complete VAT, SAF-T and B2G compliance solution for Portugal helping customers meet the demands of the digital transformation of tax and public procurement through a single provider. Sovos uniquely combines local expertise with a seamless, global customer experience.

The Zakat, Tax and Customs Authority (ZATCA) announced the finalised rules for the Saudi Arabia e-invoicing system earlier this year, announcing plans for two main phases for the new e-invoicing system.

The first phase of the Saudi Arabia e-invoicing system is set to go live from 4 December 2021.

With the mandate just around the corner, we’ve highlighted the latest news on a reform that is still evolving.

The Detailed Guidelines

The latest documentation communicated on the requirements was the Detailed Guidelines, published in August 2021. The Detailed Guidelines provided clarity on the following topics:

Even though tax invoices must be generated electronically, they can be shared by sellers to buyers in an agreed format. For the first phase, the agreed format to exchange invoices may be electronic, human readable format, or a paper format. However, in the second phase, only XML format or PDF/A-3 with an embedded XML can be used to exchange e-invoices. In case the human readable format is used, it must be in Arabic (in addition to any other language) and Arabic or Hindi numerals can be used.

A printed copy of the simplified tax invoice must be provided to the buyers, however, and based on mutual agreement between the seller and buyer, the invoice can be shared electronically or through any other way where the buyer can read it.

The e-invoices generated by a third party will contain an electronic mark indicating this fact. This marker will be generated automatically and will not be visible on the human readable version of the e-invoice. The human readable format of the invoice must contain a statement declaring that the invoice is a third-party billing invoice.

For the second phase, specific integration requirements will be published in the future.

Overview of readiness for the first phase

The first phase requirements are not as complex as the second phase requirements that will be enforced from 1 January 2023.

The ZATCA has been successful in providing taxpayers with the necessary information. The go live date is set to go ahead as planned and a delay is not currently expected.

On 1 July 2021 the EU E-Commerce VAT Package was introduced. The package replaced existing distance-selling rules and extended the Mini One Stop Shop (MOSS) into a wider-ranging One Stop Shop (OSS).

The implementation of the EU E-Commerce VAT Package was designed to simplify the VAT reporting requirements for sellers and improve the tax take for Member States.

Two months in: we take a look at how it’s going.

Delays and teething problems

There were unfortunately some initial delays and teething problems when the EU E-Commerce VAT Package was introduced, which is to be expected with the adoption of such a significant new system, but as with any new scheme these can be resolved over time.

Some examples include:

Netherlands system issues: The introduction of the system in the Netherlands appeared to cause an IT glitch whereby Article 23 licenses to defer import VAT were not recognised. As a result, importers were asked to pay VAT at the border. This caused delays in imports and onward delivery at the beginning of July. Once the Dutch tax authority became aware of this issue it implemented a temporary fix and the issue is now resolved.

Inconsistencies in data submission: There are inconsistencies in how taxpayers must communicate data to the relevant tax authority. The EU proposal foresaw a portal where all transactions could be uploaded, but this hasn’t materialised yet.

Varying file format requirements: Some Member States require data to be submitted in a .csv file whilst others ask for submissions in a .txt file. The Netherlands requires taxpayers to key data directly onto its website.

Data issues: There have been issues around receiving data and Sweden was briefly unable to receive data but this was quickly resolved (in less than a week).

IOSS processing errors: Some freight forwarders used the shipment date and not the payment date resulting in some consignments that didn’t qualify for IOSS to be processed under IOSS. This will lead to an underpayment of VAT and it will be necessary to reconcile the data.

Intrastat reporting: There is currently no mention in either the Directive or the explanatory notes of how Intrastat should be reported.

Issues with the import of goods

There are also issues associated with the import of the goods.

Some Member States disallow the import of certain categories of goods due to local restrictions e.g. foodstuffs, plants etc.

It’s sometimes unclear if freight forwarders have used IOSS or not and this could lead to repeated errors of underpayment or overpayment of VAT.

Some non-EU vendors are trying to avoid an IOSS registration by stating that the customer is the importer of record. Such practice happened before the introduction of IOSS but not always at the same level as it is now – and was not always spotted or queried.

However, since the introduction of the IOSS, some tax authorities, including Germany, are questioning such an approach on the grounds that the carrier who imports the goods is acting for the non-EU vendor and is not known by the buyer.

This means import VAT is due by the vendor who must then also charge German VAT. For cases that have already occurred there may be an issue with recovery of the import VAT, as the evidence required to support the deduction will have been issued in the wrong name (consumer).

It’s still early days for the EU VAT E-Commerce Package and initial teething problems are to be expected. One thing is certain, navigating these new VAT schemes is complex. Sovos is here to help and we’ll keep you updated on the latest regulatory changes.

Want to know more about simplifying EU VAT with IOSS?

Join our latest webinar on September 22, 2021 to learn how you can use the Import One-Stop Shop (IOSS) to simplify your EU VAT compliance and unlock the full potential of the EU e-commerce market.

Take Action

Still have questions about OSS and IOSS? Download our e-book to understand the implications of the 2021 EU e-commerce VAT package and ensure your business is ready by 1 July 2021 for the significant changes ahead

Join our latest webinar to learn how you can use the Import One-Stop Shop (IOSS) to simplify your EU VAT compliance and unlock the full potential of the EU e-commerce market.

Since July 2021, the low value consignment relief on small packages has been removed. From the same date, businesses selling imported goods valued at less than EUR 150 can now use IOSS to collect, declare and pay VAT to the local tax authorities in one single VAT return. IOSS simplifies your EU VAT compliance – making it essential to grow sales in the EU, avoid fines and penalties, and provide an excellent customer service.

Join Consulting Services Director Alex Smith and Senior Consultant Russell Hughes in this webinar to learn:

What is IOSS?

Registering and appointing an intermediary

Benefits of using the scheme

How Sovos can help

We will host a short Q&A session at the end of this webinar.

Need more information? Sovos’ VAT managed service provides a full IOSS service for your business. In addition to proving an intermediary service, we handle the IOSS registration and monthly filling. Click here to find out more.

But there are variations and identifying which class the policy is covering can be a challenge.

This article will cover what insurers need to know about Aviation Hull and Aviation Liability policy and what IPT rate to apply.

Variations in the Aviation policy

Aviation can fall under Class 5, Class 11 or General Liability.

There are five different variations of an Aviation policy, either taken out individually or in combination. Although the descriptions vary, the most referred to are:

Public and passenger liability insurance

Ground risk hull insurance, whilst in motion or stationary

In-flight insurance

Class 5 Aviation policies are focused on the hull and physical aspect of the aircraft, whereas Class 11 Aviation Liability mainly covers the public and passengers or damage to property owned by third parties.

Defining and applying the correct classification

Defining between Aviation Liability Class 5 and 11 can be a headache. As aviation policies can include a combination of liabilities, it can be difficult to know the correct classification to apply.

Some tax authorities have recognised this and applied similar rates for both, but there are exceptions.

For example, in Hungary Class 5 is considered CASCO , which stands for Casualty and Collision (automobile insurance). So, it has a higher IPT rate of 15% whereas IPT for Class 11 on Aviation Liability is 10%.

There are also parafiscal taxes to consider. These mainly come into effect when the policy includes a fire element. But as always there are exceptions – in Greece both classes are exempt from IPT, but TEAEAPAE (or Pension Fund) can be due on Class 5 Aviation when cover includes the maintenance of the aircraft.

Once the correct class of insurance has been applied to the policy, an additional reference to an AVN clause is made.

AVN clauses are additional to the main risk and more specific than some of the other coverages, which are also included in aviation contracts. There are over 214 AVN clauses and most fall under Class 13 General Liability.

Reporting

The last piece of the puzzle is how to report a policy document that could have up to three different classes.

The territory could have apportionment rules, meaning an insurer could benefit from some of those exemptions. Some insurers choose to take the prudent approach and apply the highest rate from the three classes to avoid noncompliance or penalties.

Easing the IPT compliance burden of aviation liability

For most insurers, classification of an aviation policy is only the beginning of the journey. There are other considerations such as location of risk rules outside of Europe, which can mean double taxation, or exemptions depending on the use of the aircraft.

To ease the burden on compliance, many insurers work with a managed service provider with IPT expertise.

Since then, a lot has happened: non-resident companies were brought into the scope of e-invoicing requirements, deadlines have been postponed due to Covid, and new regulations were published. This blog summarises the latest and upcoming changes.

QR Code

Introduced in 2019, the de facto implementation of the QR code requirement was delayed, and is now expected to be fully implemented by taxpayers in January 2022. A QR code should be included in all invoices. Technical specifications about the content and placement of the code in the invoice are available on the tax authority’s website.

ATCUD – Unique ID and validation codes

The ATCUD is a unique ID number to be included in invoices and is part of the content of the QR code. The ATCUD is a number with the following format ‘ATCUD:Validation Code-Sequential number’.

To obtain the first part of the ATCUD – the so-called ‘validation code’ -, taxpayers must communicate the document series to the tax authority along with information such as type of document, first document number of the series, etc.

In return, the tax authority will deliver a validation code. The validation code will be valid for the whole document series for at least a fiscal year. The second part of the ATCUD – the ‘sequential number’ – is a sequential number within the document series.

This month, the Portuguese tax authority published technical specifications for obtaining the validation code, creating a new web service. To access this web service, a specific certificate obtained from the tax authority is required and can be assigned to taxpayers or software service providers.

In addition, the tax authority has created a standard list of document classes and types, enabling the communication of document types in a structured format.

An ATCUD will be required in all invoices from January 2022. To be ready for the deadline, taxpayers must get the series’ validation codes during the last half of 2021 to apply in invoices issued in the beginning of 2022.

Consequently, since 1 July 2021, non-established but VAT registered companies must adopt certified billing software to comply with the Portuguese law as required by Law-Decree 28/2019, Decision 404/2020-XXII, and Circular 30234/2021.

E-invoices in B2G scenarios

The Portuguese e-invoicing mandate for business-to-government transactions includes a format requirement attached to specific transmission methods. In other words, invoices to the public administration must be issued electronically in the CIUS-PT format and transmitted through one of the web services made available by the public administration.

Initially, a phased roll-out started in January 2021, obliging large companies to issue e-invoices to public buyers. In July, the subjective scope was enlarged to include small and medium-sized businesses. The last step is to include microenterprises by January 2022.

Due to the Covid pandemic, Portugal established a grace period that has been renewed several times, whereby PDF invoices would be accepted by the public administration. Currently, the grace period runs until 31 December 2021, meaning that, in practice, all suppliers of the public administration, regardless of their size, should comply with the e-invoicing rules in public procurement by 1 January 2022.

In our last look at Romania SAF-T, we detailed the technical specifications released from Romania’s tax authority. Since then, additional guidance has been released including an official name for the SAF-T submission: D406.

Implementation timeline for mandatory submission of Romania SAF-T

Large taxpayers (as designated by the Romanian tax authorities) – 1 January 2022

Medium taxpayers – guidance indicates 2022, no official date released yet

Small taxpayers – 2023

To alleviate taxpayer concerns due to the complexity of the report and difficulties with extraction, the tax authorities are introducing a voluntary testing period which is due to begin in the coming weeks. During this period, taxpayers may submit what is known as D406T which will contain test data that the authorities will not use in the future for audit purposes.

Submission deadlines for Romania SAF-T

The Romanian SAF-T, D406, is based on the OECD schema version 2.0 which contains five sections:

General Ledger

Accounts Receivable

Accounts Payable</li<

Fixed Assets

Inventory

The submission deadlines are as follows:

Periodically (until the last calendar day of the month following the reporting period) – for information on General Ledger, Accounts Receivable, and Accounts Payable

Annually (until the deadline for submitting the financial statements for the financial year) – for information on Fixed Assets

On Demand (within the term established by the fiscal body, which may not be less than 30 calendar days from the date of request) – for information on Inventory

Taxpayers must submit sections of D406 monthly or quarterly, following the applicable tax period for VAT return submission.

For the first report, tax authorities have announced a grace period for the first three months of submission. This is from the date when the deposit obligation becomes effective for that taxpayer, where non-filing or incorrect filing will not result in penalization if correct submissions are submitted once the grace period ends.

Submission information for Romania SAF-T

The D406 must be submitted electronically in PDF format, with an XML attachment and electronic signature. The size of the two files must not exceed 500 MB. If the file is larger than the maximum limit, the portal will not accept it and the file must be divided into segments according to details set out in the Romanian guidance.

The tax authorities have indicated that, should a taxpayer find errors in the original submission, a corrective statement may be submitted to rectify these errors. The taxpayer should submit a second full corrected file to replace the original file that contains errors. If a taxpayer submits a second D406 for the same period, it is automatically considered a corrective statement.

Take Action

Need to ensure compliance with the latest Romania SAF-T requirements? Speak to our team. Follow us on LinkedIn and Twitter to keep up-to-date with the latest regulatory news and updates or see this overview on VAT Compliance in Romania.

Welcome to our Q&A two-part blog series on the French e-invoicing and e-reporting mandate, which comes into effect 2023-2025. That sounds far away but businesses must start preparing now if they are to comply.

The Sovos compliance team has returned to answer some of your most pressing questions asked during our webinar.

We have outlined the new mandate, e-invoicing specifically, and questions around this topic in our first blog post.

This blog will look at the other side of the mandate – e-reporting obligations. These will apply to B2C and cross-border B2B transactions in France, which must be periodically reported.

Payments E-reporting

First let’s look at common questions around payments e-reporting.

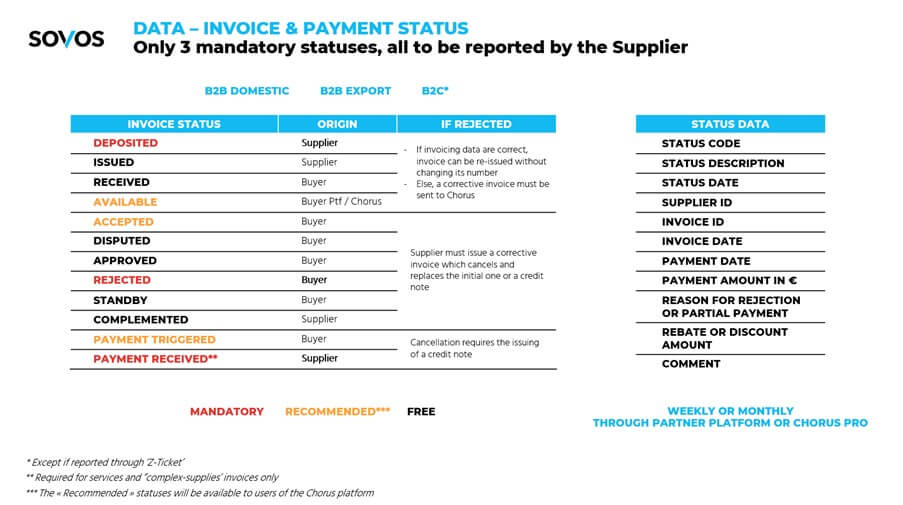

What are the invoice and payment statuses to be reported?

Here is a slide from our webinar showing invoice statuses, whether these are mandatory, recommended, or free, origins, action to take if rejected, status data, and when it needs to be reported:

Who is responsible for payment e-reporting? The buyer, the seller, or both?

It was initially rumoured to be both on the buyer and the seller side, but the latest information from DGFIP clearly states that it will be the responsibility of the seller to report the invoice status, and, if applicable, its payment status.

Some further clarification is needed though since the seller is dependent on the buyer’s response on some status (e.g. ‘invoice rejected’).

‘Partner’ platform certification requirements

Your e-invoicing and e-reporting project cannot be done in isolation. This is a significant project with many dependencies that involve external third parties.

There will be one or, in most likelihood, several third parties in the middle of the transaction chain. This will include Chorus Pro, chosen by the French government as the official and obligatory platform for businesses to issue e-invoices to public administrations.

This section covers common questions on partner platform certification requirements.

Is there a list of official validated partner platforms?

The 13 July 2021 DGFIP workshop dedicated to this matter highlighted that there would be a registration process for third-party platforms, as well as taxpayers who would want to run their own platform.

The registration process will consist of two phases:

Phase 1. A prior selection by the tax authorities based on the general profile of the candidate (e.g. are they up to date in their own tax payment duties?) and the services they propose;

Phase 2. Within 12 months after registration, an independent audit would have to performed that demonstrates that the platform meets the DGFIP requirements, such as:

Updating of the e-invoicing central directory

Issuing, transmitting / receiving e-invoices (including guaranteeing integrity and authenticity, as well as an advanced authentication process)

Processing and transmitting to Chorus Pro e-invoicing, e-reporting and payment status data

<liPerforming the control and mapping activities (extraction of invoicing data for both e-invoicing and e-reporting, certain invoice validation checks – mandatory fields, check sums, Customer ID verification – mapping to and from a minimum set of mandatory formats, compliance with GDPR, etc)

A few other key points to note are:

The registration and audit would need to be periodically renewed.

The consequences for non-compliant platform are not defined, an escalation process leading to the withdrawal of the registration would apply.

The platform operator might be French or foreign (although there is still a question mark as to whether non-EU operators will be permitted).

Implementation timeline

What is the current expectation on when exact required fields with be supplied by the government (invoice specs with all required fields and values)?

Excel files are available as a draft document at a very detailed level which Sovos can provide on request. The final specs should be known by the end of September 2021.

Take Action

Still have questions about e-reporting? Access our webinar on-demand for more information and advice on how to comply.