Top 5 Signs Your Winery is Ready for DtC Compliance Software

A quick guide to gauging if your business could benefit from automating DtC shipping compliance.

Subscribe to our Newsletter

Get monthly updates on Sovos ShipCompliant resources, data reports, fresh resources and more.

Subscribe nowTop 3 Things That Can Go Wrong if You’re Non-Compliant

The most essential considerations for compliant direct-to-consumer shipping

Subscribe to our Newsletter

Get monthly updates on Sovos ShipCompliant resources, data reports, fresh resources and more.

Subscribe nowThe Case for DtC Beer Shipping

Introduction

The wine industry has been shipping direct-to-consumer (DtC) for 20 years, and this once-novel market expansion has proven win-win-win for producers (business growth), states (increased tax revenue) and consumers (increased choice) alike. And yet, beer DtC remains a much narrower market. Why?

Beer producers aren’t the only ones asking that question. Sovos ShipCompliant’s 2025 Direct-to-Consumer Beer Shipping Report found that more than four in five regular craft beer drinkers (83%) say that current beer shipping laws in the U.S. should be updated to make it legal in more states—as do 64% of all Americans age 21+.

Lessons from 20 years of DtC wine shipping

DtC wine shipping is a nearly $4 billion market as of 2024. Because DtC shipping and three-tier distribution complement one another, the three-tier system has continued to thrive in its central role in alcohol distribution even as the DtC channel has grown. In fact, while DtC wine shipping has been in place for two decades, it makes up 8% of total off-premise wine sales in the U.S. (as estimated by Jon Moramarco, managing partner at bw166).

The success the DtC wine channel has found has gone hand in hand with shippers’ commitment to following state regulations and tax requirements. DtC wine shippers participate in a safe, well-regulated market, complying with varying state regulations that include:

- Getting properly licensed by the destination state;

- Abiding by regulatory rulings of the destination state;

- Conducting age checks and preventing sales to minors; and

- Correctly determining, paying and reporting on taxes owed to the states.

Additionally, shippers abide by destination states’ jurisdiction in terms of other producer-enablement rules that include customer volume limits, the registration of brand labels and brand ownership requirements.

Distinct product offerings

The products that reach consumers through the DtC wine shipping channel are not the same ones they are shopping for at their local retail outlets. Rather, wineries typically offer special allocations or other higher-end, more limited offerings direct-to-consumer.

Similarly, beer lovers are not necessarily looking to ship products that can be easily found at local retail stores. However, breweries can offer highly allocated and limited run products that consumers would otherwise have difficulty gaining access to.

Thus, there is generally no direct competition between the products available through these different channels — though a producer that grows its fan base via DtC shipping can expect to see increased demand for their products sold through the three-tier system. In fact, the DtC beer shipping report found that 95% of regular craft beer drinkers who are likely to purchase craft beer via DtC shipping say they’d be likely to look at retail for brands enjoyed via the DtC channel.

An equitable marketplace?

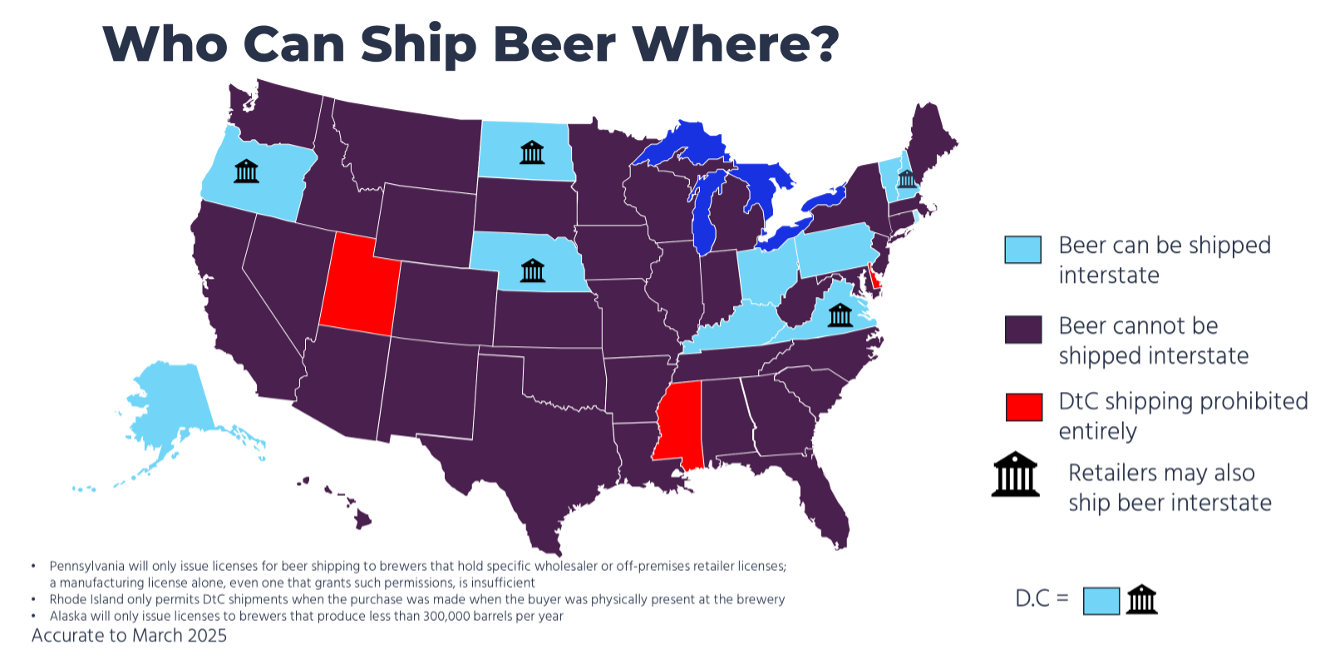

Across the vast majority of the U.S. — 47 states and the District of Columbia — DtC wine shipping is permitted. The map of where beer producers are legally entitled to ship DtC is much, much narrower.

* Pennsylvania will only issue licenses for beer shipping to brewers that hold specific wholesaler or off-premises retailer licenses; a manufacturing license alone, even one that grants such permissions, is insufficient.

Only 12 locales are open for DtC beer shipping, compared to wine’s 48:

As beer producers have demonstrated through their compliant participation in the three-tier system, they are readily equipped to mimic the conforming behaviors of their winery counterparts in the DtC shipping channel.

How states have benefited from DtC shipping

Naturally, states are eager to maximize the tax revenues they collect, as taxes fund their service to the public, including infrastructure, education and social services.

The compliant actions of DtC alcohol shippers to date has enriched states’ coffers to the benefit of many. As a leading beverage alcohol compliance solutions provider, Sovos ShipCompliant has facilitated states’ securing hundreds of millions in tax revenue each year. Because the footprint for legal DtC shipping of non-wine beverage alcohol is limited, the vast majority of this tax revenue is driven by DtC wine shipments.

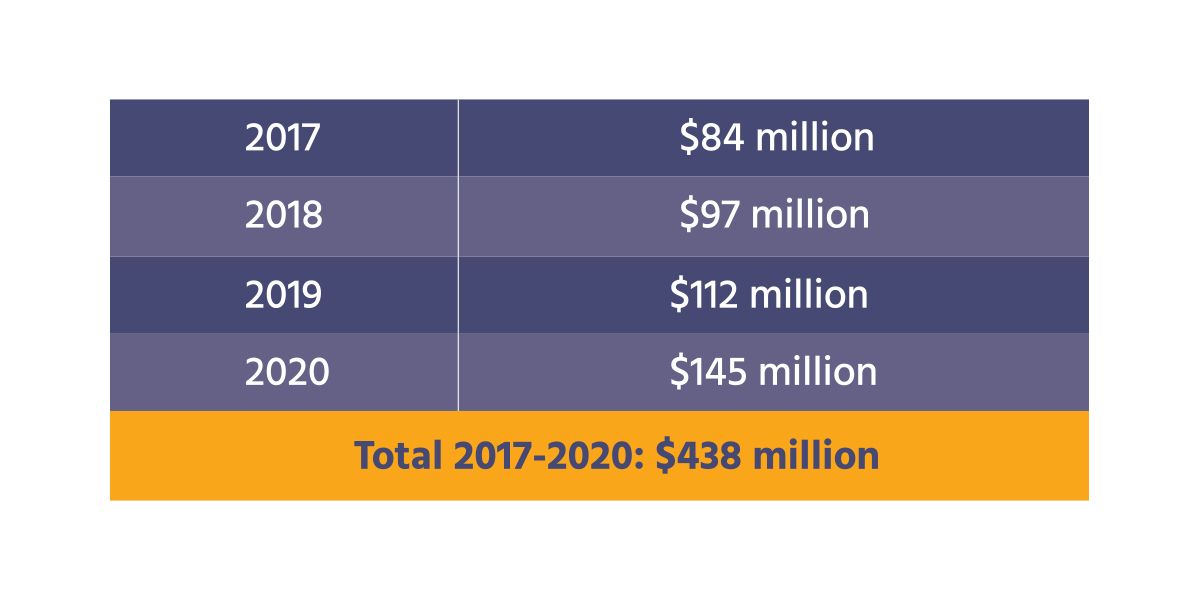

DtC Tax Revenue Paid to States via Sovos ShipCompliant

| 2017 | $88.6 million |

| 2018 | $101.4 million |

| 2019 | $117.8 million |

| 2020 | $149.7 million |

| 2021 | $172.8 million |

| 2022 | $180.1 million |

| 2023 | $177.4 million |

| 2024 | $171.6 million |

| Total 2017-2024 | $1.16 billion |

States opening to the DtC shipment of beer would only grow these welcome additional revenues.

In conclusion

The case for beer DtC shipping is clear. The demand is strong from producers and consumers alike, and states stand to benefit greatly. Some 20 years of well-regulated DtC wine shipping have paved the way for the healthy expansion of DtC beverage alcohol shipping.

Beer producers simply want the same kind of DtC market access that wine shippers enjoy. The data shows that DtC wine shipping is profitable for states and can be done safely. Consumers are ready for more choice and are already utilizing the DtC market. The time for expanded DtC beer shipping permissions is now.

Learn how Sovos ShipCompliant can help you manage your taxes and compliance for DtC shipping.

Talk to an expertSubscribe to our Newsletter

Get monthly updates on Sovos ShipCompliant resources, data reports, fresh resources and more.

Subscribe nowThe Case for Spirits Direct-to-Consumer (DtC) Shipping

Introduction

The wine industry has been shipping direct-to-consumer (DtC) for more than 15 years, and this once-novel market expansion has proven win-win-win for producers (business growth), states (increased tax revenue) and consumers (increased choice) alike. And yet, spirits DtC remains a much narrower market. Why?

Spirits producers aren’t the only ones asking that question. A Distilled Spirits Council of the United States (DISCUS) survey shows overwhelming consumer demand for DtC shipping of distilled spirits. Eight out of 10 consumers surveyed said distillers should be allowed to directly ship their products to legal-age consumers in any state. Additionally, some 76% said they would consider purchasing spirits online shipped directly from distillers to them from outside or within their state.

Lessons from 15 years of DtC wine shipping

DtC wine shipping is a $4.2 billion market as of 2021. Because DtC shipping and three-tier distribution complement one another, the three-tier system has continued to thrive in its central role in alcohol distribution even as the DtC channel has grown. In fact, while DtC wine shipping has been in place for 15+ years, it makes up 10%-11% of total off-premise wine sales in the U.S. (as estimated by Jon Moramarco, managing partner at bw166).

The success the DtC wine channel has found has gone hand in hand with shippers’ commitment to following state regulations and tax requirements. DtC wine shippers participate in a safe, well-regulated market, complying with varying state regulations that include:

- Getting properly licensed by the destination state;

- Abiding by regulatory rulings of the destination state;

- Conducting age checks and preventing sales to minors; and

- Correctly determining, paying and reporting on taxes owed to the states.

Additionally, shippers abide by destination states’ jurisdiction in terms of other producer-enablement rules that include customer volume limits, the registration of brand labels and brand ownership requirements.

Distinct product offerings

The products that reach consumers through the DtC wine shipping channel are not the same ones they are shopping for at their local retail outlets. Rather, wineries typically offer special allocations or other higher-end, limited offerings via the DtC channel — compared to more inexpensive wines that are widely available at retail or for which a consumer would be hard-pressed to justify the shipping cost. In fact, the average price per bottle of wine shipped DtC hovers around $40, three to four times the average price paid at grocery stores and liquor shops.

Thus, there is generally no direct competition between the products available through these different channels — though a producer that grows its fan base via DtC shipping can expect to see increased demand for their products sold through the three-tier system.

From a DtC shipping standpoint, a bottle of wine and a bottle of spirits look a lot alike — and as in wine, spirits producers offer a number of speciality or limited production releases — so there is every reason to expect that as more states open to DtC spirits shipping, the spirits industry will follow wine’s lead in offering distinct products via different channels.

An equitable marketplace?

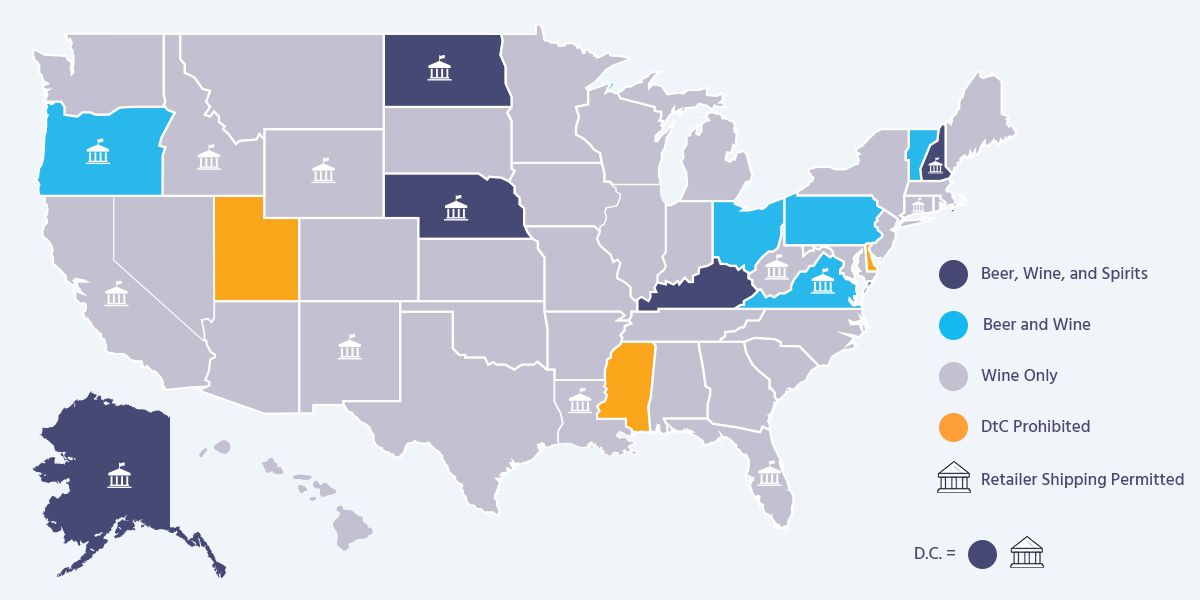

Across the vast majority of the U.S. — 46 states and the District of Columbia — DtC wine shipping is permitted. The map of where spirits producers are legally entitled to ship DtC is much, much narrower.

* Oregon will only issue licenses for beer shipping to breweries located in states that themselves permit DtC shipping of beer

* Pennsylvania will only issue licenses for beer shipping to brewers that hold specific wholesaler or off-premises retailer licenses; a manufacturing license alone, even one that grants such permissions, is insufficient

Accurate to October 2021

As the map demonstrates, the only seven locales open for DtC spirits shipping are Alaska, D.C., Kentucky, Nebraska, Nevada, New Hampshire, North Dakota and (in very limited fashion) Rhode Island, compared to wine’s 47.

As spirits producers have demonstrated through their compliant participation in the three-tier system, they are readily equipped to mimic the compliant behaviors of their winery counterparts in the DtC shipping channel.

What's fair for wine is also fair for spirits

How states have benefited from DtC shipping

Naturally, states are eager to maximize the tax revenues they collect, as taxes fund their service to the public, including infrastructure, education and social services.

The compliant behavior of DtC alcohol shippers to date has enriched states’ coffers to the benefit of many. As a leading beverage alcohol compliance solutions provider, Sovos ShipCompliant has facilitated states’ securing hundreds of millions in tax revenue each year. Because the footprint for legal DtC shipping of non-wine beverage alcohol is limited, the vast majority of this tax revenue is driven by DtC wine shipments.

DtC Tax Revenue Paid to States Via Sovos ShipCompliant

States opening to the DtC shipment of spirits would only grow these welcome additional revenues.

In conclusion

The case for spirits DtC shipping is clear. The demand is strong from producers and consumers alike, and states stand to benefit greatly. More than 15 years of complaint DtC wine shipping have paved the way for the healthy expansion of DtC beverage alcohol shipping.

Spirit producers simply want the same kind of DtC market access that wine shippers enjoy. The data shows that DtC wine shipping is profitable for states and can be done safely. Consumers are ready for more choice and are already utilizing the DtC market. The time for expanded DtC spirits shipping permissions is now.

Learn how Sovos ShipCompliant can help you manage your taxes and compliance for DtC shipping.

Talk to an expertSubscribe to our Newsletter

Get monthly updates on Sovos ShipCompliant resources, data reports, fresh resources and more.

Subscribe nowDtC Alcohol Shipping Essentials: Getting Started & Staying Compliant

A free ebook for DtC shippers of wine, beer, spirits, cider and sake

Direct-to-Consumer Alcohol Shipping Essentials: Getting Started and Staying Compliant

Direct-to-consumer (DtC) alcohol shipping continues to grow in popularity. The rise of ecommerce along with a global pandemic have fueled consumers’ desire to have products shipped directly to their doors. Producers, retailers and others would-be shippers have started exploring how best to meet this increased demand—and finding that while DtC shipping represents an excellent channel for expansion, there are numerous rules and regulations to consider.

DtC shipping laws vary from state-to-state and can even diverge from one jurisdiction to another within a state. Understanding those nuances, and how to get started in DtC alcohol shipping in the first place, is not a simple task. Laws can and do change, further increasing the difficulty of maintaining compliance.

This free ebook details the basics of what you need to know about getting started, staying compliant and finding success in DtC alcohol shipping.

Topics include:

- How to Get a License

- Age Verification

- Customer Aggregate Volume Limits (CAVL)

- Brand Label Registration

- Alcohol Not of Own Production (NOOP)

- Tax Determination and Reporting

Download your free copy of this in-depth information today.

Get the ebook

Subscribe to our Newsletter

Get monthly updates on Sovos ShipCompliant resources, data reports, fresh resources and more.

Subscribe nowInfographic: Top 5 Things Cideries Must Know About DtC Shipping

Find out the most essential considerations for compliant direct-to-consumer cider shipping.

Subscribe to our Newsletter

Get monthly updates on Sovos ShipCompliant resources, data reports, fresh resources and more.

Subscribe nowMeet Sovos ShipCompliant!

This one-minute video provides a quick introduction to our compliance and reporting solutions for wineries, breweries, distilleries, cideries, distributors, importers and other members of the beverage alcohol industry.

Subscribe to our Newsletter

Get monthly updates on Sovos ShipCompliant resources, data reports, fresh resources and more.

Subscribe nowHow and Where Retailers Can Ship Alcohol Direct-to-Consumer

Introduction

While direct-to-consumer (DtC) shipping was thrown into the spotlight by the COVID-19 pandemic, the popularity of shipping alcohol directly to consumers has been growing for some time. For wineries, DtC shipping is a $3.7 billion dollar industry. But for years, retailers have not been able to enjoy the same successes from this growing market.

The map of where retailers are allowed to ship DtC is much smaller than it is for wineries. But as DtC shipping grows in popularity retailers are starting to take more advantage of this channel and reach new customers, despite some of the added regulatory rules to comply with.

Here is what you need to know to consider shipping DtC as an off-premise retailer.

Where you can ship direct-to-consumer as a retailer

Currently, 12 states and the District of Columbia permit out-of-state retailers to sell directly to their residents, and fulfill those orders through a common carrier. Ten of these states require the retailer to receive a license, two operate under a “reciprocal” process, where only retailers located in those reciprocal states can ship to each other’s residents, and only Florida doesn't require a specific license. Except for selling to residents of these 13 states and D.C., it is illegal for a retailer to deliver beverage alcohol into any state in which it does not have a licensed retail operation.

Licensed retailer DtC states

If a retailer receives a DtC license, they may sell out-of-state directly to customers in Oregon, Wyoming, Nebraska, North Dakota, Louisiana, West Virginia, Virginia, New Hampshire, Florida, Connecticut, California and the District of Columbia. However, there are some unique situations:

- Florida and D.C. do not require an actual DtC license, but do have a set of DtC compliance rules that must be followed.

Reciprocal retailer DtC states

Beyond the 10 “license” states and D.C., there are currently two states that operate under what is known as reciprocity rules. These states are California and New Mexico, which permit shipments of wine only.

These two reciprocity states allow out-of-state retailers to sell directly to their residents only if those out-of-state retailers are located in a state that allows out-of-state retailers to sell directly to their residents without any licensing, tax or other regulatory burdens. Put more simply, the rules in state B must be as free and open for retailer DtC sales as the rules in state A for a retailer shipping from state B to sell to a resident of state A. They may also require a specific letter of agreement between the two states, indicating that there are no license or tax requirements. Currently, only California and New Mexico have such an agreement.

State rules for retailers shipping DtC

Wyoming, Louisiana, Connecticut, Florida and West Virginia permit the DtC sale of wine only for retailers. Nebraska, North Dakota, D.C. and New Hampshire permit the DtC sale of all types of beverage alcohol. Virginia permits the DtC sale of beer and wine, as does Oregon. However, Oregon only allows beer to come from states that themselves permit DtC shipping of beer.

Some other state considerations to be aware of include:

- West Virginia and New Hampshire have “dry” communities where it is illegal to sell alcohol in any manner, including DtC.

- West Virginia and Virginia will require a DtC seller to indicate to the alcohol control boards which labels will be sold via DtC.

- Virginia requires a retailer to post that they have permission from the manufacturer to resell their products through DtC, and also prohibits DtC sellers from using third-party marketing to advertise their DtC shipping option.

Packaging

When alcohol is being delivered direct-to-consumer, it must be shipped in a properly labeled package indicating it contains alcohol and an adult’s signature is required for delivery to be made. Carriers experienced with the DtC market (USPS is prohibited by federal law from accepting any packages containing alcohol) are aware of these rules and will collect signatures. These carriers will also ensure retailers have valid DtC licenses before agreeing to ship their packages. When choosing a carrier to use, a retailer should make sure that they have a well-thought out and developed alcohol program and clearly commit to fulfilling their regulatory requirements.

Tax and compliance for DtC retailers

Retailers must also follow specific tax rules. Every state that allows retailer DtC shipping, D.C., require the seller (i.e., the retailer) to collect and remit both excise taxes and sales taxes for the state they ship into. Most states also require a regular report from the retailer detailing the DtC sales they have made, though this is often coupled with an excise tax return.

While retailers should already have a handle on managing sales taxes for sales made at their licensed premises, once they begin engaging with DtC shipping they will be faced with a much bigger burden handling sales taxes in all the states they ship into. This can get complicated, because the correct sales tax rate is based on the customer’s exact deliver-to address, which can be some combination of state, county, city, and special district rates. Some states do make it easy by having a single state-wide sales tax rate, but there are places where the tax rate can be different depending on what side of the street a shipment goes to.

This can make the process of collecting and remitting tax very difficult depending on the state. Tax returns that are still reliant on paper forms or more manual filings processes can also make things difficult for a retailer now dealing with tax policies in several states at once. More states are moving toward simplified online filings, but properly collecting and remitting sales tax remains a major burden for DtC alcohol shippers.

Excise taxes

For retailers, excise tax obligations represent a novel challenge that, unlike sales taxes, many retailers may not have much experience with. This is because while excise taxes are ubiquitous in alcohol sales, they are typically handled by the distributor or possibly supplier in a three-tier sale, and therefore have been handled by the time any alcohol gets to a retailer. However, because shipping alcohol DtC into a state eliminates the parties who would normally remit the state’s excise tax, states require all DtC shippers to directly pay the excise tax due on their shipments.

Unlike sales taxes, excise taxes are fairly straightforward. They are based on the total volume of product shipped into a state, and while the rates can vary state to state, there is only one rate for a single product type or ABV range in a state. Typically, the rates are lowest for beer and cider—maybe 20 cents per gallon—and highest for spirits, with wine rates generally in the middle. One major difference for excise tax from sales tax is that the retailer may not collect the amount of excise tax due from the consumer at the time of purchase like they can with sales tax. Instead, the excise tax is supposed to be built into the listed purchasing price of the alcohol sold.

While excise taxes are in some ways a relatively simple aspect of the compliance burden for DtC shippers, they present a unique complication for retailers engaged in DtC shipping.

Filing a remittance is generally simple, only requiring the shipper to catalog total shipments made and calculate the tax due based on the products shipped. An excise tax return can be made more complicated if the return is required to be accompanied by a shipping report, for which the shipper must provide a detailed list of all shipments made during the reporting period, including date of delivery, name and address of recipient, and products shipped.

While excise taxes are in some ways a relatively simple aspect of the compliance burden for DtC shippers, they present a unique complication for retailers engaged in DtC shipping. This is because all alcohol sold by retailers has already had their state’s excise tax assessed and remitted against it. Retailers are required to purchase the alcohol they resell within their state’s three-tier market, meaning that it came from a local distributor (or from a self-distributing manufacturer where allowed) who was already obligated to pay the local excise tax for that alcohol. But if the retailer then resells that alcohol DtC into a different state, they would be obligated to remit the excise tax of that other state as well.

For example, if a California retailer ships a wine DtC to a consumer in Illinois, that wine would have already had a 20-cent per gallon tax remitted to California (paid by the distributor or winery the retailer received the wine from) and then would also be subject to the $1.39 per gallon excise tax in Illinois, to be paid by the retailer. As such, this creates a double-taxation scenario where alcohol shipped by retailers DtC is ultimately subject to more tax than alcohol shipped DtC by the manufacturer (who can sell alcohol that has not already been tax-paid in their home state). Requiring DtC shippers to remit the ship-to state’s excise tax does make policy sense, to create parity with other sales in that state and ensure the state keeps its coffers full, but the extra burden on retailers engaged in DtC shipping remains a point of contention, though perhaps it may just be the price paid by retailers to engage in this market.

Will DtC shipping for retailers expand in the future?

While there is a lot of interest among retailers and consumers for DtC shipping opportunities, the map for retailer DtC shipping map is a lot smaller than it is for other entities, particularly wineries. Part of the reason for this is the perception of unfair advantages that a remote retailer might have over local retailers, which leads to demands for laws restricting “foreign” competition. There is also concern among regulators that they lack the jurisdiction to properly monitor and control retailers located in other states. However, the general success of retailer shipping in the states that do allow it would seem to belie these concerns.

Another issue currently facing the retailer DtC shipping market is the lack of a national policy on whether states can extend discriminatory permissions for local retailers to do DtC shipping, while blocking that permission for remote retailers. The 2005 Supreme Court case Granholm v. Heald established the modern jurisprudence around DtC shipping of alcohol, primarily that states could not allow local shipping of wine while prohibiting it from out-of-state sources. However, that case only mentioned producers (wineries, really, but it has become accepted that the principles would also apply to breweries and distilleries) and it left open the question of retailers. There have been efforts over the years to extend Granholm to retailers, but they have been unsuccessful so far and even faced increasing pushback in just the last year or two.

Nevertheless, if the number of states that allow out-of-state retailer DtC shipping were to expand, there would be great benefit for consumers. There are a number of retailer DtC myths saying that out-of-state retailer DtC permissions would harm local retailers and that states would miss out on the tax revenue. This is untrue, as evidence shows that where allowed to ship DtC, retailers are active in complying with regulatory requirements, including getting licensed and protecting against sales to minors. Those states that allow retailer DtC shipping have earned additional tax revenue they otherwise would not have and they continue to have thriving local retailer markets.

The fact is that shipping of alcohol entails a lot of additional costs, particularly when it comes to the time and fees for shipping, that do not exist with local retailer sales. As such, DtC shipping by retailers largely focuses on purchases of specialty or unique wines that are not distributed in the destination state. The key example is the Nebraska consumer looking for a specialty imported wine that is sold only by one or two select New York retailers who have access to the importer; there is not enough demand in Nebraska (or most states) for a local distributor to pick up that wine, and therefore it is otherwise unavailable to the Nebraska consumer. (While many states do offer “special order” options, that is a long and complicated process that depends on finding a local distributor willing to take the time and effort to manage a single sale.) This is a very different scenario than the sale of a $20 bottle of widely distributed wine, for which any consumer is going to rely on their local wine shop for a purchase.

Hopefully, as DtC shipping continues to grow, more states will see the benefits of retailer DtC shipping and pass legislation that allows consumers to purchase beverage alcohol products they normally wouldn’t have access to.

Learn how Sovos ShipCompliant can help you manage your taxes and compliance for DtC shipping as a retailer.

Talk to an expertSubscribe to our Newsletter

Get monthly updates on Sovos ShipCompliant resources, data reports, fresh resources and more.

Subscribe nowWhite Paper: A Guide to Direct-to-Consumer Taxes for Brewers and Distillers

Get the whitepaper

Brewers and distillers entering the direct-to-consumer (DtC) shipping channel face numerous regulatory requirements, including a variety of tax implications. In fact, taxes on DtC shipments present a special challenge, as they require the shipper to recognize and manage a broader tax burden than if they were selling only through a state’s three-tier system. This extends to both a state’s excise taxes, based on the volume of sales made, and a state’s sales taxes, based on the value of sales made.

This free white paper takes a look at what those obligations are and how breweries and spirits producers can navigate them. Topics discussed include:

- Sales tax rules for shipping beer and spirits direct-to-consumer

- Excise tax requirements

- Some unique tax scenarios for DtC alcohol shippers

Staying on top of tax obligations is critical to remaining in compliance when shipping alcohol to consumers across state lines, thus avoiding the risk of fines and other penalties.

Download your free copy of this white paper today for an expert overview of these essential tax topics for DtC beer and spirits shippers.

Subscribe to our Newsletter

Get monthly updates on Sovos ShipCompliant resources, data reports, fresh resources and more.

Subscribe nowInfographic: 4 Essential Traits to Look for in Your Compliance Partner

Subscribe to our Newsletter

Get monthly updates on Sovos ShipCompliant resources, data reports, fresh resources and more.

Subscribe now