By Andrew Adams, Editor, WineBusiness Analytics

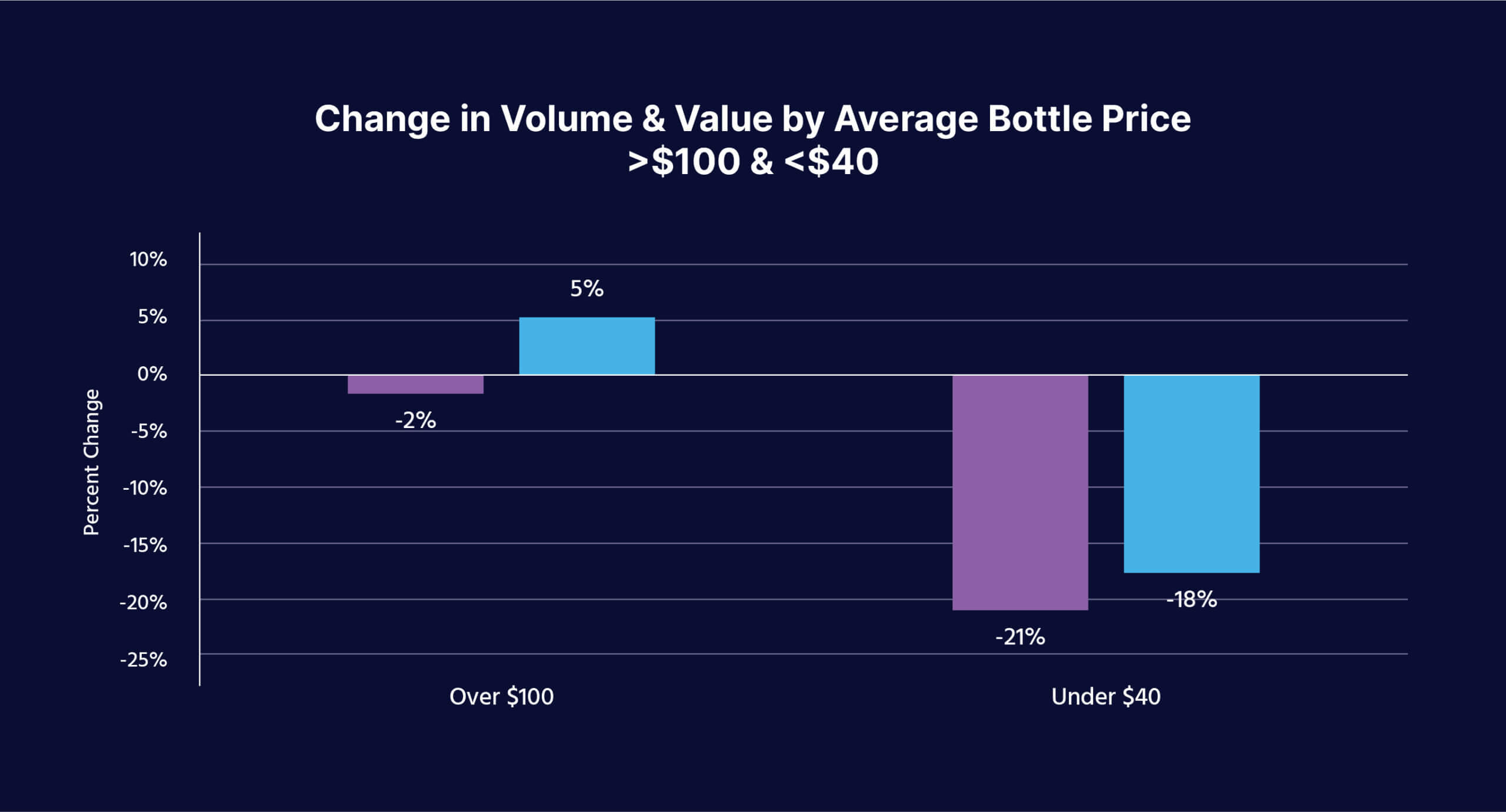

The pandemic surge in DtC wine shipments temporarily obscured a structural change that is now hard to ignore. The story is told in a chart from this year’s annual report on winery direct-to-consumer (DtC) shipments depicting the change in value and volume of shipments of wines priced more than $100 and less than $40.

These two price tiers at opposite ends of the wine price spectrum illustrate one of the defining characteristics of the post-pandemic DtC shipment market. Total value of wines priced more than $100 grew 5% year-over-year, and volume declined by just 2%, which is significantly better than the overall channel. Meanwhile wines priced less than $40 did worse, declining 18% by value and 21% by volume.

Premiumization at Play?

It’s clear now that this change is not the result of premiumization, which had been defined in the previous decade as wine drinkers buying the same amount of wine but at higher prices. What’s happened among DtC shipments is, instead, referred to in the annual report as “mix shift” — shipments of the most expensive wines now account for a larger share of the total market as fewer bottles of more affordable wines are shipped DtC.

What the Pandemic Years Hid

The surge in total shipment volume seen in 2021 and 2022 obscured this trend, which appears to have been in play even then.

In 2020, shipments of wines priced more than $50 accounted for 52% of total shipment value of $3.7 billion. Last year, total shipment value also came to $3.7 billion but wines with an average price of more than $50 accounted for 71% of total value. Among shipments by Napa County wineries the share has increased from 75% to 88% and for wineries located in states east of the Rocky Mountains, or “Rest of U.S.”, the share has increased from 11% to 20%.

Since 2020, total shipment value of all wines with an average price of more than $50 grew 36% at an average annual rate of 5% across all major winery regions.

Wineries in all regions and of all sizes and price points relied on the DtC channel to offset losses from the on-premise market and other disruptions during the COVID-19 pandemic. Just as recent years have seen an increase in the share of higher-priced bottles, 2021 and 2022 saw a dramatic increase in more affordable prices that pushed total volume to unprecedented levels that have not been matched.

Rising Bottle Prices and the Impacts

As the pandemic came to an end, shipments of more affordable wines rapidly began to decline. Many wineries increased their prices to stay ahead or integrate increased costs for packaging materials and shipping, and for the all-important appearance of free (included) shipping through a seamless, simplified online checkout process to prevent shopping carts from being abandoned.

As winery prices rose, consumers have also pulled back on their spending because of a host of reasons that have led to a downturn in wine sales and nearly all other beverage alcohol products.

The increase in shipments of higher-priced wines has helped keep total DtC shipment value outpacing volume, but even that trend is slowing. Compared to 2024, shipment value of wines priced more than $50 slipped 1%, while the total volume of such wines declined 7%.

In 2025, the total shipment volume of wines with an average price of more than $50 accounted for roughly 37% of total channel volume and that’s about the same as in 2024. Total channel volume last year, however, declined by nearly 1 million cases, meaning some of that value “growth” really was from the same amount of wine accounting for a larger share of a shrinking market.

What’s Ahead for DtC Wine Shipping?

Taken together, we see a DtC channel increasingly shaped by price pressure, changing consumer behavior, and the unwinding of pandemic-era distortions. Winery DtC shipments started 2026 off on a weak note, declining nearly 28% by volume in January. The start of the year has always been a slow period for shipments, but the size of the decline is a strong indication the trends of the previous year have continued into this one.