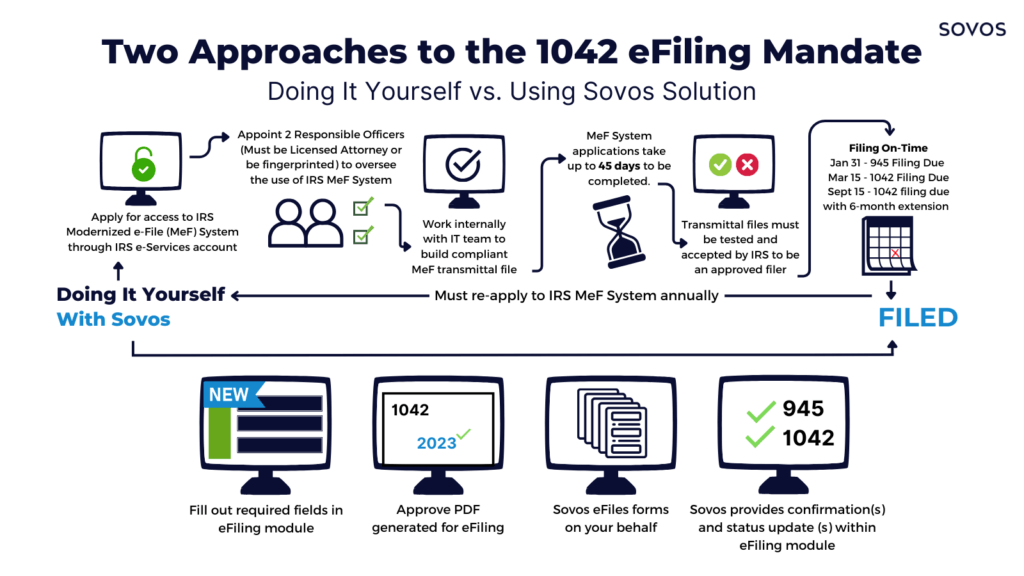

Better understand the new eFiling requirements for Form 1042

Learn the detailed, step-by-step registration process with the IRS MeF system

Comprehend the ramifications of failing to account for the eFiling updates

Understand compliance best practices for IRS filing requirements

Utilize the right solutions and services for 1042 eFiling needs